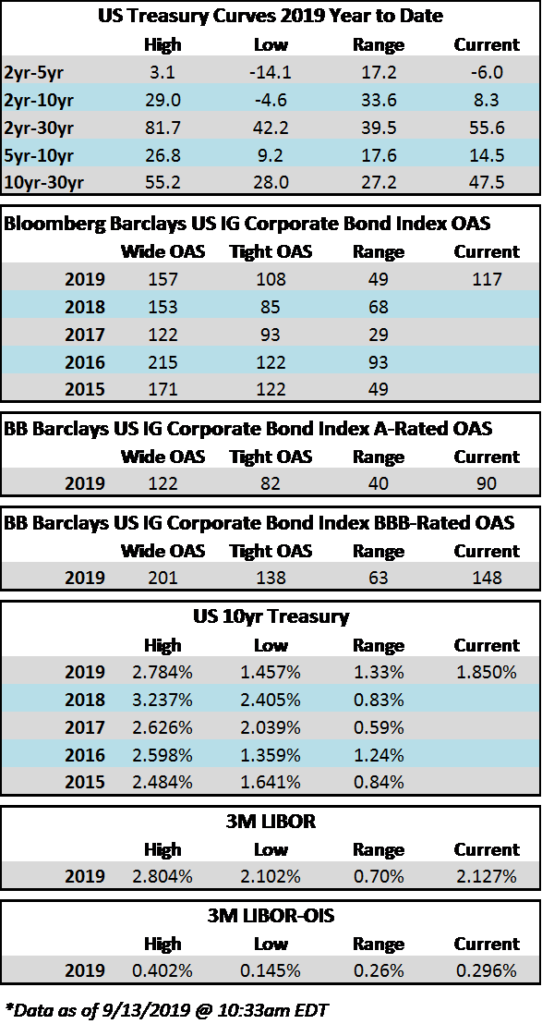

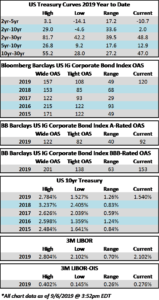

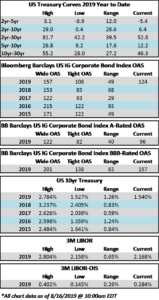

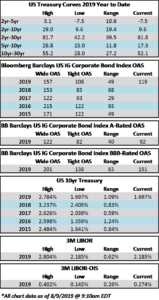

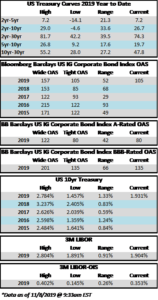

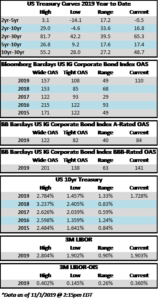

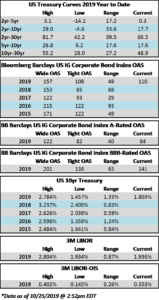

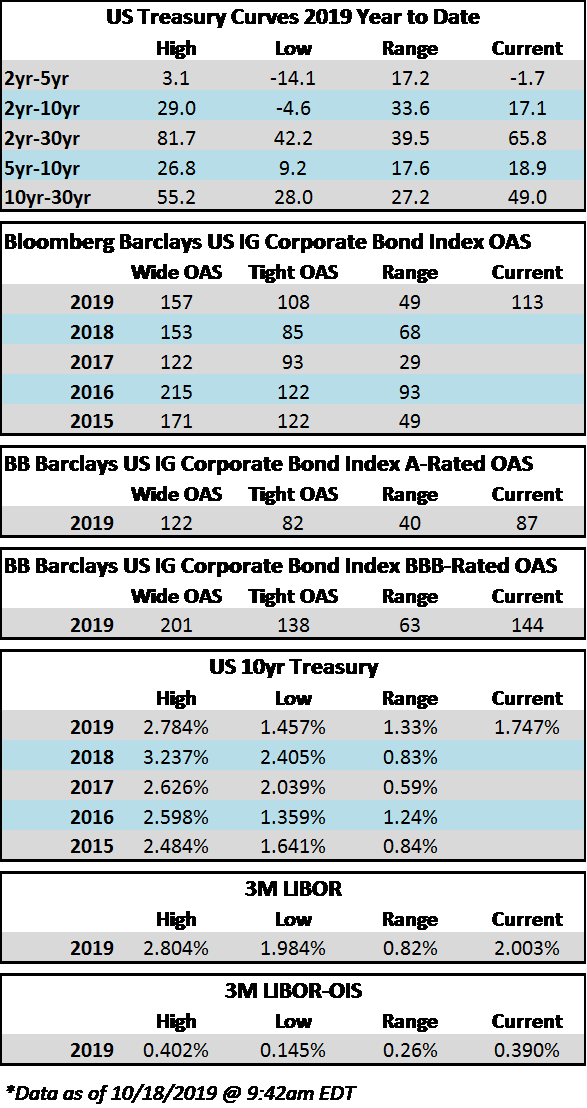

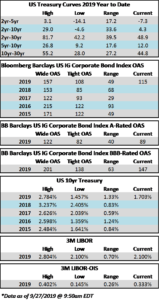

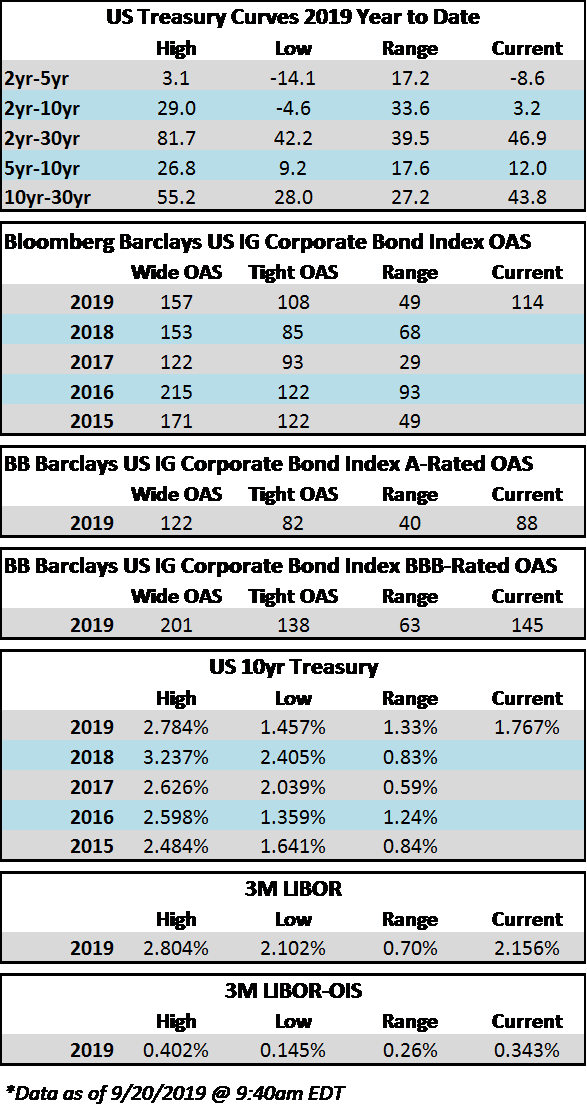

Credit spreads were tighter during the week and are now at the tightest levels of 2019. The spread on the Bloomberg Barclays Corporate Index closed at 105 on Thursday and there is a positive tone in the air on Friday morning which could lead to an even tighter close as we head into the long weekend –the bond market is closed on Monday in honor of Veteran’s Day. The move in Treasuries during the week has more than overshadowed tighter credit spreads. It has been a quick and violent move higher in rates. As we go to print the 10yr Treasury is over 22 basis points higher on the week while the 30yr is 21 basis points higher. Unpredictability in rate moves is the principal reason that we are “rate agnostic” at CAM and instead focus on credit risk while avoiding interest rate speculation by always positioning investor portfolios in intermediate maturities.

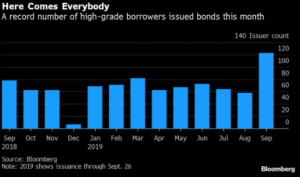

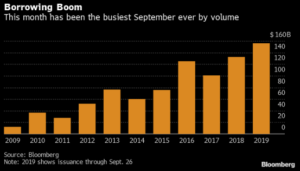

The primary market got a decent start to the month as $21.8bln in new debt came to market. The pace should pick up substantially as soon as next week due to pending M&A funding from AbbVie which could total near $30bln. 2019 issuance has now passed the trillion dollar mark and it stands at $1,014bln which trails 2018 by -7%.

According to Wells Fargo, IG fund flows during the week of October 31-November 6 were +$3.2bln. This brings YTD IG fund flows to +$249bln. 2019 flows are up 9.5% relative to 2018.

Bloomberg) Global Bond Sell-Off Persuades Some Investors to Buy the Dip

- Recent losses in Treasuries, which crescendoed Thursday into one of the worst days since Donald Trump was elected president, look like a buying opportunity for many investors who have a grim view of the economy’s prospects.

- And it appears some are pouncing, with traders cashing out bearish wagers and buy-the-dip buyers rushing in. The rekindled interest in the safety of bonds nudged yields on the 10-year, which had climbed to a three-month high of 1.97% on Thursday, down to as low as 1.89% in early European trading Friday before bouncing back to around 1.94%. European bonds rebounded after French and Belgian yields had climbed above 0% Thursday.

- Signs of progress in U.S.-China trade talks have thrashed bonds for days, and the two countries agreed Thursday to roll back tariffs on each other’s goods if a deal is reached. The Treasury market has seen a huge turnaround since August, when fears that global growth is slowing prompted the biggest monthly rally since 2008.

(Bloomberg) U.S. Says Phase-One China Deal Would Include Tariff Rollback

- The U.S. and China have agreed to roll back tariffs on each other’s goods in stages as negotiations continue over resolving the more than yearlong trade war, officials on both sides said.

- “In the past two weeks, top negotiators had serious, constructive discussions and agreed to remove the additional tariffs in phases as progress is made on the agreement,” China’s Ministry of Commerce spokesman Gao Feng said Thursday.

- White House economic adviser Larry Kudlow confirmed the advance in negotiations. “If there’s a phase one trade deal, there are going to be tariff agreements and concessions,” he told Bloomberg.

- An agreement to ratchet back tariffs would pave the way for a de-escalation in the trade war that’s cast a shadow over the world economy. China’s key demand since the start of negotiations has been the removal of punitive tariffs imposed by Trump, which by now apply to the majority of its exports to the U.S.

- “If China, U.S. reach a phase-one deal, both sides should roll back existing additional tariffs in the same proportion simultaneously based on the content of the agreement, which is an important condition for reaching the agreement,” Gao said Thursday.

(Bloomberg) The Repo Market’s a Mess. (What’s the Repo Market?): QuickTake

(Bloomberg) The Repo Market’s a Mess. (What’s the Repo Market?): QuickTake