Second Quarter Commentary & Outlook

July 2026

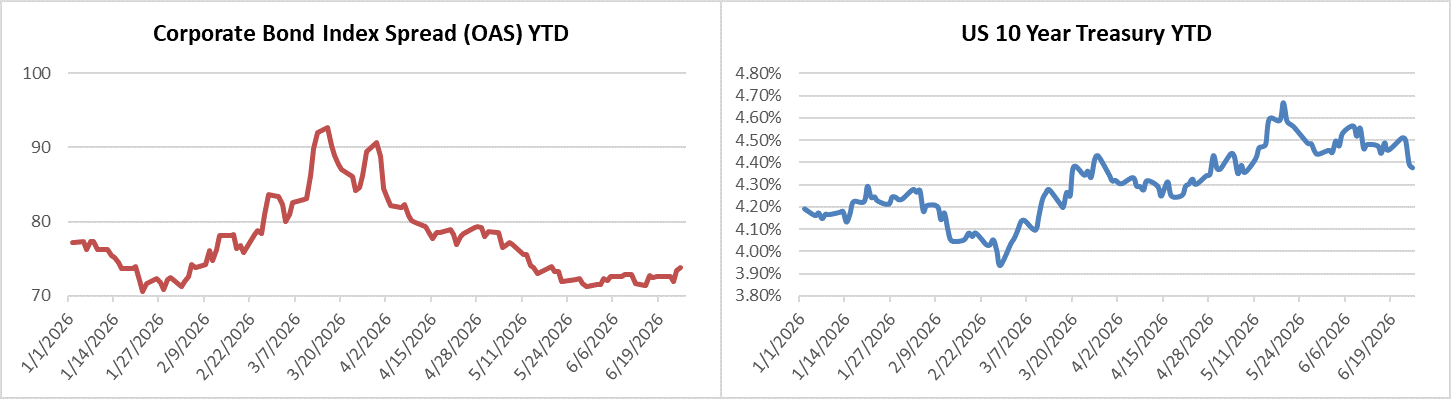

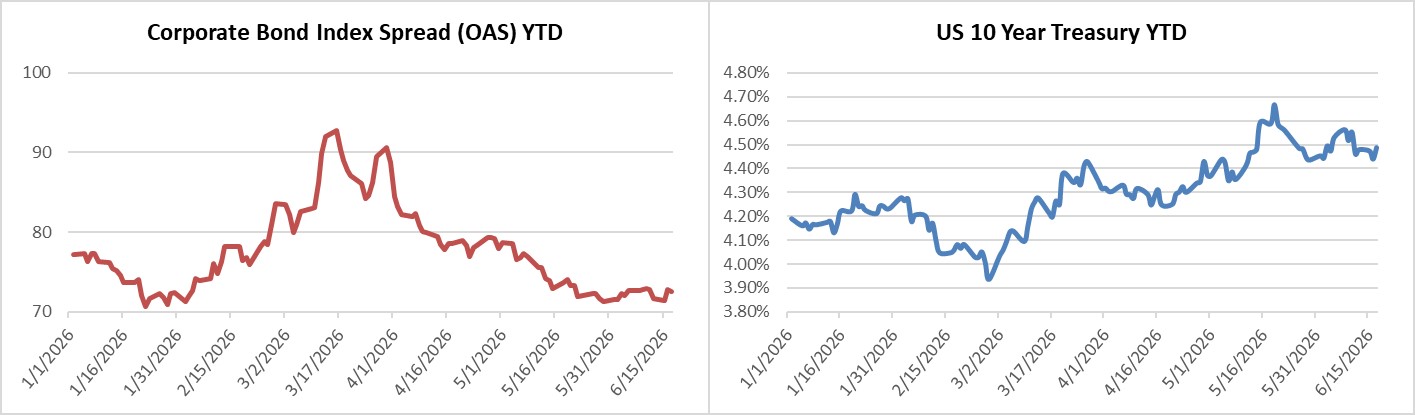

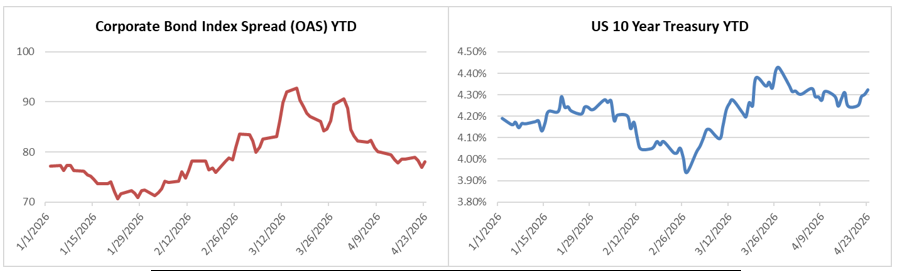

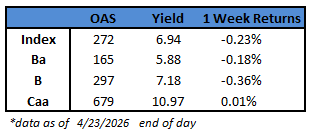

In the second quarter of 2026, the Bloomberg US Corporate High Yield Index (“Index”) return was 2.47% bringing the year to date (“YTD”) return to 1.96%. The S&P 500 index return was 15.20% (including dividends reinvested) bringing the YTD return to 10.19%. Over the period, while the 10 year Treasury yield increased 15 basis points, the Index option adjusted spread (“OAS”) tightened 47 basis points moving from 317 basis points to 270 basis points.

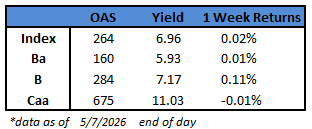

With regard to ratings segments of the High Yield Market, BB rated securities tightened 42 basis points, B rated securities tightened 68 basis points, and CCC rated securities widened 45 basis points. The chart below from Bloomberg displays the spread move of the Index over the past five years. For reference, the average level over that time period was 343 basis points.

The sector and industry returns in this paragraph are all Index return numbers. The Index is mapped in a manner where the “sector” is broader with the more specific “industry” beneath it. For example, Energy is a “sector” and the “industries” within the Energy sector include independent energy, integrated energy, midstream, oil field services, and refining. The Banking, Finance Companies, and Other Financials sectors were the best performers during the quarter, posting returns of 3.72%, 3.67%, and 3.44%, respectively. On the other hand, Communications, Energy, and Insurance were the worst performing sectors, posting returns of 1.60%, 1.63%, and 1.70%, respectively. At the industry level, office REITs, life insurance, and healthcare REITs all posted the best returns. The office REITs industry posted the highest return of 5.77%. The lowest performing industries during the quarter were railroads, cable, and retail REITs. The -6.72% posted by the railroads industry was the lowest return by any industry.

After the very strong issuance of 2025, Q1 posted a robust $92.7 billion in new issuance and Q2 was even stronger at $127.7 billion. Of the issuance that did take place during Q2, Communications took 26% of the market share followed by Discretionary at 16% share, and Financials at 15% share.

The Federal Reserve held the Target Rate steady at the April and June meetings. There was no meeting held in May. More interesting to note is that the new Fed Chair Kevin Warsh made his debut and the Fed changes that are afoot. Kevin Warsh’s first Fed meeting marked a regime shift: less guidance and a stripped-down statement. But the message was clearly hawkish from his committee and the markets.i Fed communications will be much reduced going forward as Warsh isn’t really a fan and is creating a task force to evaluate. The Fed dot plot was still released after the June meeting, but the Chairman chose not to provide his own projection dot. At the post-meeting press conference, he was quite clear that inflation is very much in the Committee’s cross-hairs stating, “Persistently high prices are a burden for the American people. This committee will deliver price stability.” For their part, market participants are now forecasting hikes instead of cuts in the Fed Target rate for 2026. At the end of March, investors were pricing in an implied rate cut of 7 basis points for 2026. Currently, the implied rate move being priced in is a hike of 34 basis points for 2026.ii More broadly, Warsh said another task force would examine the Fed’s reliance on economic data built from surveys, arguing that official statistics haven’t kept pace with the real-time information used in the private sector. The Fed will also review job frameworks, inflation frameworks, and the Fed balance sheet, creating a total of five separate task forces.

Intermediate Treasuries increased 15 basis points over the quarter, as the 10-year Treasury yield was at 4.32% on March 31st, and 4.47% at the end of the second quarter. The 5-year Treasury increased 29 basis points over the quarter, moving from 3.94% on March 31st, to 4.23% at the end of the second quarter. Intermediate term yields more often reflect GDP and expectations for future economic growth and inflation rather than actions taken by the FOMC to adjust the target rate. The revised first quarter GDP print was 2.1% (quarter over quarter annualized rate). Looking forward, the current consensus view of economists suggests a GDP for 2026 around 2.1% with inflation expectations around 3.5%.iii

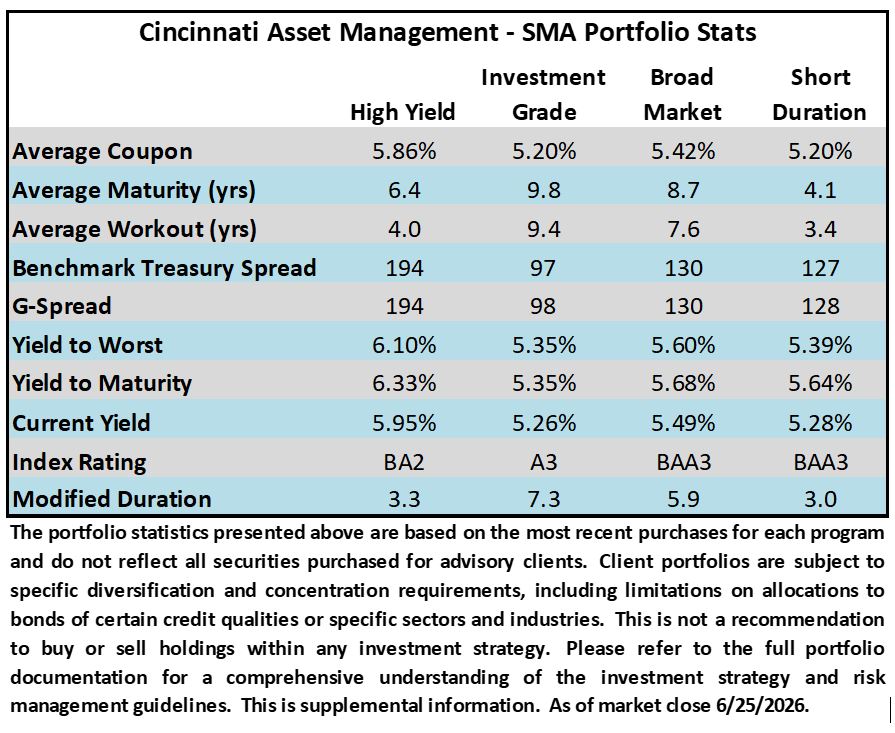

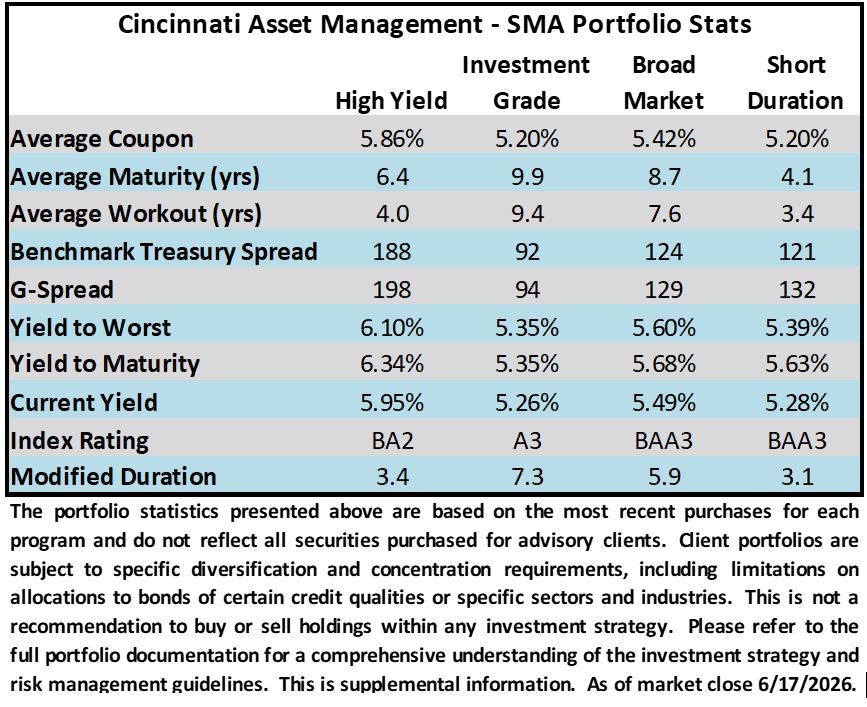

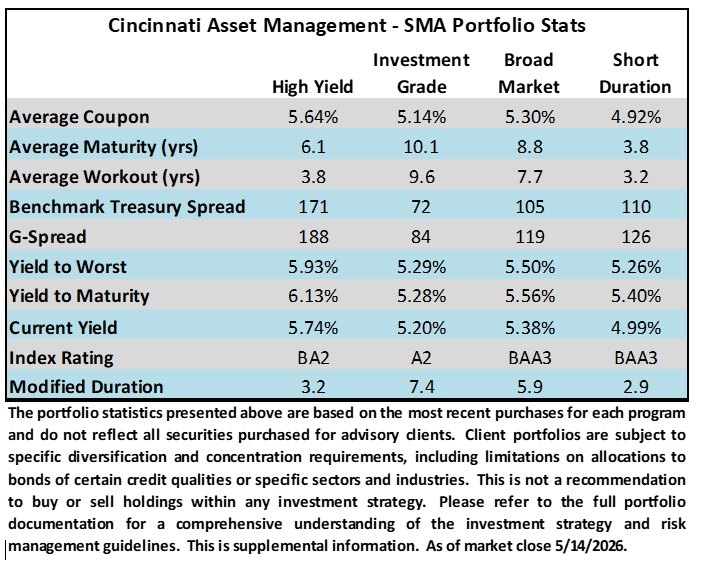

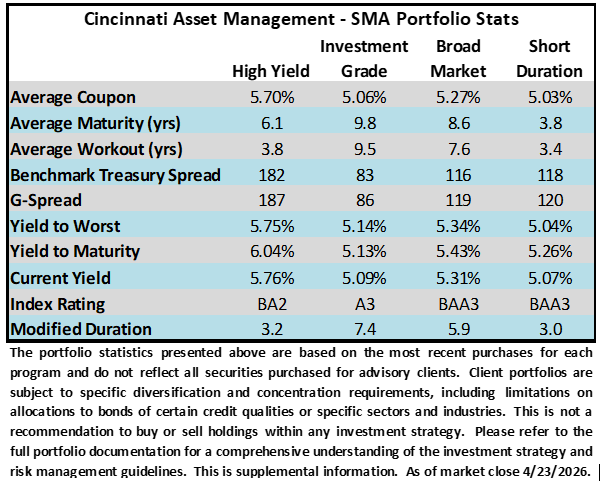

Being a more conservative asset manager, Cincinnati Asset Management does not buy CCC and lower rated securities. Additionally, our interest rate agnostic philosophy keeps us generally positioned in the five to ten year maturity timeframe. During Q2, our higher quality positioning was a negative to performance as lower rated securities outperformed. Our natural cash overweight was also a drag on performance as the Index produced a solid return in Q2. An additional performance detractor included our credit selections within the consumer cyclicals sector. Benefiting our performance this quarter were our credit selections in the basic industry sector and selections within the utilities sector. Another benefit was added due to our overweight in the banking sector.

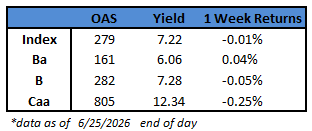

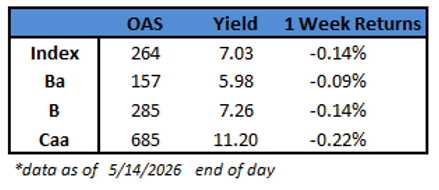

The Bloomberg US Corporate High Yield Index ended the second quarter with a yield of 7.16%. Treasury volatility, as measured by the Merrill Lynch Option Volatility Estimate (“MOVE” Index), had a spike to 115, a level well above the 80 index average of the past 10 years, as the conflict in Iran got in full swing toward the end of Q1. However, with much of the steam released from that pressure cooker, the current rate stands at a more reasonable level of 72. Data available through May shows 14 bond defaults so far in 2026 which is relative to 16 defaults in all of 2022, 41 defaults in all of 2023, 34 defaults in all of 2024, and 32 defaults in all of 2025. The trailing twelve month dollar-weighted bond default rate is 1.93%.iv The current default rate is relative to the 2.06%, 1.83%, 1.52%, 1.65% default rates from the previous four quarter end data points listed oldest to most recent. Defaults are generally stable and the fundamentals of high yield companies are in decent shape. From a technical view, fund flows are negative this year through May data at -$6.6 billion.v No doubt there are risks, but we are of the belief that for clients that have an investment horizon over a complete market cycle, high yield deserves to be considered as part of the portfolio allocation.

As the month of June got underway, oil prices were already coming down off highs in anticipation of a US and Iran conflict resolution. A Memorandum of Understanding was signed mid-June and oil prices continued to slide throughout the month as the MoU included reopening the Strait of Hormuz. Unfortunately, inflation remains stubbornly elevated as energy prices are only one of the contributing factors. This year has seen budding momentum in job growth, the economy has remained resilient, and the artificial intelligence buildout continues to see a flood of investment spending. The market narrative will likely remain in flux, as we wrap up the commentary for this quarter, a freshly released jobs report showed US hiring slowed sharply in June after downward revisions to the previous two months. There will certainly be plenty to evaluate as we move through the second half of 2026. Our exercise of discipline and credit selectivity is important as we continue to evaluate that the given compensation for the perceived level of risk remains appropriate. As always, we will continue our search for value and adjust positions as we uncover compelling situations. Finally, we are very grateful for the trust placed in our team to manage your capital.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results. Gross of advisory fee performance does not reflect the deduction of investment advisory fees. Our advisory fees are disclosed in Form ADV Part 2A. Accounts managed through brokerage firm programs usually will include additional fees. Returns are calculated monthly in U.S. dollars and include reinvestment of dividends and interest. The index is unmanaged and does not take into account fees, expenses, and transaction costs. It is shown for comparative purposes and is based on information generally available to the public from sources believed to be reliable. No representation is made to its accuracy or completeness. Additional disclosures on the material risks and potential benefits of investing in corporate bonds are available on our website: https://www.cambonds.com/disclosure-statements/.

i Bloomberg June 18, 2026: Warsh’s Fed Opens with Less Guidance

ii Bloomberg July 1, 2026: World Interest Rate Probability

iii Bloomberg July 1, 2026: Economic Forecasts (ECFC)

iv Moody’s June 16, 2026: May 2026 Default Report and data file

v Bloomberg July 1, 2026: Fund Flows