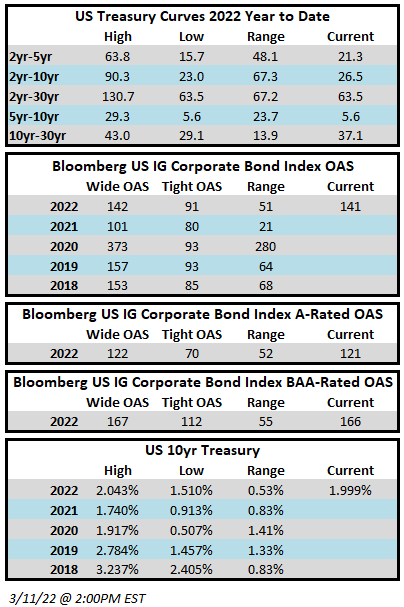

Spreads are wider week over week in what seems to have become a recurring theme. The tone of the market is mixed as we go to print this Friday afternoon but market participants remain wary of risk. Geopolitical turmoil in Europe remains at the forefront but there have been other challenges and there are more ahead –the market survived the highest CPI print in over 40 years on Thursday morning and all eyes are looking toward the FOMC meeting next Wednesday. The OAS on the Bloomberg US Corporate Bond Index closed at 141 on Thursday, March 10, after having closed the week prior at 130. The Investment Grade Corporate Index had a negative YTD total return of -7.9% through Thursday. The YTD S&P500 Index return was -10.6% and the Nasdaq Composite Index return was -16.1%.

The primary market had its 8th busiest week on record and volume will approach $70bln by the end of the week. Magallanes, which is the WarnerMedia SpinCo for assets that AT&T is selling to Discovery Communications, led all issuers this week with a $30bln debt deal across 11 tranches. This was the fourth largest bond offering in history. Next week should continue to see a brisk pace of issuance as it is well known that Oracle will soon be in the market to finance its acquisition of Cerner and there are other issuers waiting in the wings as well. We have mentioned this in previous notes but it bears repeating; even amid widening spreads, geopolitical uncertainty and a pivot in Fed policy, the investment grade new issue market remains wide open and the secondary market is showing signs of good liquidity and two-way flow with low transaction costs.

Per data compiled by Wells Fargo, flows for investment grade were negative on the week. Outflows for the week of March 3–9 were -$4.7bln which brings the year-to-date total to -$19.3bln.