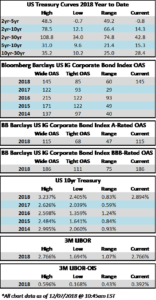

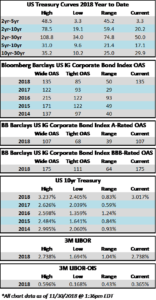

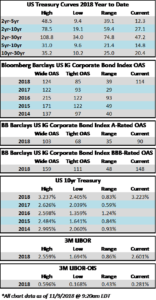

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $2.0 billion and year to date flows stand at $1.0 billion. New issuance for the week was zero, and high yield has not seen a new issue in over 5 weeks now.

(Bloomberg) High Yield Market Highlights

- U.S. junk bonds traded slightly higher yesterday, adding to recent strong gains as investors piled back into the asset class and issuance restarted. The index is up 3.06 percent this year, the best return in fixed income.

- U.S. corporate high-yield funds swung back to inflows

- Junk bond index yield dropped to 7.23%, lowest since Dec. 4

- Index return was 0.04% yesterday, extending rising streak to 10 days

- Energy sector and triple C debt outperformed

- CCC yield dropped to 11.38% vs. 12.77% on Dec. 26

- This was the tenth day of decline, marking the longest falling streak since December 2016, Bloomberg data show

- CCCs YTD return is 4.38%

- High- yield U.S. bonds are unlikely to move much higher, following the best start to a year since 2009, UBS strategists said in a note

(Reuters) PG&E falls further after S&P cuts credit rating to junk

- PG&E Corp’s shares fell 14 percent on Tuesday, after S&P Global stripped the California power company of its investment-grade credit rating in the face of massive claims stemming from deadly wildfires.

- S&P cut the rating on PG&E and its Pacific Power & Gas Co unit on Monday to “B” from “BBB-,” the lowest tier of so-called investment-grade ratings, citing political and regulatory pressure and uncertainty over its potential liabilities.

- The utility, whose roughly $18 billion in bonds fell on Monday due to bankruptcy fears, has come under severe pressure since a fatal Camp fire in November compounded its woes. It currently faces billions of dollars in liabilities related to wildfires in 2017 and 2018.

- S&P Global said it could further cut the company’s rating over the next few months if explicit steps are not taken by authorities to improve the regulatory situation, signaling that the agency may be losing faith that lawmakers could rescue PG&E.

(Fierce Wireless) T-Mobile/Sprint merger review suspended

- The federal government funding lapse has claimed another victim, at least temporarily. The FCC has paused its review of the $26 billion proposed merger between T-Mobile and Sprint for the second time in four months.

- The 180-day review period for mergers and other transactions that require FCC approval, otherwise known as a shot clock, was suspended earlier this week (PDF) when the agency shut down most operations due to the ongoing impasse over federal government funding. The partial government shutdown has effectively put the timeline for a final decision on hold until Congress and the president come to an agreement on a federal government spending bill.

(Bloomberg) T-Mobile Outpaces Even Verizon’s Strong Growth in Customer Adds

- T-Mobile US Inc.’s fourth-quarter wireless customer gains surpassed analyst estimates and topped strong growth at larger rival Verizon Communications Inc., continuing the company’s run as the fastest-growing U.S. mobile carrier.

- The phone provider said it added 1.4 million regular monthly wireless customers, according to preliminary results. Analysts expected 985,000 new subscribers, according to data compiled by Bloomberg. The new additions included 1 million phone customers,

more than the 650,000 Verizon added in the quarter. - T-Mobile’s outperformance of even Verizon’s surprisingly strong numbers is a signal that it’s continuing to take the most market share among U.S. carriers.

- The results suggest it’ll be tough for AT&T Inc. and T-Mobile’s planned merger partner Sprint Corp. to hit their current estimates for subscriber growth, in a mature wireless

market that has seen little new-customer growth overall.

(Bloomberg) U.S. Says China Willing to Buy More American as Trade Talks End

- The Trump administration wrapped up the latest round of trade talks in Beijing, noting a commitment by China to buy more U.S. agricultural goods, energy and manufactured items.

- China and the U.S. concluded three days of talks on Wednesday with a cautious sense of optimism that the world’s two biggest economies might be able to reach a deal that ends their bruising trade war.

- In a statement, the office of U.S. Trade Representative Robert Lighthizer said the two sides considered ways to “achieve fairness, reciprocity, and balance in trade relations.” Officials discussed the need for any deal to include “ongoing verification and effective enforcement,” USTR said. The U.S. will decide on the next steps after officials report back to Washington.