CAM Investment Grade Weekly Insights

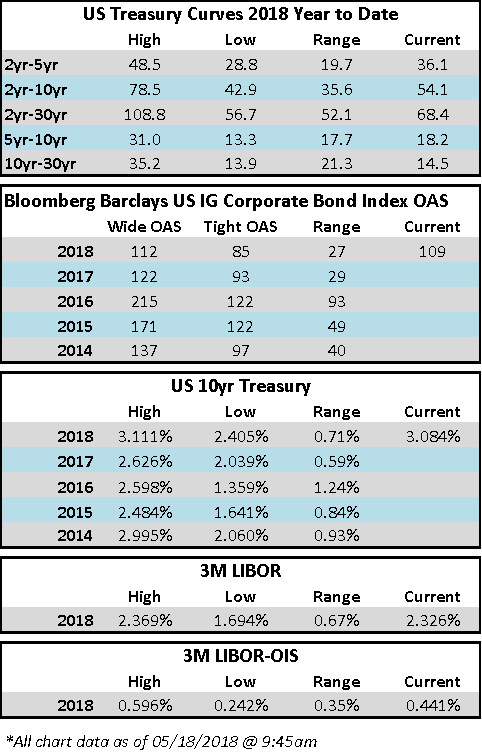

Fund Flows & Issuance: According to Wells Fargo, IG fund flows for the week of May 10-May 16 accelerated from prior weeks, with a positive inflow of $3.5 billion. Short duration funds have registered 80% of all inflows over the past four weeks, according to Wells. IG funds have garnered $65.764 billion in net inflows YTD.

Per Bloomberg, over $30bn in new corporate debt priced for the second straight week. This brings the YTD total to $509bn. The pace of new issuance is off 2% relative to this point in 2017.

(WSJ) The Era of Low Mortgage Rates Is Over

- Mortgage rates this week jumped to their highest level since 2011, signaling a shift from a period of ultracheap loans to a higher-rate environment that could slow home price appreciation and squeeze first-time buyers.

- The average rate for a 30-year fixed-rate mortgage rose to 4.61% this week from 4.55% last week, according to data released Thursday by mortgage-finance giant Freddie Mac.

- The concern among economists is that higher rates will prompt homeowners to keep their low-rate mortgages rather than trade up for better properties. As rates approach 5%, the risk of the phenomenon known as rate lock grows, economists said.

- A one percentage point increase in rates can lead to a reduction in home sales of 7% to 8%, according to Lawrence Yun, chief economist at the National Association of Realtors. The recent increases in home prices and mortgage rates could especially hurt first-time and moderate-income borrowers, economists said.

- The Mortgage Bankers Association expects refinancings to decline 26% this year, after plunging 40% last year.

(WSJ) What Do Tesla, Apple and SoftBank Have in Common? They’re All Hot for Lithium

- Tesla Inc. and a large Chinese firm each struck deals with lithium producers, the latest sign that big users are rushing to secure supplies of the material used in electric-car and cellphone batteries.

- Both lithium and cobalt, which is also used in these batteries, face potential shortages in the years ahead as electric-vehicle use increases.

- That concern is driving a number of companies like technology firms and car makers reliant on lithium and cobalt to strike deals now, even if it means joining with suppliers that haven’t started producing yet.

- In addition to the sector’s dominant players such as Glencore PLC and Albemarle Corp. , analysts estimate there are more than 100 smaller lithium miners and about 25 cobalt firms. Many are publicly traded in Canada and Australia, and some have already clinched deals with big users. “It just looks like we’re on the precipice of this wave,” said Chris Berry, founder of House Mountain Partners LLC, a New York-based adviser to battery-metals companies and investors. “You’re going to need a lot of investment in a hurry to meet demand.”

- But the rush to lock in deals could turn out to be a speculative bust. Prices of lithium and cobalt more than doubled from 2016 through last year, but the rally has cooled off recently amid worries about oversupply. Some investors also think manufacturers will replace pricey materials like lithium and cobalt using different types of batteries with a higher concentration of cheaper metals such as nickel.

- Analysts expect demand for the materials used to power electric vehicles and smartphones to more than double by 2025, pushing transportation and technology companies into exploring unconventional deals to meet that pressing need.

- Many lithium and cobalt mines are located in regions that have historically been unstable: Congo in the case of cobalt, and South America for lithium, adding to worries about a supply shortage.

(Bloomberg) U.S. Retail Sales Gain Points to Healthier Second Quarter

- S. retail sales rose in broad fashion last month as bigger after-tax paychecks helped compensate for rising fuel costs, signaling consumer demand was off to a firm start this quarter.

- The value of sales increased 0.3 percent in April, matching the median forecast, after a 0.8 percent advance in the prior month that was stronger than initially reported, Commerce Department figures showed Tuesday.

- So-called retail-control group sales, which are used to calculate gross domestic product and exclude food services, auto dealers, building materials stores and gasoline stations, improved 0.4 percent after an upwardly revised 0.5 percent gain.

- The results add to the expectation that consumer spending, the biggest part of the economy, will rebound from its first-quarter weak patch. A strong job market and higher take-home pay in wake of tax reductions are buoying Americans’ wherewithal to spend and cushioning the squeeze from costlier fuel that leaves people with less money to buy other goods and services.

- Nine of 13 major retail categories showed advances in April, led by the biggest jump in sales at apparel stores since March of last year. Increased receipts were also evident at furniture merchants, building-materials outlets, Internet retailers and department stores.

- While consumer spending has remained solid in this expansion, business investment has also been posting strong growth in recent quarters. Tax cuts that President Donald Trump signed into law at the end of 2017 were seen as providing a further jolt to consumption and capital spending that would spur growth toward the president’s 3 percent goal.

- Economists including those at Bank of America Corp. and JPMorgan Chase & Co. have noted the recent runup in gasoline prices, and said persistently higher fuel costs this year would risk eroding a sizeable portion of the tax benefits.