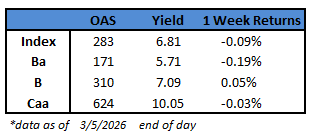

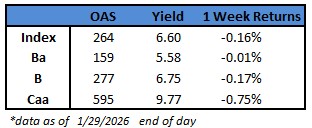

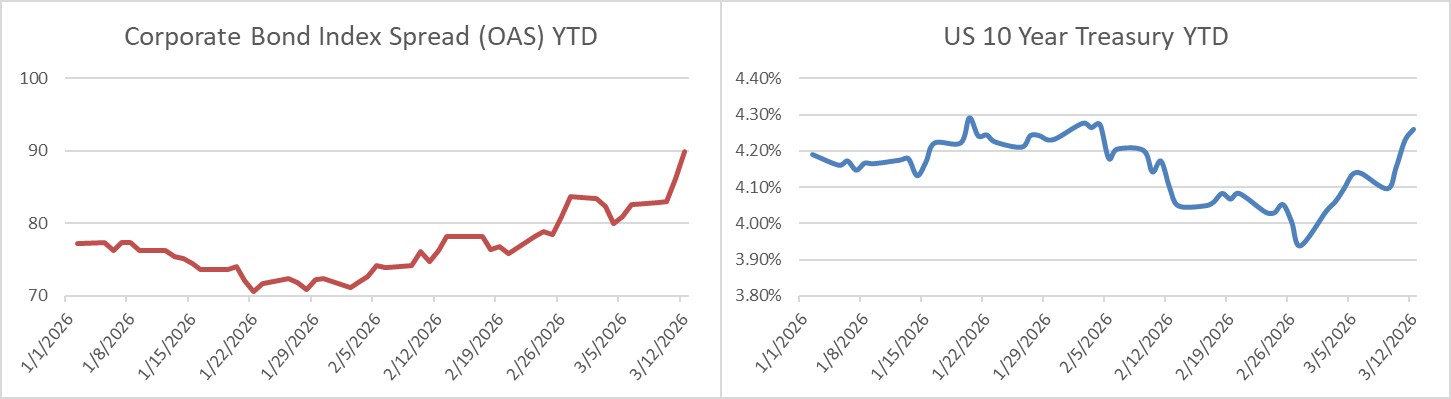

Credit spreads were meaningfully wider this week through Thursday, though the tone was positive with tighter spreads on Friday morning. The OAS on the Corporate Index closed at 90 on Thursday March 12th after closing the week prior at 83. The 10yr Treasury ended last week at 4.14% and it closed at 4.26% on Thursday evening. Through Thursday, the Corporate Bond Index year-to-date total return was -0.69% and the yield to maturity for the index was 5.11%. It is worth noting that this week was the first time the corporate index yield closed above 5% since the last trading day of July 2025.

Points of Interest

It was another volatile week for risk assets as the conflict with Iran looks as though it could drag on for quite some time. The implication for oil prices has been profound which has led to higher expectations for inflation and lower expectations for consumer spending. There were some meaningful economic releases this week with Personal Income/Spending and Core PCE. These were mostly in line with expectations but the problem is that this data was for the month of January and backward looking in nature. It will be months before we know the full extent of the impact that higher energy prices will have on the economy. Next Wednesday the FOMC will convene and deliver a decision on the policy rate. Interest rate futures are pricing an extremely high probability that the Fed maintains the status quo. In fact, futures are not even pricing in a one full 25bp cut for the entirety of 2026. Expectations can evolve rapidly but we believe that the Fed is on hold for the foreseeable future.

Primary Market

New issue supply was the big story of the week in the credit markets as issuers priced $115bln of new debt versus the estimate of $60bln. It was the second busiest week on record, just trailing the $117bln that was priced in 2020. Amazon, Honeywell and Salesforce led the way with three jumbo deals that accounted for $78bln of the total. Amazon’s $37bln deal on Tuesday was the 4th largest of all time and helped reach a new daily record for the US primary market of $65.75bln. Remarkably, Amazon returned to market in Europe on Wednesday pricing €14.5 billion, the largest bond deal ever for that currency. Syndicate desks are looking for around $40bln of issuance next week. Year-to-date new issue supply stood at $565bln through the end of the week.

Flows

According to LSEG Lipper, for the week ended March 10th, short and intermediate investment-grade bond funds reported a net inflow of +$3.28bln. This was the 15th consecutive week of inflows. 2026 year-to-date flows into investment grade were +$36.5bln.

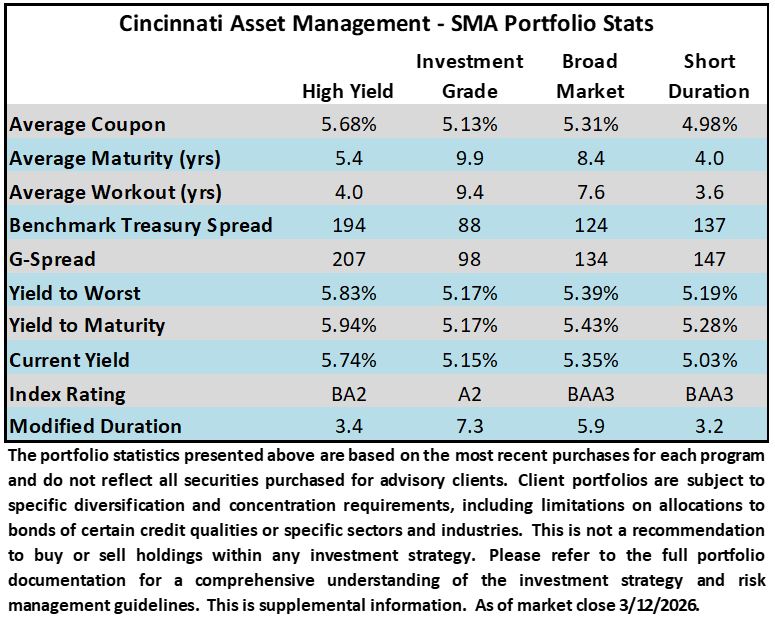

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.