(Bloomberg) High Yield Market Highlights

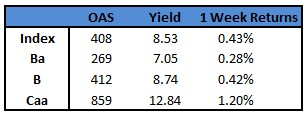

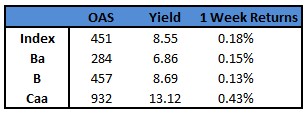

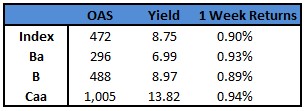

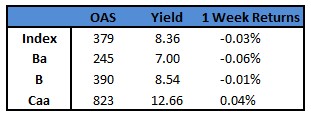

- The US junk-bond rally stalled after data showing a resilient labor market renewed concerns that the Federal Reserve may not stop its interest-rate hikes after the quarter-point move expected next week. The securities posted a modest loss of 0.03% on the week as yields rose seven basis points to 8.36. The weakness extended across ratings as CCC yields jumped nine basis points to 12.66% and BB yields 11 basis points to 7%, the most in two weeks.

- Though the rally paused on Thursday after the labor data, tightening spreads, easing recession concerns and steadily declining inflation continued to draw cash into the market.

- US high-yield funds reported cash inflows of $2.22b for week ended July 19, the first in three weeks, driving demand for new bonds.

- The primary market revived, pricing more than $3b this week, driving month-to-date tally to almost $4b.

- The recent rally was primarily fueled by expectations the Fed’s move in the next meeting would be its last.

(Bloomberg) Goldman Sachs Says This Yield Curve Inversion Is Different

- While the deeply inverted yield curve has stoked anxiety among investors about the prospect of a recession, Goldman Sachs Group Inc. has a different message: stop worrying about it.

- “We don’t share the widespread concern about yield curve inversion,” Jan Hatzius, the bank’s chief economist wrote in a note Monday, cutting his assessment of the probability of a recession to 20% from 25%, following a lower-than-expected inflation report last week.

- Hatzius stands in opposition to most investors who point out that the curve inversion has an almost impeccable track record of foretelling economic downturns. The three-month T-bills yielded more than 10-year notes before each of the past seven US recessions. Currently, the short-term yields are more than 150 basis points above the longer-maturity notes, close to the biggest inversion in four decades.

- Normally, the curve is upward sloped because investors demand higher compensation — or term premium — for holding longer-maturity bonds than short-term ones. When the curve turns upside down, it means investors are pricing in rate cuts large enough to overwhelm the term premium, such a phenomenon only occurs when recession risk becomes “clearly visible,” Hatzius explained.

- This time, though, things are different, the economist said. That’s because term premium is “well below” its long-term average, so it takes fewer expected rate cuts to invert the curve. In addition, as inflation cools, it opens “a plausible path” to the Federal Reserve easing up on interest rates without triggering a recession, according to Hatzius.

- When economic forecasts became overly pessimistic, Hatzius added, they put more downward pressure on longer-term rates than justified.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.