CAM High Yield Weekly Insights

(Bloomberg) High Yield Market Highlights

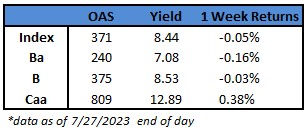

- US junk bonds lost some momentum on renewed concerns that strong macro data will pressure the Federal Reserve to raise rates again, prolonging the most aggressive policy tightening in decades. Junk bonds posted a modest loss of 0.1% on Thursday, on pace to end the two-week gaining streak. Yields jumped nine basis points to 8.44%, the biggest one-day increase in more than two weeks, after rising steadily in three of the last four sessions.

- Gross domestic product accelerated, orders for business equipment were stronger-than-expected and unemployment claims were lower despite an aggressive interest-rate hike campaign with rates at a 22-year high. Fed Chair Jerome Powell said the central bank could raise or hold in September, depending on the data.

- The softness extended across ratings in the US high yield market. The week-to-date losses in single-Bs are 0.03% and BBs 0.16%.

- CCCs, the riskiest part of the US high yield market, bucked the broad trend. CCCs are heading toward third consecutive week of gains, with week-to-date returns at 0.38%, after rallying for straight sessions.

- The gains in CCCs were partly fueled on expectations that the economy will dodge recession.

- “The staff now has a noticeable slowdown in growth starting later this year in the forecast, but given the resilience of the economy recently, they are no longer forecasting a recession,” Powell said Wednesday during a press conference following a policy meeting.

- US high yield funds reported an outflow of $376m for week ended July 26.

- The primary market was steadily building up, though a tad cautiously, as US borrowers took advantage of strong technicals, namely light supply.

- New bonds were inundated with demand as investors looked for new paper amid thin supply.

(Bloomberg) Fed Raises Rates as Powell Keeps Options Open for Future Hikes

- The Federal Reserve resumed raising interest rates and Chair Jerome Powell left open the possibility of further hikes, which he emphasized will depend on incoming data that has recently signaled a resilient US economy.

- After pausing rate increases in June, policymakers lifted borrowing costs again at their policy meeting on Wednesday for the 11th time since March 2022 to curb inflation. The quarter percentage-point hike, a unanimous decision, boosted the target range for the Fed’s benchmark federal funds rate to 5.25% to 5.5%, the highest level in 22 years.

- While Powell pointed to encouraging signs that the Fed’s rate hikes are working to curb price pressures, he reiterated that policymakers have a long way to go to return inflation to their 2% goal.

- The Fed chief refused to be pinned down on when officials may hike again, citing a raft of economic reports due before the Fed’s next meeting in September, including two jobs reports, two reports on consumer-price inflation and data on employment costs.

- “All of that information is going to inform our decision as we go into that meeting,” he said. “It is certainly possible that we would raise [rates] again at the September meeting, if the data warranted. And I would also say it’s possible that we would choose to hold steady at that meeting.”

- Markets took the decision in stride. Swaps traders held fairly steady the probability they see of the Fed hiking rates by an additional quarter point before year’s end. The pricing implies just slightly over 50% chance of another bump higher before the Fed tightening cycle ends.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.