Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were -$3.4 billion and year to date flows stand at -$44.0 billion. New issuance for the week was $0.9 billion and year to date issuance is at $68.9 billion.

(Bloomberg) High Yield Market Highlights

- U.S. junk bonds are headed toward the fourth straight weekly loss as investors pull cash out of high-yield funds amid growing concerns that the economy is headed toward a recession. Yields are hovering near a two-year high of 8.56% and spreads at a 21-month high of +525bps. Barclays Plc’s Brad Rogoff said in a note Friday that high inflation will likely cause the fundamentals supporting the high-yield market to “deteriorate,” putting pressure on “lower-margin or more-leveraged companies.”

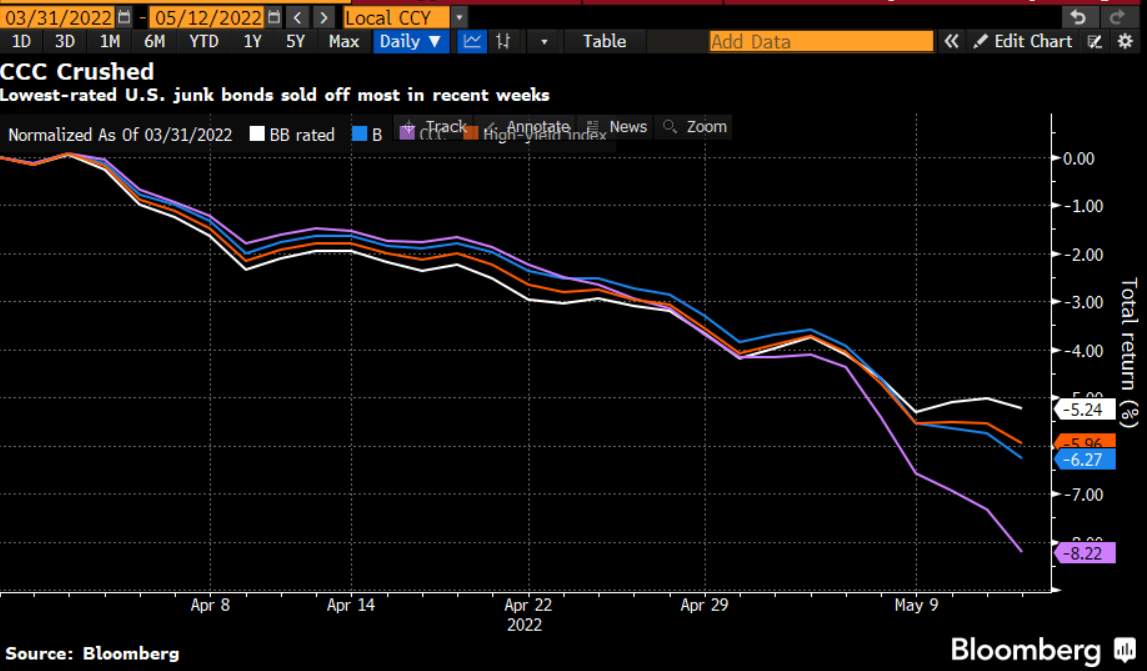

- “The average weighted debt to EBITDA leverage for CCCs is 10.5 times, with 1.8x interest cover indicating unsustainable capital structures over the next two years,” S&P Global wrote on Thursday. CCC yields were close to breaching the 13% level and spreads were near distressed levels, closing at +966bps as tightening financial conditions fuel worries about default risk.

- U.S. high yield funds saw an outflow for week.

- The junk bond primary market was virtually nonexistent amid rising yields and fears of slowing economic growth. Month-to-date issuance is at a modest $9.25b, making it the slowest June in more than a decade.

- JPMorgan revised its junk-bond supply forecast for 2022 to $175b from the earlier estimate of $425b made in November.

(Bloomberg) Powell Says Soft Landing ‘Very Challenging,’ Recession Possible

- Federal Reserve Chair Jerome Powell gave his most explicit acknowledgment to date that steep rate hikes could tip the US economy into recession, saying one is possible and calling a soft landing “very challenging.”

- “The other risk, though, is that we would not manage to restore price stability and that we would allow this high inflation to get entrenched in the economy,” Powell told lawmakers on Wednesday. “We can’t fail on that task. We have to get back to 2% inflation.”

- The Fed chair was testifying before the Senate Banking Committee during the first of two days of congressional hearings. In his opening remarks, Powell said that officials “anticipate that ongoing rate increases will be appropriate,” to cool the hottest price pressures in 40 years.

- “Inflation has obviously surprised to the upside over the past year, and further surprises could be in store. We therefore will need to be nimble in responding to incoming data and the evolving outlook,” he said.

- Powell’s remarks reinforced comments at a press conference last week after he and his colleagues on the Federal Open Market Committee raised their benchmark lending rate 75 basis points — the biggest increase since 1994 — to a range of 1.5% to 1.75%.

- “We understand the hardship high inflation is causing,” Powell said Wednesday. “We are strongly committed to bringing inflation back down, and we are moving expeditiously to do so.”

- “Financial conditions have tightened and priced in a string of rate increases and that’s appropriate,” Powell said in response to a question following his opening remarks. “We need to go ahead and have them.”

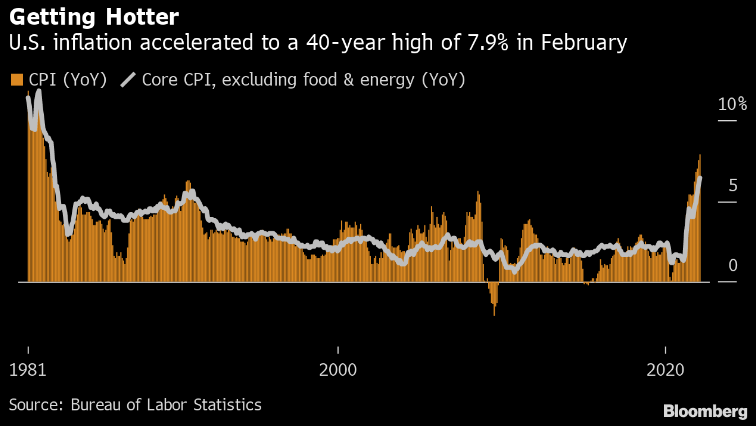

- The Labor Department’s consumer price index rose 8.6% last month from a year earlier, a four-decade high. University of Michigan data showed US households expect inflation of 3.3% over the next five to 10 years, the most since 2008 and up from 3% in May.

- The rising cost of living has angered Americans and hurt the standing of President Joe Biden’s Democrats with voters ahead of November congressional midterm elections.

- Fed officials have admitted that they were too slow to tighten and are now trying to front-load rate increases in the most aggressive policy pivot in decades.

- While a recession isn’t in the Fed’s forecast, economists are increasingly flagging the likelihood of a downturn sometime in the next two years.

- Former New York Fed President Bill Dudley said in a Bloomberg Opinion column Wednesday that a recession is “inevitable” within the next 12 to 18 months. An economist at the Fed, Michael Kiley, said in a paper Tuesday that the risk of a large increase in the unemployment rate is above 50% over the next four quarters, based on a simulation incorporating inflation data, unemployment, corporate bond yields and Treasury yields.

- While he said that he did not see the likelihood of a recession as particularly elevated right now, he said that it was “certainly a possibility. It is not our intended outcome at all,” noting that events in the last few months have made it harder for the Fed to lower inflation while sustaining a strong labor market.

- A soft landing “is our goal. It is going to be very challenging. It has been made significantly more challenging by the events of the last few months — thinking there of the war and of commodities prices and further problems with supply chains.”

- “The tightening in financial conditions that we have seen in recent months should continue to temper growth and help bring demand into better balance with supply,” he said.

- Policy makers’ latest forecasts, released last week, show the level of rates roughly doubling in the second half of the year to a target range of 3.25% to 3.5%. They saw rates peaking next year at 3.8%.

- Officials have also begun shrinking their massive balance sheet. The combined impact of higher borrowing costs and so-called quantitative tightening is expected to come at some cost to jobs.

- Unemployment was near a 50-year low of 3.6% last month and Fed officials forecast it rising to 4.1% by the end of 2024, when they see rates peaking at 3.8%. Inflation was projected to decline toward their 2% goal by then from current readings of more than three times that level, according to the gauge that the Fed targets.