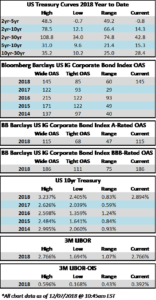

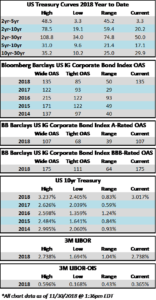

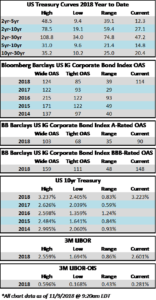

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were -$1.8 billion and year to date flows stand at -$55.3 billion. New issuance for the week was zero and year to date HY is at $162.5 billion, which is -41% over the same period last year.

(Bloomberg) High Yield Market Highlights

- Continued weakness in oil and stock markets will keep pressure on high yield bonds

- Index yield rose to 7.92%, highest since April 12, 2016

- Average yield on BB rated bond rose to 6.24%, highest since February 2016

- Trading volume was slightly above average for the time of year

- S. corporate high-yield funds posted a fifth consecutive week of outflows

- Junk index return was -1.28% on Thursday, the fifth straight decline

- High yield has lost 2.21% so far this month and is down 2.16% YTD

- No new high-yield bond issues priced MTD

- December could be first month in 10 years with no bond sales

- Key drivers of U.S. junk bonds — low default rate, steady GDP growth, corporate cash flow, earnings — holding firm

(Bloomberg) Community Health, Tenet Notes Slip on Judge’s Obamacare Ruling

- Tenet Healthcare Corp. and Community Health Systems Inc. were among the biggest decliners in the high-yield market as hospitals sink after a federal judge in Texas ruled that Obamacare is unconstitutional.

- Tenet’s 7% senior unsecured 2025 bonds slid 2.25 cents on the dollar to 94, while its 8.125% bonds due 2022 dropped 2.125 cents to 100.75, according to Trace

- Community’s 6.25% notes due 2023 fell 1.25 cents to 92

- The judge’s ruling brings the constitutionality question around the ACA back into the political arena which creates another “known-unknown” for healthcare investors, “especially though involved in rural hospitals operators and Medicaid managed care companies,” Mike Holland of Bloomberg Intelligence said in an interview

- “The uncertainty around how and when this plays out will weigh on asset prices until the divided Congress comes up with a fix,” Holland said

(Bloomberg) Charter Settles N.Y. Internet Suit for Record $174 Million

- Charter Communications Inc. agreed to pay $174.2 million to settle consumer fraud claims by the state of New York, which accused the cable provider of ripping off customers with promises of faster internet speeds than the company knew it could possibly deliver.

- The accord is believed to be the largest-ever payout to consumers by an internet service provider in U.S. history, New York Attorney General Barbara Underwood said in a statement Tuesday. The state claimed subscribers to the company’s premium plan received internet speeds as much as 70 percent slower than guaranteed in advertisements by Time Warner Cable, which Charter acquired in 2016 and renamed Spectrum.

- The settlement marks another black eye for an industry that has long been ranked poorly by consumers for its lackluster customer service.

- The pact includes $62.5 million in direct refunds to 700,000 consumers and provides about 2.2 million subscribers with more than $100 million in premium channels and streaming services, according to the attorney general’s statement. Charter also agreed to implement business reforms as part of the settlement, which will set the stage for similar marketing and business changes across the broadband industry, the attorney general’s office said.

(New York Times) Sprint, T-Mobile Deal Gets Green Light From U.S. Regulators

- A federal government committee and other top regulators in the United States have approved the proposed merger between T-Mobile and Sprint, paving the way for a union between the country’s third- and fourth-largest wireless operators.

- The Committee on Foreign Investment in the United States — a body that reviews foreign investments in the United States for national security threats — the Department of Justice, the Department of Homeland Security, and the Department of Defense all agreed to the $26.5 billion deal, T-Mobile said in a statement.

- Some investors, consumer advocates and government officials opposed the merger, claiming that the new telecommunications giant would limit customer choices and result in high prices for consumers.

- Proponents of the deal said it would make the combined company, with about 100 million customers, a competitor that would be able to go toe-to-toe with AT&T and Verizon in the battle to dominate the next frontiers of wireless technology in the United States. John Legere, T-Mobile’s chief executive, has argued that he would “lower prices to attract new customers.”

- The combination would still need to secure approval from the Federal Communications Commission, which has scrutinized a possible T-Mobile-Sprint merger before. In 2014, regulators at the F.C.C. rejected a proposed merger, concluding that effectively reducing the American wireless market to three major carriers from four would not be good for consumers.

- The deal remains subject to other regulatory approvals as well. If the two companies receive those approvals, the deal is expected to close during the first half of 2019, according to T-Mobile.

(Natural Gas Intelligence) Cheniere’s Sabine Pass LNG Train 6 Near FID as Petronas Contracts for 20-Year Supply

- Cheniere Energy Partners LP on Tuesday said it has secured another liquefied natural gas (LNG) supply contract that may help to advance building the sixth train at the Sabine Pass export facility in Cameron Parish, LA.

- Petronas LNG Ltd., a subsidiary of Malaysia’s state-owned Petroliam Nasional Berhad, aka Petronas, made the sale and purchase agreement (SPA) with Cheniere’s Sabine Pass Liquefaction LLC for 1.1 million metric ton/year over 20 years on a free-on-board basis.

- The SPA is subject to a final investment decision (FID) by Cheniere to build Train 6 at the facility, which has been exporting gas overseas since 2016.

- “Petronas is one of the largest and most experienced participants in the global LNG market, and we are pleased to have it as our newest foundation customer at Sabine Pass, supporting Train 6,” Cheniere Partners CEO Jack Fusco said.

- “This 20-year agreement with Sabine Pass Liquefaction continues our momentum on Train 6, where early engineering, procurement, and site preparation activities have recently commenced ahead of a final investment decision.”