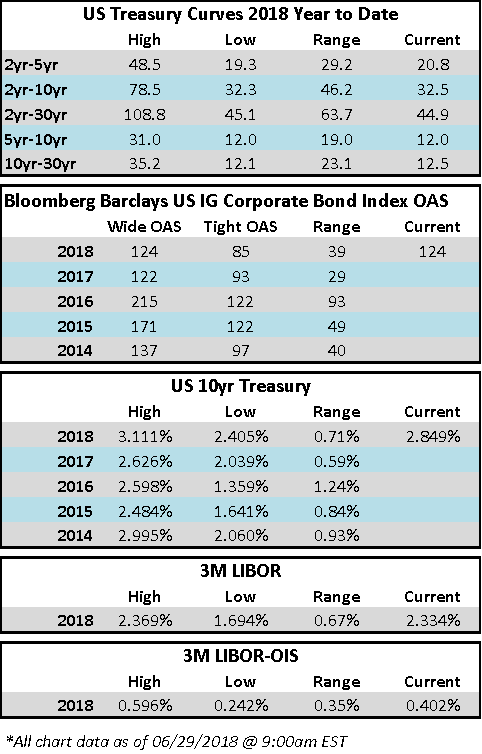

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $1.2 billion and year to date flows stand at -$33.0 billion. New issuance for the week was $1.8 billion and year to date HY is at $108.5 billion, which is -25% over the same period last year.

(Bloomberg) High Yield Market Highlights

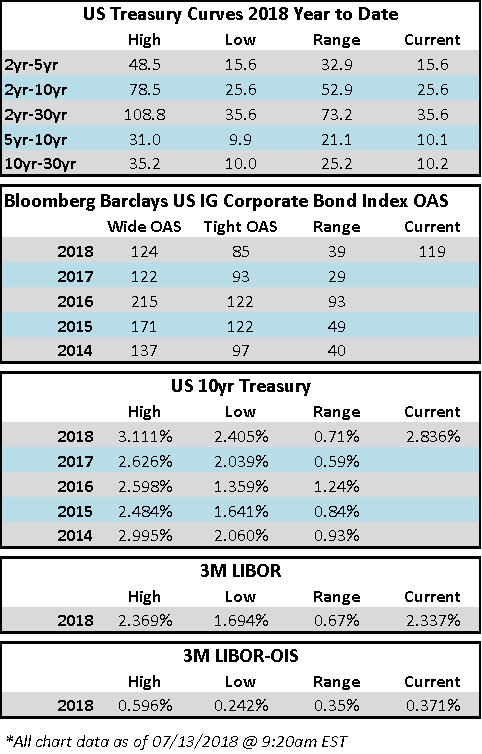

- The spread on the riskiest end of the junk bond market plunged to a four-year low as yields fell across the board and investors allocated fresh funds to high yield.

- Spreads tightened in four of the last five sessions across ratings

- Triple-C spread tightened most, closing at a 4-year low of +556

- Junk yields dropped to a 2-week trough, with CCC yields closing at a 3-week low as the S&P 500 closed at a 5-month high and the VIX dropped in four of the last five sessions to hit a 3-week low

- Investors ignored the hype and hoopla surrounding the trade conflict as high yield retail funds reported cash inflows

- Lipper reported an inflow of $1.8b for week ended July 11, the biggest inflow since April

- YTD supply is down 25%

- CCCs beat BBs and single-Bs with YTD returns of 3.65%

- CCCs outperformed investment-grade bonds, which are down 2.56% YTD

(MarketWatch) U.S. oil sees steepest one-day percentage decline in more than a year

- Oil futures finished sharply lower Wednesday, with the U.S. benchmark registering its sharpest daily slump in about 13 months as fears of flagging demand and renewed production from Libya overshadowed a report showing the biggest weekly drop in domestic crude supplies in nearly two years.

- August West Texas Intermediate crude the U.S. benchmark, fell 5%, to $70.38 a barrel on the New York Mercantile Exchange—its lowest finish since June 25. The drop marked the worst percentage decline for a most-active contract since June 7 of 2017 and the steepest fall on a dollar basis since Sept. 1 of 2015, according to WSJ Market Data Group.

- “Market players are taking profits after reports of the return of Libyan crude oil,” possible waivers for U.S. sanctions on Iranian oil and renewed trade war fears, said Phil Flynn, senior market analyst at Price Futures Group.

- There is also speculation that U.S. President Donald Trump “will hammer Russia on raising oil production” in an effort to push prices lower, and that has “traders running for cover,” he said.

- The losses come even as the Energy Information Administration reported Wednesday that domestic crude supplies plunged by 12.6 million barrels for the week ended July 6.

- “The biggest draw since September 2016 should be a wake up call for the U.S.,” said Flynn. “We are in a tightening supply situation that is not going to get better soon.” The EIA reported a climb in crude supplies last week, but that followed three-consecutive weeks of hefty declines.

- Meanwhile, Libya’s state-run National Oil Corp. lifted force majeure on eastern oil ports on Wednesday after the ports were handed back from an armed faction, paving the way for a resumption of full production.

- “Resumption of exports from Libya trumps one week of bullish EIA data,” said James Williams, energy economist at WTRG Economics. “That reduces fear of shortages with so little spare production capacity worldwide.”

(Bloomberg) Dish Network Gets Distress Signals From FCC

- Hurry up is the message the Federal Communications Commission had for Dish Network Corp. in a July 9 letter asking for more detail about how Dish plans to use the $40 billion of spectrum it acquired in recent years to build a wireless network. Dish faces an accelerated March 2020 deadline to use-or-lose some of the spectrum after missing previous cutoff dates.

- Chairman Charlie Ergen has invested heavily in wireless spectrum as he pivots the company he co-founded away from its declining satellite TV business. He’s funneling cash from the old business to fund the new one, and bondholders are worried they’ll be left behind.

- The agency said it’s following up on recent meetings between Ergen and FCC Chairman Ajit V. Pai with more more than a dozen questions about Dish’s plans to build out “spectrum that is apparently lying fallow.” Bond and stock holders might want the answers, too: The queries include the timing of critical milestones, the service Dish intends to provide and what industry standard technology might be used. Officials at Dish didn’t immediately respond to a request for comment.

(Fierce Telecom) Frontier launches new cloud-based UCaaS offering for businesses

- Frontier Communications is now offering its customers a cloud-based unified communications-as-a-service to help them migrate their voice services to the cloud.

- Frontier’s AnyWare UCaaS allows small- to medium-sized business and enterprise customers to lease phones and equipment without having to worry about stranding investments in outdated gear.

- The scalable and customizable platform can be adapted for each company’s specific needs. Customers are able to save money by putting former hardware functions into the cloud while also reducing the cost of investing in and maintaining on-premise PBX systems.

- The UCaaS business has been booming of late. In the most recent fourth quarter, more than 300,000 subscriber seats were added to the global installed base, which is now growing by 29% per year, according to Synergy Research. Mitel and RingCentral were the top-two UCaaS companies in Synergy Research’s fourth quarter report. Combined, the two companies accounted for more than half of all the growth in the fourth quarter.

- Other UCaaS competitors in Frontier’s footprint include Charter Spectrum, Comcast and 8×8.