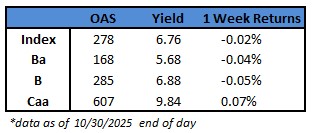

Credit spreads remained range bound this week with The Index just slightly wider through Thursday. The OAS on the Corporate Index closed at 73 on Thursday January 29th after closing the week prior at 72. The 10yr Treasury closed last week at 4.23% and exhibited almost no change whatsoever throughout the week before closing at 4.23% on Thursday evening. Through Thursday, the Corporate Bond Index year-to-date total return was +0.24% while the yield to maturity for the index was 4.85%.

Points of Interest

The biggest news of the week came on Friday morning when President Donald Trump said that he intends to nominate Kevin Warsh to be the next chair of the Federal Reserve. Warsh still needs to be confirmed by the Senate but he is widely viewed as a relatively safe pick given his past experience serving on the US Central Bank’s Board of Governors from 2006 to 2011. Recall that Jerome Powell’s term expires in May.[i]

The FOMC also met this week and made no changes to its policy rate, as expected. This pause came after three consecutive meetings where the committee elected to lower rates. 10 of the 12 voting members chose to pause with only 2 dissenters that were in favor of lower rates.

This creates a tough situation for Kevin Warsh and we are not envious of the job that he has in front of him. On one hand he has a President that has repeatedly called for a policy rate up to 3% lower than its current level (this would be the equivalent of a dozen 25bp rate cuts!). On the other hand, Warsh inherits an economy that has continued to perform and a job market that has experienced slowing growth but has still managed to maintain an unemployment rate that has shown signs of stabilization near historical lows. With the December dot plot showing a median consensus of just two cuts by the end of 2027 it is hard to envision a scenario where Kevin Warsh will be able to deliver lower rates and appease the President. In any case, we are hopeful that the Fed continues its time-honored tradition of independence and allows the data to guide its decision-making process.

There is a smattering of economic data next week but the major highlights are JOLTS job data on Wednesday followed by the Nonfarm Payroll report on Friday morning.

Primary Market

The primary market picked up this week as borrowers priced $36.9bln of new debt topping the high end of estimates. This helped push the monthly total for January to $208bln, making it the 5th busiest month of all-time. Syndicate desks are looking for another busy week to start the month of February with the average supply estimate coming in at around $40bln.

Flows

Investment grade bond inflows hit a five-year high in the latest week. According to LSEG Lipper, for the week ended January 28, short and intermediate investment-grade bond funds reported a net inflow of +$5.4bln, the most since the week ended February 3rd, 2021. This was the 9th consecutive week of inflows. 2026 year-to-date flows into investment grade were +$14.46bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

[1] Bloomberg, January 30 2026, “Trump Picks a Reinvented Warsh to Lead the Federal Reserve”