(Bloomberg) High Yield Market Highlights

- US junk bond yields edged up, looking through trade tariffs noise and mixed earnings, with Walmart posting disappointing forecasts on Thursday. Traders awaited manufacturing PMI data due later today for clues on the interest-rates path.

- Higher yields continued to bring borrowers into the market

- Four companies sold a little more than $3b in just three sessions to drive the month’s volume to $16b

- Spreads remain tight, bolstered by strong technicals and demand for all-in yield, strategists Brad Rogoff and Dominique Toublan from Barclays wrote this morning

- There is a lack of near-term catalyst to materially disrupt credit markets, they added

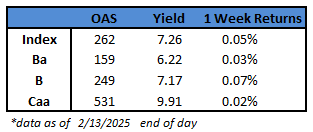

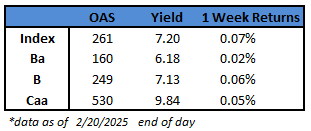

- Yields closed at 7.20% and spreads at 261 basis points

- CCC yields closed at 9.84% and spreads unchanged at 530

(Bloomberg) Fed Minutes Signal Officials on Hold Until Inflation Improves

- Federal Reserve officials in January expressed their readiness to hold interest rates steady amid stubborn inflation and economic-policy uncertainty.

- “Participants indicated that, provided the economy remained near maximum employment, they would want to see further progress on inflation before making additional adjustments to the target range for the federal funds rate,” minutes from the Federal Open Market Committee’s Jan. 28-29 meeting showed.

- The minutes, released Wednesday in Washington, said “many participants noted that the committee could hold the policy rate at a restrictive level if the economy remained strong and inflation remained elevated.”

- Officials held the Fed’s benchmark policy rate in a range of 4.25%-4.5% at that gathering.

- The record of the meeting underscored the cautious approach Fed policymakers are taking after lowering interest rates by a percentage point in the closing months of 2024. Several officials have said they’d like to see inflation cool further toward the Fed’s 2% target before backing another cut.

- Investors are currently pricing in one rate cut in 2025, with the possibility of a second, according to futures markets.

- Policymakers are watching the rollout of Trump’s economic-policy plans and how they might shape the economy. Trump is pushing an agenda that includes an increased use of tariffs on US trading partners and an immigration crackdown, both of which could affect the outlook for inflation, the labor market and economic growth.

- While characterizing risks in the economy as roughly balanced, policymakers “generally pointed to upside risks to the inflation outlook,” the minutes said.

- “Participants cited the possible effects of potential changes in trade and immigration policy, the potential for geopolitical developments to disrupt supply chains, or stronger-than-expected household spending,” the minutes showed.

- Still, officials expected that “under appropriate monetary policy” inflation would continue to decline toward their 2% goal.

- Some policymakers also noted that difficulties in fully removing seasonal distortions from inflation data at the start of the year could make the figures “harder than usual to interpret.”

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.