CAM Investment Grade Weekly Insights

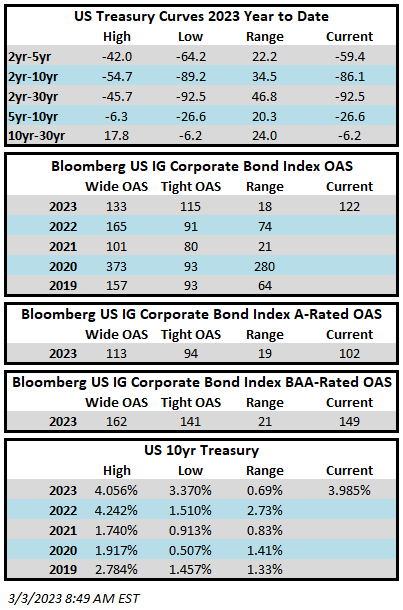

Investment grade credit spreads are set to finish the week tighter amid a strong market tone this Friday morning. The fact that spreads moved tighter this week is an impressive feat amid higher Treasury yields and an extremely active primary market. The Bloomberg US Corporate Bond Index closed at 122 on Thursday March 2 after having closed the week prior at 123. The 10yr Treasury closed above 4% for the first time this year on Thursday but it has since fallen below that threshold as we go to print on Friday morning. Through Thursday the Corporate Index had a YTD total return of -0.05% while the YTD S&P500 Index return was +4.0% and the Nasdaq Composite Index return was +9.7%.

The slate of economic data this week was lighter relative to recent weeks but the data flow continued to have market participants erring on the side of caution with regard to Fed policy. We would argue that this should have always been the case but many prognosticators seemed to be holding on to the belief that the Fed would be delivering rate cuts in the second half of 2023. Although a reversal in policy later this year cannot be ruled out we think the prevailing mood has shifted over the past two weeks and at this point the consensus view is that the Fed will indeed be hesitant to slash its policy rate until it is very clear that inflation will not be a longer term concern. Again, we think the Fed has been transparent about how this process would play out, but the market sometimes hears what it wants to hear. Fed officials continued to be hawkish in interviews and speeches this week which should reinforce this view.

The primary market remains healthy as it had its busiest week of the year, not in terms of volume but in terms of the number of deals and tranches. Volume too was impressive at just over $46bln printed relative to the high end of estimates which was $40bln. Year to date, $310.74bln of new debt has been priced. Syndicate desks are estimating $35bln in supply for the week ahead.

Investment grade credit reported its largest inflow in almost two months. Per data compiled by Wells Fargo, inflows for the week of February 23–March 1 were +5.0bln which brings the year-to-date total to +$50.4bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.