CAM Investment Grade Weekly Insights

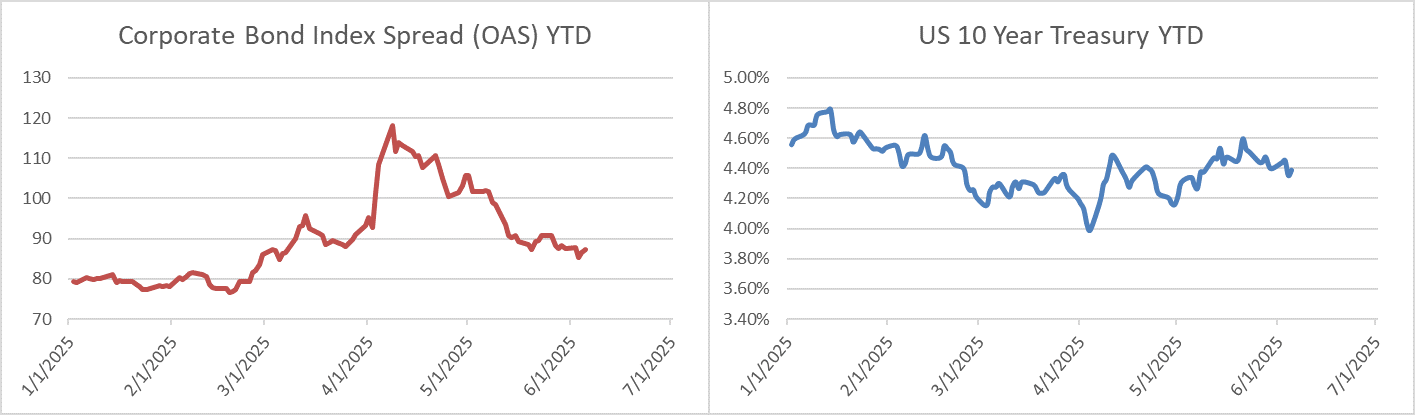

Credit spreads were little changed this week. The US Corporate Bond Index closed last week at 88 and it was at the same level when the market closed this Thursday. The 10yr Treasury yield was also nearly unchanged this week through Thursday moving from 4.40% lasts week to 4.39% through Thursday’s close. The benchmark rate had moved up to 4.48% by midday Friday on the back of a “decent” Friday morning payroll report. Through Thursday, the Corporate Bond Index year-to-date total return was +2.53% while the yield to maturity for the Index closed the day at 5.21%.

Economics

There was plenty of economic news this week. JOLTS kicked things off coming in slightly better than expectations. Data showed that job openings increased in April and the March number caught an upward revision. ISM manufacturing missed to the downside for the month of May, remaining in contraction territory. Construction spending posted a big miss to the downside, and was much lower than expected for the month of April. Lousy spring weather could have played a part but so too could tariff related fears, as total construction spending through the April report was down 1.5% relative to the same time period in 2024. ISM services also came in on the low side, and remained in contraction. The price component of ISM release increased however which could be a negative indicator with regard to future inflation readings. Finally on Friday we got some relatively good news for the labor market as the release showed that nonfarm payrolls for the month of May increased by 139k (126k survey) and the unemployment rate remained steady at 4.2%. There were some more bearish economists looking for a sub-100k print. This report likely gives the Fed some room to continue to delay its next cut. On the downside the job numbers for the two previous reports were revised to the tune of -95k which takes some shine off of the numbers from March and April. Taking it altogether it would be fair to say that the data this week continued to paint a picture of a slowing economy but one that is declining in a moderate fashion that looks like more of a soft-landing scenario at this juncture.

Across the pond, the ECB elected to cut its policy rate by 25bps. This makes 200bps of cumulative cuts for the European Central Bank since June of 2024. The ECB is now well ahead of the FOMC’s 100bps of cumulative cuts. Commentary from ECB president Lagarde indicated that central bank is near the end of its cutting cycle.

After two weeks of a bevy of economic releases, next week is on the lighter side, but there are a couple of highlights with CPI and PPI on Wednesday and Thursday, respectively. Looking further ahead, the June FOMC rate decision is on Wednesday the 18th. Barring an unforeseen exogenous shock over the next dozen days it is all but certain that the Fed will elect to hold rates steady at its June meeting.

Primary Market

It was an active week for the IG primary market but total volume of $26.2bln fell short of the $30bln estimate. New issue concessions remained sparingly narrow as most deals in recent weeks have been priced to perfection. Dealers are looking for $25bln in new supply next week with most activity centered on Monday and Tuesday. Year-to-date issuance through this week stood at $814.7bln which was +4% ahead of 2024’s pace.

Flows

According to LSEG Lipper, for the week ended June 4, investment-grade bond funds reported their largest inflow of the year, a whopping +$4.11bln. Total year-to-date flows into investment grade were +$14.02bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.