(Bloomberg) High Yield Market Highlights

- US junk bonds bounced back from Wednesday’s selloff as yields and spreads declined, driving modest gains on a broader risk-on tone as equities recovered on strong corporate earnings and a dip in oil prices.

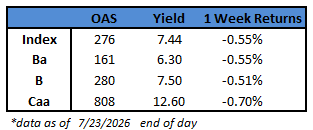

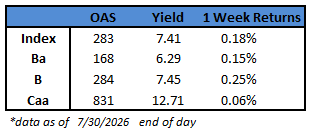

- The recovery was broad-based, with yields and spreads falling across ratings. CCC yields fell 12 basis points to 12.71%, while spreads tightened 9 basis points to 831.

- Market volatility, fueled by continuing hostilities in the Middle East, climbing oil prices and inflation worries kept new borrowers on the sidelines, with just three deals pricing for $3b, spurring a monthly volume of a little more than $18b

- Three PE-backed firms sold bonds this week.

- Solid private demand growth, moderating inflation and strong earnings remain supportive of the credit markets, but hyperscaler weakness is spreading across the broader AI ecosystem, Barclays’ strategists Bradley Rogoff and Dominique Toublan wrote

(Bloomberg) Fed Dissenters Say Rate Hikes Needed to Tame High Inflation

- Three Federal Reserve officials who dissented against Wednesday’s decision to hold interest rates steady warned that waiting too long to act against inflation could risk the need for even more aggressive policy moves later.

- “The longer that high inflation persists, the more challenging and costly it can be to bring it back down,” Cleveland Fed President Beth Hammack said in a statement released Friday.

- Minneapolis Fed President Neel Kashkari said in a separate statement that to manage against the risk of high inflation becoming entrenched, he “would rather tighten policy incrementally as we gather more data on the path of inflation and employment.”

- Lorie Logan, head of the Dallas Fed, said in a statement released later Friday that “modest action in the near term would reduce the likelihood of needing to take sharper action later.”

- Fed officials voted 9-3 this week to leave their benchmark rate unchanged for the fifth consecutive meeting. Policymakers have held their target rate in a range of 3.5% to 3.75% all year. But more officials have expressed support for potential rate increases after renewed tensions in the Middle East and a massive investment boom driven by artificial intelligence have revived inflationary pressures.

- Hammack, Kashkari and Logan, who all would have preferred to raise rates this week, pointed to the various supply shocks helping drive up inflation. Hammack said she sees pressure on the demand side of economy as well. Kashkari said that the Fed’s tools can be successful in fighting inflation driven by “successive supply shocks,” as they were in the late 1970s and early 1980s.

- Logan argued that inflation “appears to be trending toward the mid-2’s, not all the way to 2%” — the rate Fed officials target — even after accounting for the supply shocks and gains in productivity. She said the labor market, spending and financial market conditions suggested policy was not restraining the economy and it was unlikely price pressures would fully cool without some action from the Fed.

- All three officials noted that the economy overall is strong right now.

- The Fed’s preferred inflation measure, the personal consumption expenditures index, fell 0.1% in June, data released Thursday showed. A report earlier this month showed a similar decline in another inflation measure, driven by large declines in gasoline prices. Now, economists warn the inflation relief seen earlier this summer may be short lived after a re-escalation of the Iran war pushed oil prices up again in July.

- Hammack said she did not see policy as “appropriately restrictive” to cool price pressures, and was not confident inflation would return to the Fed’s 2% goal on its own.

- “Now is the time for the FOMC to act to speed the return of PCE inflation to our 2% objective and deliver on our commitment to price stability for the American people,” she said.

- The same three regional bank presidents dissented at the Fed’s April meeting. While they supported the decision to hold interest rates then, they objected to language in the post-meeting statement that suggested the next rate move would likely be a cut.

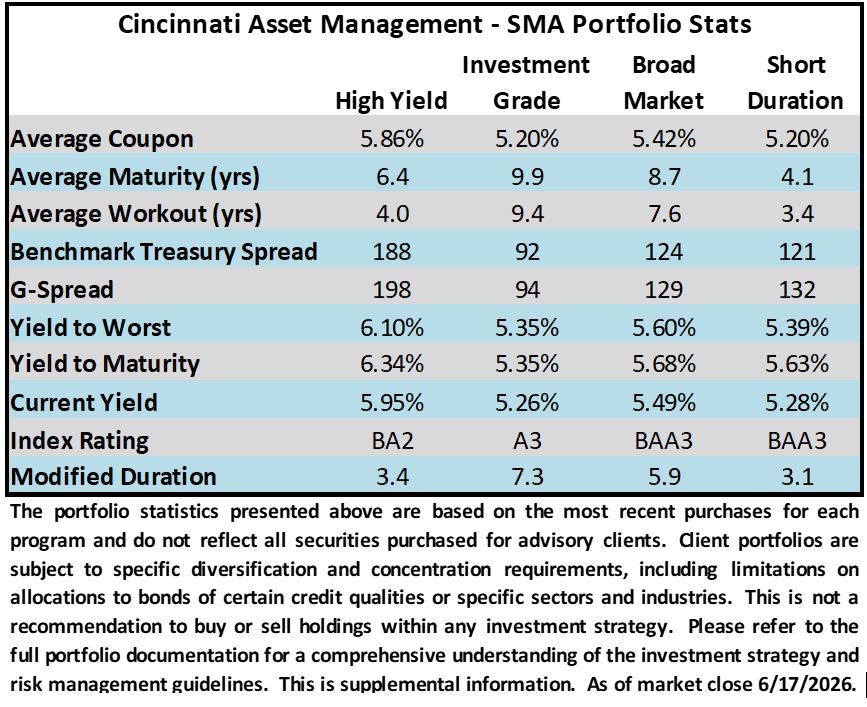

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.