(Bloomberg) High Yield Market Highlights

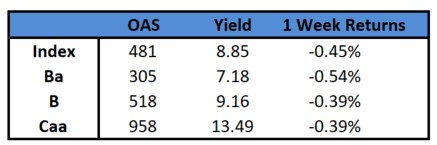

- US junk bonds are headed toward the third straight week of losses and the biggest weekly loss in more than two months, pushing yields to a seven-week high on worries over negotiations to raise the debt ceiling. The week-to-date loss is 0.45%.

- The losses spanned ratings categories. US high yield funds reported an outflow of $1.15b for week ended May 17, the third consecutive week of outflows.

- Yields have risen amid higher inflation expectations and hawkish commentary from Fed officials, while the outlook for economic growth has deteriorated across major developed markets, Barclay’s Brad Rogoff wrote in a note.

- This creates greater uncertainty about the June Fed decision, Rogoff wrote.

- Even as yields rose steadily and nervous investors stayed on the sidelines, the primary market saw a deluge of new issuance, with borrowers rushing to get ahead of any jumps in yields spurred by gridlock in the negotiations to raise the US debt ceiling.

- As US borrowers made a quick dash to the market, the week-to-date tally rose to $3.5b. The month-to-date supply jumped to more than $13b. The year-to-date volume stood at almost $71b.

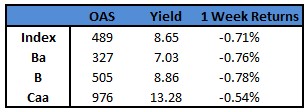

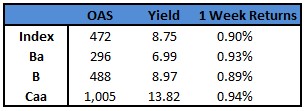

- CCCs have bucked the overall trend as yields dropped on Thursday to 13.49% and has risen by just 6bps week-to-date versus a 35bps jump single B yields and 17bps in BBs.

- BBs posted losses for six days in a row and are on track to see the biggest weekly decline, with week-to-date losses of 0.54%, the biggest since March 10.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.