CAM High Yield Market Note

10/18/2019

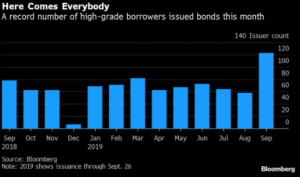

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $1.9 billion and year to date flows stand at $20.0 billion. New issuance for the week was $4.1 billion and year to date HY is at $203.8 billion, which is +33% over the same period last year.

(Bloomberg) High Yield Market Highlights

- A six-day rally in U.S. junk bonds is poised to run out of steam as investors digest more corporate earnings and as stock futures drift on data showing slowing growth in China.

- Returns on BB junk bonds hit a new high of 13.189% as investors continue to scramble for higher-quality junk debt

- BBs are the second best performing asset class in fixed income after BBBs, which have returned 14.31%

- The overall junk bond index extended gains for the sixth straight session to 11.635%. The year-to- date high was 11.809% on September 23

- Issuance has slowed this week as the earnings season keeps companies in blackout

- Junk bond index yields rose 2bps to close at 5.67%, while spreads held steady at 380bps over U.S. Treasuries

- BB yields eased to 3.96% after reaching a six-year low

- CCC yields rose 4bps to 10.97%

- (Bloomberg) Aecom Reaches $2.4 Billion Deal for Management Services Unit

- Aecom, targeted by activist investor Starboard Value, agreed to sell its management services division to a consortium of private equity firms including Lindsay Goldberg and American Securities for $2.4 billion.

- The Los Angeles-based firm, one of the world’s top engineering and design groups, plans to use the proceeds from the sale to reduce debt and to repurchase stock, it said in a statement Monday, confirming an earlier report in Bloomberg News. The transaction is expected to close in the first half of fiscal year 2020, it said.

- “We are extremely pleased with today’s transformative and value-enhancing announcement, which significantly accelerates our planned debt reduction and commitment to repurchase stock,” Michael Burke, AECOM’s chairman and chief executive officer, said in a statement.

- Aecom announced plans to spin off its management services unit in June. It argued at the time that the move would create a leading government services company for its clients, including the U.S. Departments of Defense and Energy, by leveraging its expertise in areas such as intelligence, cyber-security and information technology.

Business Wire) AMC Entertainment Selects Sean Goodman as Its New CFO

- AMC Entertainment announced the hiring of Sean Goodman, currently CFO of Fortune 500 company Asbury Automotive Group (NYSE: ABG), who will commence working with AMC as Executive Vice President – Finance on December 2, 2019. Current AMC CFO Craig Ramsey will retire on February 28, 2020, in a long-envisioned move.

- During the overlap, the two executives will work closely together, and Goodman will assume the Chief Financial Officer title upon Ramsey’s retirement. The Company expects an orderly, easy and seamless transition.

- After an extensive and comprehensive national search, AMC has tapped Goodman, 54, to be Ramsey’s successor. Goodman has more than 30 years of finance experience including leading Financial Planning and Analysis as well as Business Development at Home Depot in Atlanta, was an investment banker at Morgan Stanley in London and worked for Deloitte & Touche in South Africa and New York. He has U.S. public company CFO experience at Asbury Automotive Group. In addition to his almost 20 years working in the United States, Goodman has extensive international work experience in Europe, Asia and Africa.

- In early February, Craig Ramsey will achieve a milestone 25th anniversary in leadership roles at AMC, including having become its CFO in the year 2000. His eventual retirement has long been in the executive succession planning process for AMC.

- Adam Aron, AMC CEO and President said, “I cannot thank Craig Ramsey enough for his longstanding service to AMC, and the many vital contributions he has made as one of our most key executives. Our company has greatly benefited from his distinguished career, which has been marked by integrity, ability and common sense. At the same time, I am absolutely thrilled that we have been able to attract to AMC Sean Goodman who surely will help us to propel AMC forward in the years ahead. As we recruited him to join AMC, the sharpness of his mind, his strategic clarity, his extensive international experience and authentic leadership style were all quite evident. It is a terrific outcome that we have added such a superb top tier talent to AMC’s executive team.”

(Business Wire) Geysers Power Company, LLC Announces Senior Secured Notes Offerings

- Geysers Power Company, LLC (“GPC”), an indirect wholly owned subsidiary of Calpine Corporation and the owner of 13 Geysers geothermal power plants and related assets, announced that it intends to offer Senior Secured Notes, Series A, due 2039 and Senior Secured Notes, Series B, due 2039 in a private placement to qualified institutional buyers. Prior to consummating the notes offerings, GPC and certain other Calpine Corporation subsidiaries (collectively, the “Geysers Entities”) involved in the geothermal power generation business will each be released from current guarantee obligations in respect of Calpine Corporation’s indebtedness and the related liens encumbering the Geysers Assets will be released and no longer available to satisfy creditors of Calpine Corporation. The notes will be guaranteed by the Geysers Entities. The notes and related guarantees will be secured equally and ratably with the indebtedness under a new seven-year senior secured revolving credit facility and a new ten-year senior secured term loan facility in an estimated aggregate principal amount of up to $320.0 million and $400.0 million, respectively (which GPC intends to enter into concurrently with the consummation of this offering) and other indebtedness that is permitted to be secured by such assets, by a first-priority lien on substantially all of GPC’s and the guarantors’ existing and future assets, subject to certain exceptions and permitted liens.

- GPC intends to use the proceeds from the offerings, together with borrowings under the new term loan facility and letters of credit issued under the new revolving credit facility, to (i) fund a debt service reserve account and a major maintenance reserve account, (ii) pay costs associated with the offerings and entry into the new revolving credit facility and the new term loan facility, (iii) pay a dividend to Calpine Corporation (the majority of which Calpine Corporation intends to use to repay a portion of its existing indebtedness, and any excess funds from such dividend may be used by Calpine Corporation for general corporate purposes) and (iv) fund working capital, ongoing capital requirements and general corporate purposes of the Geysers Entities.

(Bloomberg) The Repo Market’s a Mess. (What’s the Repo Market?): QuickTake

(Bloomberg) The Repo Market’s a Mess. (What’s the Repo Market?): QuickTake