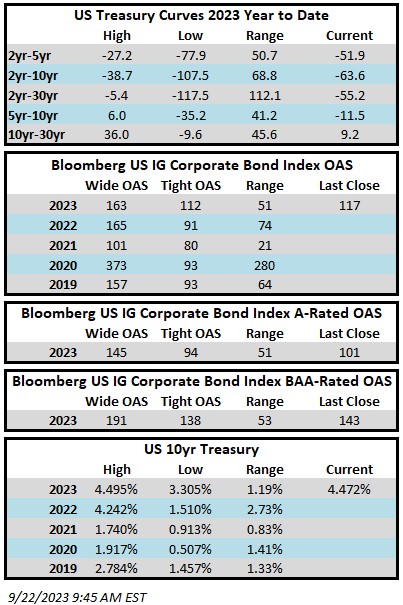

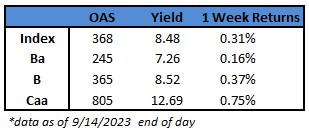

Los diferenciales de crédito con grado de inversión fueron más ajustados durante el tercer trimestre, pero los rendimientos de los bonos del Tesoro subieron, lo que actuó como un importante obstáculo para la rentabilidad. Durante el trimestre, el diferencial ajustado por opciones (Option Adjusted Spread, OAS) en el índice de bonos corporativos de EE. UU. de Bloomberg se redujo en 2 puntos básicos y llegó a 121 después de haber abierto el año con un OAS de 123. Las curvas de los bonos del Tesoro intermedio se inclinaron durante el período, con relativamente pocas variaciones en los bonos del Tesoro a 2 años, mientras que los rendimientos de los bonos del Tesoro a 5 y 10 años subieron significativamente. Las tasas más altas son malas noticias para los rendimientos a corto plazo, pero a largo plazo, la inclinación de la curva es algo que nos gusta ver, ya que crea un entorno más amigable para los inversores en bonos. Las curvas con pendiente positiva maximizan la eficiencia y el potencial de rendimiento de un bono que avanza hacia abajo en la curva de rendimiento a medida que se acerca al vencimiento.

El índice corporativo registró un rendimiento total de todo el trimestre de -3.09 %. La rentabilidad total neta de comisiones del programa de grado de inversión de Cincinnati Asset Management, Inc. (CAM) fue del -2.36 %. Los rendimientos totales el último año se mantuvieron positivos tanto para el índice como para el CAM hasta el final del trimestre.

Actualización de mercado

El rendimiento al vencimiento (yield to maturity, YTM) del índice Bloomberg U.S. Corporate cerró el trimestre en 6.04 %. Aquí hay algunas estadísticas para proporcionar contexto:

- El YTM promedio a 5 años fue del 3.48 %. El índice cerró >6 % menos del 0.7 % de los días hábiles.

- El YTM promedio a 10 años fue del 3.38 %. El índice cerró >6 % menos del 0.4 % de los días hábiles.

- El YTM promedio a 15 años fue del 3.69 %. El índice cerró >6 % menos que el 5.2 % de los días hábiles.

- El YTM promedio a 20 años fue del 4.12 %. El índice cerró >6 % menos que el 7.6 % de los días hábiles.

Con los rendimientos cerca de los máximos del ciclo y las situaciones fundamentales de las empresas en buena forma, creemos que el crédito IG ofrece una propuesta de valor atractiva. También creemos que la desventaja para la clase de activos es limitada debido a estos elevados rendimientos. Los rendimientos del Tesoro podrían subir a partir de aquí o podría haber un aterrizaje forzoso que podría ampliar los diferenciales de crédito, pero el impacto de esos movimientos en los rendimientos disminuye cuando el punto de partida es un rendimiento >6 %, lo que proporciona un colchón significativo para los inversores en bonos.

Creemos que los diferenciales de crédito estaban valorados de forma justa al final del trimestre. La OAS en el índice terminó el trimestre en 121 en relación con sus promedios de 5 y 10 años de 123 y 124, respectivamente. Los inversores son cautelosos respecto de la dirección de la economía estadounidense, por lo que creemos que podría resultar difícil un mayor ajuste de los diferenciales desde los niveles actuales. Sin embargo, existen un par de escenarios que podrían hacer que los diferenciales se ajusten más: 1.) La curva de rendimiento continúa aumentando hasta el punto de que ya no está invertida y/o 2.) La inflación continúa cayendo, coincidiendo con un aterrizaje suave para la economía de EE. UU. Existe también un tercer escenario, que contempla una falta de oferta de nuevos bonos hasta finales de año, lo que podría crear un desajuste entre la oferta y la demanda: si las nuevas emisiones son insuficientes para satisfacer la demanda de los inversores, entonces los diferenciales secundarios podrían reducirse en ausencia de datos económicos negativos. Por el contrario, los diferenciales podrían ampliarse si una política monetaria restrictiva lleva a la economía a una recesión. Creemos que el resultado más probable es que los diferenciales se negocien dentro de un rango relativamente estrecho hasta que haya más certeza entre los inversores sobre la dirección de la economía y las expectativas de inflación. En resumen, con rendimientos elevados del Tesoro y una compensación justa por el riesgo crediticio, creemos que el crédito con grado de inversión sigue siendo atractivo.

Asignación de activos: acciones frente a bonos

A lo largo de 2023, los bonos del Tesoro han subido más, mientras que las acciones han seguido avanzando, registrando rendimientos impresionantes. Esta acción del precio ha puesto de relieve el concepto de prima de riesgo de acciones (equity risk premium, ERP). La ERP es el rendimiento adicional que un inversor obtiene de las acciones en comparación con los bonos por asumir un riesgo adicional en el mercado de valores. Para decirlo en términos matemáticos, la ERP es la diferencia entre el rendimiento de las ganancias del S&P 500 y el rendimiento del Tesoro a 10 años. El siguiente gráfico de la ERP está expresado en términos de puntos básicos.

Actualmente, la ERP se encuentra en su nivel más bajo en cualquier momento de los últimos 20 años. ¿Fortalece esto el argumento a favor de los bonos con grado de inversión, que obtienen un diferencial superior a la tasa libre de riesgo? Creemos que sí, pero vale la pena señalar que la ERP puede volverse negativo; fue profundamente negativo durante un período prolongado durante el período de la burbuja de las puntocom de 1998 hasta principios de 2001.

El efectivo sigue siendo atractivo, pero no tanto

La pregunta más frecuente que hemos seguido recibiendo de inversores individuales durante el año pasado es algo como esto.

“Los rendimientos al 6 % me parecen fantásticos, pero ¿por qué debería asignarlos a bonos corporativos intermedios cuando puedo comprar un Tesoro a dos años al 5 % o un CD a 18 meses al 5.25 %?”

Para ser claros, creemos que los inversores deberían aprovechar la dislocación en el extremo inicial de la curva de rendimiento, pero no deberían hacerlo a expensas de sus objetivos a más largo plazo. Estas tasas altas a corto plazo son un fenómeno del ciclo de subidas de tipos de la Reserva Federal y la curva invertida podría disiparse rápidamente cuando la Reserva Federal cambie de rumbo. Un inversor que asigna en exceso al extremo inicial de la curva corre el riesgo de perder rendimientos mayores un poco más allá de la curva. El objetivo para la mayoría de los inversores debe ser asignar su cartera de manera que se beneficie de tasas altas a corto plazo y al mismo tiempo mantener una exposición a la parte intermedia de la curva de rendimiento para que la cartera pueda cosechar los beneficios de una curva que eventualmente se vuelve a empinar de su estado invertido actual. Un inversor que espere el primer recorte de tipos de la Reserva Federal o espere a que esta operación sea obvia podría perderse muchos frutos maduros en lo que a rentabilidad se refiere.

El tema del riesgo de reinversión sigue siendo de gran actualidad en nuestras conversaciones con los inversores. Comuníquese con uno de nuestros asesores de clientes si desea discutir esto más a fondo o si puede ver parte de nuestro contenido anterior aquí.

Curva de crédito corporativo: un juego de espera

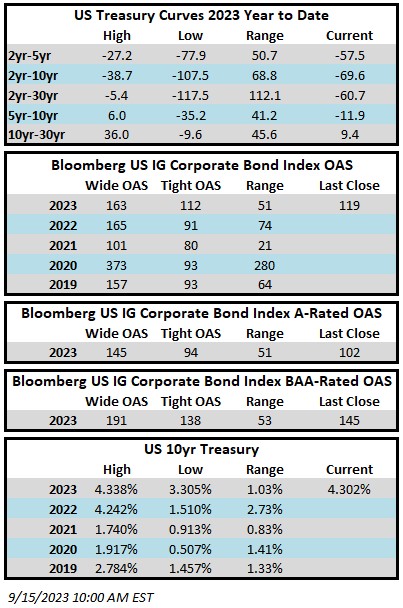

La curva de crédito corporativo es parte integral de nuestra estrategia en CAM. El siguiente gráfico muestra la variación desde principios de año hasta finales del tercer trimestre tanto para la curva del Tesoro como para la curva de rendimiento corporativo. Nuestro enfoque en CAM está en vencimientos intermedios que van de 5 a 10 años.

Tanto las curvas corporativas como las del Tesoro han subido mucho en lo que va de 2023. Es importante señalar que, si bien la curva del Tesoro se ha mantenido invertida, la curva corporativa ha mantenido su pendiente. Por ejemplo, aunque la curva del Tesoro 5/10 se invirtió -4pb al final del trimestre, un inversor podría esperar ganar +21pb en rendimiento adicional (en promedio) al extender desde un bono corporativo a 5 años a un bono corporativo a 10 años. Esto equivale a una curva de crédito corporativo 5/10 de +25pb. Para nuestros inversores actuales, actualmente mantenemos algunos vencimientos más largos de lo habitual, ya que estamos esperando pacientemente a que la curva de crédito corporativo se intensifique. Una curva más pronunciada nos permite extraer más valor para nuestros inversores de las operaciones de extensión. A medida que el ciclo de ajuste de la Reserva Federal llegue a su conclusión lógica, esperamos un aumento tanto en la curva del Tesoro subyacente como en la curva de crédito corporativo. A medida que estas curvas se profundicen, los inversores que han estado con nosotros durante algún tiempo empezarán a vernos reanudar nuestras operaciones de extensión. El siguiente gráfico de la Reserva Federal de St. Louis ofrece un buen ejemplo de cuánto más pronunciada ha sido la curva de crédito corporativo durante la mayor parte de la última década en relación con su situación actual.

La Reserva Federal: ¿ya llegamos a ese punto?

La Reserva Federal aumentó los tipos un +0.25 % en su reunión de julio, pero mantuvo los tipos estables en su reunión de septiembre. La Reserva Federal se reúne dos veces más este año, el primer día de noviembre y nuevamente a mediados de diciembre. El gráfico de puntos del FOMC muestra una expectativa de un aumento más de +25pb este año y recortes de -50pb el próximo año. Al final del trimestre, los inversores asignaban una probabilidad del 39.1 % a una subida adicional de tipos para finales de año, según Fed Funds Futures.

El mensaje de la Reserva Federal ha sido coherente últimamente, recalcando el mantra de “más alto por más tiempo”. No creemos que sea especialmente significativo que la Reserva Federal suba las tasas una vez más, o incluso dos veces. En cambio, creemos que los inversores en bonos deben alegrarse ante la probabilidad de que la Reserva Federal finalmente esté cerca del final de su ciclo de subidas de tipos.

Seguir trabajando duro

Fue un trimestre para olvidar para los rendimientos del crédito IG, pero la propuesta de valor a largo plazo permanece. Incluso a pesar del movimiento masivo de los bonos del Tesoro, la clase de activos se ha mantenido en territorio positivo en el último año. Continuaremos administrando su capital lo mejor que podamos, buscando rendimientos superiores ajustados al riesgo en medio de un panorama cada vez más volátil. Gracias por su continuo interés y confianza.

Esta información solo tiene el propósito de dar a conocer las estrategias de inversión identificadas por Cincinnati Asset Management. Las opiniones y estimaciones ofrecidas están basadas en nuestro criterio y están sujetas a cambios sin previo aviso, al igual que las declaraciones sobre las tendencias del mercado financiero, que dependen de las condiciones actuales del mercado. Este material no tiene como objetivo ser una oferta ni una solicitud para comprar, mantener ni vender instrumentos financieros. Los valores de renta fija pueden ser vulnerables a las tasas de interés vigentes. Cuando las tasas aumentan, el valor suele disminuir. El rendimiento pasado no es garantía de resultados futuros. El rendimiento bruto de la tarifa de asesoramiento no refleja la deducción de las tarifas de asesoramiento de inversión. Nuestras tarifas de asesoramiento se comunican en el Formulario ADV Parte 2A. En general, las cuentas administradas mediante programas de firmas de corretaje incluyen tarifas adicionales. Los rendimientos se calculan mensualmente en dólares estadounidenses e incluyen la reinversión de dividendos e intereses. El índice no está administrado y no considera las tarifas de la cuenta, los gastos y los costos de transacción. Se muestra con fines comparativos y se basa en información generalmente disponible al público tomada de fuentes que se consideran confiables. No se hace ninguna afirmación sobre su precisión o integridad.

La información proporcionada en este informe no debe considerarse una recomendación para comprar o vender ningún valor en particular. No hay garantía de que los valores que se tratan en este documento permanecerán en la cartera de una cuenta en el momento en que reciba este informe o que los valores vendidos no hayan sido vueltos a comprar. Los valores de los que se habla no representan la cartera completa de una cuenta y, en conjunto, pueden representar solo un pequeño porcentaje de las tenencias de cartera de una cuenta. No debe suponerse que las transacciones de valores o tenencias analizadas fueron o demostrarán ser rentables, o que las decisiones de inversión que tomemos en el futuro serán rentables o igualarán el rendimiento de la inversión de los valores discutidos en este documento.

En nuestro sitio web se encuentran disponibles las divulgaciones adicionales sobre los riesgos materiales y los posibles beneficios de invertir en bonos corporativos: https://www.cambonds.com/disclosure-statements/.