Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $4.7 billion and year to date flows stand at -$55.1 billion. New issuance for the week was $1.5 billion and year to date issuance is at $93.5 billion.

(Bloomberg) High Yield Market Highlights

- U.S. junk bonds are set for the biggest weekly loss in six, snapping a two-week gaining streak as yields surge to 9.22% as recession fear spurred a selloff in equities and an extreme inversion in a key portion of the Treasury yield curve. The low-grade market erased most recent gains across ratings. CCCs, the riskiest of junk bonds, posted a loss of 1.04% Thursday, the biggest one-day fall in more than four months. That’s put the notes on track to end a two-week gaining stretch, with a week-to-date drop of 1.08%.

- The October rally fueled and lured investors into junk bond market as US high-yield funds reported a cash intake of $4.7b for the week, the third biggest weekly inflow this year.

- The cash haul came in at the time of acute shortage of new supply, bolstering secondary market prices as investors looked for new paper. The primary market was mostly quiet until this week.

- The rally brought some relief to bankers who have long waited to clear all pending deals to fund leveraged buyout. Apollo’s Tenneco was the first to get out of the gate earlier this week. Nielsen Holdings, a US TV rating business firm, kicked off a bond sale Wednesday to fund its buyout by Elliott Investment Management and Brookfield Asset Management.

- Satellite TV company Dish Network also jumped into the market Wednesday to start marketing 5-year notes to fund the build-out of wireless infrastructure, among other purposes.

- The rally was sapped after the Federal Reserve signaled a higher terminal rate against a backdrop of slowing growth.

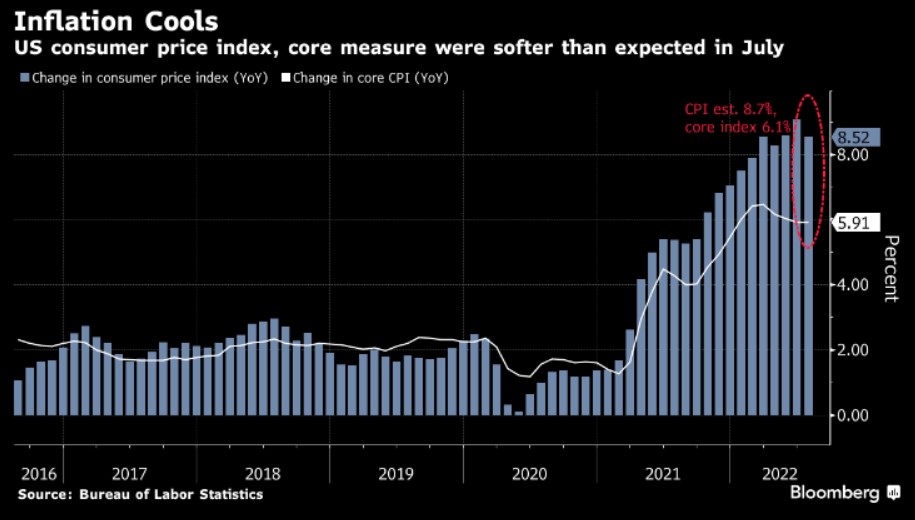

- Despite continued near-term pressures Morgan Stanley expects a “significant deceleration in the inflation path” to take hold by mid-2023, Morgan Stanley’s Srikanth Sankaran wrote last week.

(Bloomberg) Powell Sees Higher Peak for Rates, Path to Slow Tempo of Hikes

- Federal Reserve Chair Jerome Powell opened a new phase in his campaign to regain control of inflation, saying US interest rates will go higher than earlier projected, but the path may soon involve smaller hikes.

- Addressing reporters Wednesday after the Fed raised rates by 75 basis points for the fourth time in a row, Powell said “incoming data since our last meeting suggests that ultimate level of interest rates will be higher than previously expected.”

- Powell said it would be appropriate to slow the pace of increases “as soon as the next meeting or the one after that. No decision has been made,” he said, while stressing that “we still have some ways” before rates were tight enough.

- “It is very premature to be thinking about pausing,” he said.

- The Federal Open Market Committee said that “ongoing increases” will still likely be needed to bring rates to a level that are “sufficiently restrictive to return inflation to 2% over time,” in fresh language added to their statement after a two-day meeting in Washington.

- The Fed’s unanimous decision lifted the target for the benchmark federal funds rate to a range of 3.75% to 4%, its highest level since 2008.

- “Slower for longer,” declared JP Morgan Chase & Co, chief US economist Michael Feroli in a note to clients. “The Fed opened the door to dialing down the size of the next hike but did so without easing up financial conditions.”

- Officials, as expected, said they will continue to reduce their holdings of Treasuries and mortgage-backed securities as planned.

- The higher rates go, the harder the Fed’s job becomes. Having been criticized for missing the stubbornness of the inflation surge, officials know that monetary policy works with a lag and that the tighter it becomes the more it not only slows inflation, but economic growth and hiring too.

- Still, Powell stressed that they would not blink in their efforts to get inflation back down to their 2% target.

- “The historical record cautions strongly against prematurely loosening policy,” he said. “We will stay the course, until the job is done.”

- Fed forecasts in September implied a 50 basis points move in December, according to the median projection. Those projections showed rates reaching 4.4% this year and 4.6% next year, before cuts in 2024. Powell’s remarks made clear that the peak signaled in that projection would be higher if it came at this meeting.

- No fresh estimates were released at this meeting and they won’t be updated again until officials gather Dec. 13-14, when they will have two more months of data on employment and consumer inflation in hand.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.