Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $0.3 billion and year to date flows stand at $48.6 billion. New issuance for the week was $21.3 billion and year to date issuance is at $318.9 billion.

(Bloomberg) High Yield Market Highlights

- S. junk bonds are holding up well amid heavy supply. They’re set to post gains after two weeks of losses, and the riskiest debt in the CCC tier is leading the way.

- CCCs have returned 0.85% so far this week, the fourth week of gains. The broader index has gained 0.15%

- Spreads have also been resilient, tightening 8bps to 488bps more than Treasuries since Friday even after the third busiest week on record for supply, according to Bloomberg

- “Despite the lack of good news, spreads were little changed on the week and volatility remains light compared with equities,” Barclays Plc strategists led by Brad Rogoff wrote in note on Friday. This means that the market is “in a range”, he added

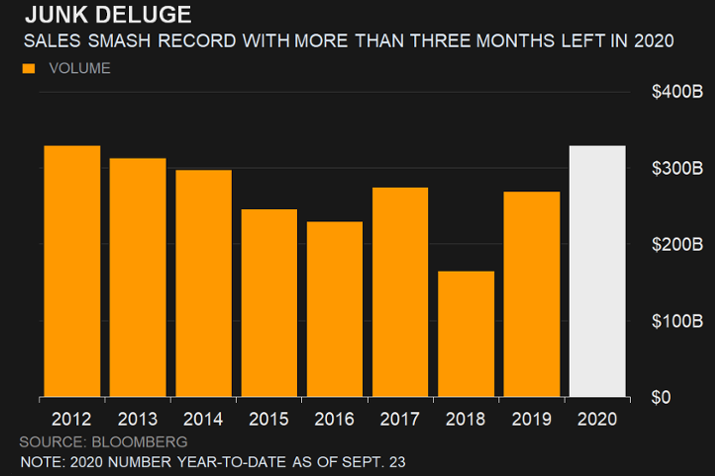

- The annual supply record is in sight with just a bit more needed to topple the previous high of $329.6b set in 2012

- New issues are drawing investor demand of more than three times the size of debt offered in many cases

- Junk bond spreads and yields closed at +488bps and 5.48%, respectively

- CCC spreads bucked the trend, tightening 7bps to +919bps, the lowest level since Feb. 26

(Barron’s) The Federal Reserve Is Buying Fewer Junk Bonds. That Should Be Good News

- The Federal Reserve has taken a step back from the high-yield bond market. That isn’t necessarily bad news, Citigroup says.

- It bought high-yield debt at a pace of $550,000 a day in August, according to Citi’s analysis of the Fed’s latest report. That is significantly slower than its peak pace of $55 million a day in mid-May.

- The composition of the Fed’s purchases has changed in a couple of ways as well.

- First, the central bank bought bonds directly, instead of buying exchange-traded funds that own bonds. While ETFs were the quickest way for the central bank to provide broad support to the corporate debt market, they are only a fraction of the market’s total size. So it shouldn’t be surprising that the Fed has focused its efforts on direct bond purchases instead.

- More important, junk-rated bonds made up a smaller share of the Fed’s purchases. They made up just 1.1% of the bonds purchased during the month ended Aug. 28, down from a 2.5% share in July, Citi found.

- “Critically, the updated report indicates the Fed has significantly reduced both the scale and scope of support for high yield,” the bank’s strategists wrote in a note.

- “The improvements in market structure and economic performance indicate less need for continued broad-based support,” the bank’s strategists wrote. “Should conditions deteriorate over the medium term, the Fed would likely ramp purchases again.”

(Wall Street Journal) Central bank signals rates near zero at least through 2023

- The Federal Reserve pledged to support the economic recovery by setting a higher bar to raise interest rates and by signaling it expected to hold rates near zero for at least three more years.

- In new projections released Wednesday after a two-day policy meeting, all 17 officials who participated said they expect to keep rates near zero at least through next year, and 13 projected rates would stay there through 2023.

- The Fed’s rate-setting committee also released new guidance specifying it would maintain rates near zero until it sees evidence of a tight labor market and inflation reaches 2% “and is on track to moderately exceed 2% for some time.”

- “They set an enormously high bar to raise rates here. That’s the bottom line,” said Roberto Perli, a former Fed economist who is now at research firm Cornerstone Macro.

- The Fed’s meeting was its first since officials made public last month a new policy framework that abandoned officials’ longtime strategy of pre-emptively lifting interest rates to head off higher inflation rates.

- The latest materials from the Fed revealed just how much the central bank expects to change the way it will react to improvements in the economy.

- New economic projections, for example, showed most officials expected interest rates to stay near zero over the next three years, even if inflation reaches 2% and the unemployment falls to around 4%.

- “These changes clarify our strong commitment over a longer time horizon,” said Fed Chairman Jerome Powell at a news conference. “I’m not looking for a big reaction right now. But I think over time, guidance that we expect to retain the current stance until the economy has moved very far toward our goals is a strong and powerful thing.”