(Bloomberg) High Yield Market Highlights

- US junk bonds are headed for their fifth weekly gain on easing trade tensions and signs of a still-resilient economy. The rally was also fueled by bets that the Federal Reserve will cut interest rates at least twice this year after data showed tariffs have had limited impact on inflation so far.

- Falling spreads and attractive all-in yields attracted a flood of new debt to the primary market. Eleven borrowers sold more than $11b in just four sessions to make it the busiest week since January. Total supply this month is at $19b.

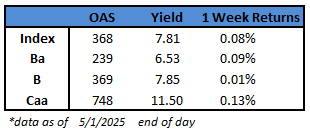

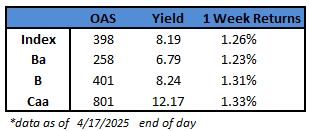

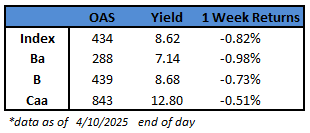

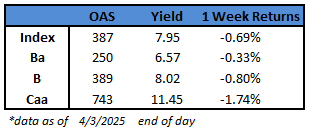

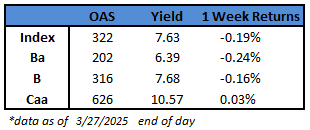

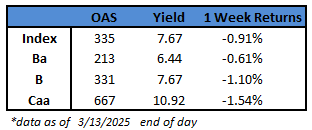

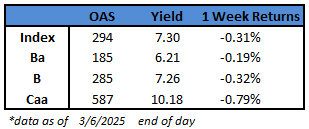

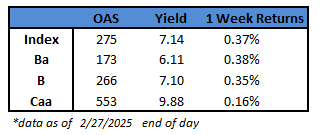

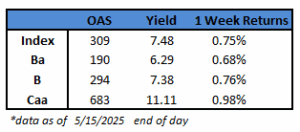

- The Index yield is set to drop for the fifth straight week, the longest streak since September. It declined 26 basis points in four sessions this week to 7.48%. The Index risk premium fell for the sixth consecutive week, the longest streak in 17 months. It closed at 309 after falling 34 basis points so far this week.

- The broad gains extended across ratings. CCC yields are on track to drop for the fifth straight week after closing at 11.11% on Thursday. Yields fell 19 basis points in four sessions this week. CCCs are also set to post fifth weekly gains.

- BB yields are also poised to fall for the fifth successive week after closing at 6.29% on Thursday, down 18 basis points in four sessions. Spreads tightened for the sixth consecutive week to close at 190 basis points, the longest declining streak in more than four years

- Meanwhile, investors flocked to new issues with big orders following light supply after a frozen market in April and three straight weeks of cash inflows into US high yield funds. US high yield funds reported a cash intake of $2.6b for week ended Wednesday, according to LSEG Lipper

- More borrowers are expected to take advantage of the broad market rally next week

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.