(Bloomberg) High Yield Market Highlights

- US junk bond yields reached a new nine-month high on climbing oil prices, and Fed Chair Jerome Powell cautioning that the inflationary fallout from rising energy costs remains uncertain.

- The high-yield primary market has remained quiet.

- Rattled investors pulled more than $3b from US high yield funds last week. The weekly withdrawals were the highest since the tariff-turmoil last April, reflecting the continuing war in Iran and concerns about its potential impact on inflation and growth.

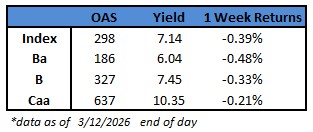

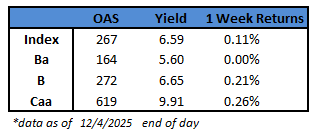

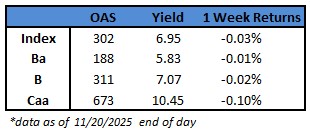

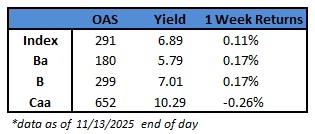

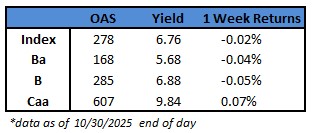

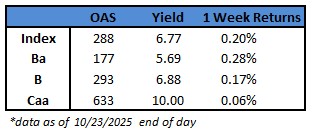

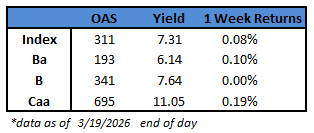

- CCC yields, the riskiest part of the market, breached the 11% level to close at a nine-month high of 11.05%. BB yields also rose to a new nine-month high at 6.14%, on track for a fourth weekly rise, the longest such streak since April 2025.

(Bloomberg) Fed Holds Rates Steady, Powell Vows to Stay Amid DOJ Probe

- Federal Reserve officials left interest rates unchanged as they acknowledged increased uncertainty due to war in the Middle East.

- Chair Jerome Powell emphasized that to resume lowering rates, officials would have to see progress in reducing inflation, especially goods inflation that has been boosted by tariffs.

- “If we don’t see that progress, then we won’t see the rate cut,” Powell said in remarks to reporters after the Fed released its decision.

- That progress may be difficult to achieve. In economic forecasts released with their decision, officials raised their outlook for inflation in 2026 to 2.7% from 2.4%. Notably, they saw the core measure — which excludes volatile food and energy categories — also rising to 2.7%.

- Powell surprised Fed watchers by making some definitive statements about his near-term future at the central bank. He told reporters he had “no intention” of resigning as a member of the Fed’s Board of Governors until an investigation by the Department of Justice into a building renovation project is “well and truly over.”

- He said that if his successor is not confirmed before his term as chair ends in May, he would serve as chair pro tempore. The Fed has conferred that temporary designation in the past on a board member to lead the institution when the chair role was vacant. Powell’s term as a governor extends until January 2028.

- He said he hadn’t decided whether he would depart if the investigation were closed.

- The Federal Open Market Committee voted 11-1 to hold the benchmark federal funds rate in a range of 3.5% to 3.75%. Governor Stephen Miran dissented, calling for a quarter-point reduction.

- In their post-meeting statement, policymakers underscored the uncertainty they’re facing in the economy due to the conflict in the Middle East, as did Powell in his press conference.

- “It is too soon to know the scope and duration of the potential effects on the economy,” Powell said. “The thing I really want to emphasize is that nobody knows.”

- Asked about the impact of surging oil prices on inflation, Powell acknowledged that central bankers typically don’t raise rates when energy prices jump because the impact on inflation is temporary. But that approach, he said, has always depended on the public continuing to expect inflation will settle around the Fed’s 2% goal over the long term. He also noted that inflation in the US has been above the Fed’s 2% target for five years.

- Powell said the committee had again discussed the possibility that the Fed’s next rate move could be a hike, but added, “the vast majority of participants don’t see that as their base case.”

- Wednesday’s decision marks the second straight time officials held rates in place, though the economic backdrop has changed significantly since their last meeting. In January, policymakers signaled growing confidence the unemployment rate was stabilizing. Soon after, several officials sounded intent on holding rates for an extended period to help nudge inflation lower.

- Then came a weak February employment report that cast fresh doubt on the steadiness of the labor market. US-Israeli strikes against Iran that began Feb. 28 have also caused global oil prices to surge, threatening to boost inflation and undermine growth and employment.

- Officials dropped language from their January statement describing the labor market as showing signs of stabilization. In its place, they said the unemployment rate was “little changed in recent months.”

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.