CAM High Yield Weekly Insights

(Bloomberg) High Yield Market Highlights

- US junk bond yields held steady and spreads barely moved as investors remained wary of tech-stocks volatility and stretched valuations. Concerns deepened after data showed US consumer spending accelerated while inflation rose at its fastest pace in more than three years, reinforcing expectations that the Federal Reserve is set to raise interest rates as early as September.

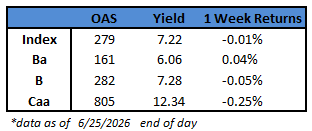

- Elevated valuations and persistent inflation concerns pushed yields and spreads on the riskiest tier of the junk bond market – CCCs – to fresh 14-month highs, driving losses in three of the last four sessions. Yields closed at 12.34% and spreads at 805 basis points.

- The primary market, however, looked past those concerns, as a supply wave persisted with a steady stream of issuance. Three more borrowers sold $1.75b on Thursday, driving the weekly issuance volume to more than $7b, the busiest since mid-May

- Borrowers rushed to take advantage of the still-open capital markets and strong demand before conditions change

- The multiple issues sold on Thursday drove June’s volume to more than $33b, the second-biggest month for supply this year

(Bloomberg) US Hot Inflation and Spending Data to Keep Fed Cautious

- Hot headline and core inflation, together with a pickup in personal spending, affirm the Fed’s hawkish tilt at the June FOMC meeting. Spending growth was broad-based, and real consumption accelerated even amid high inflation.

- A rise in hiring and wage growth has helped to undergird spending in recent months, and elevated tax refunds and favorable wealth effects also have played a role. Declining global energy prices will suppress headline inflation going forward.

- The PCE deflator increased 0.45% in May (vs. 0.41% prior), boosting the year-on-year inflation pace to 4.1% from 3.8%. The monthly pace of core inflation jumped to 0.32% (from 0.25%). The year-on-year pace rose to 3.4% from 3.3%.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.