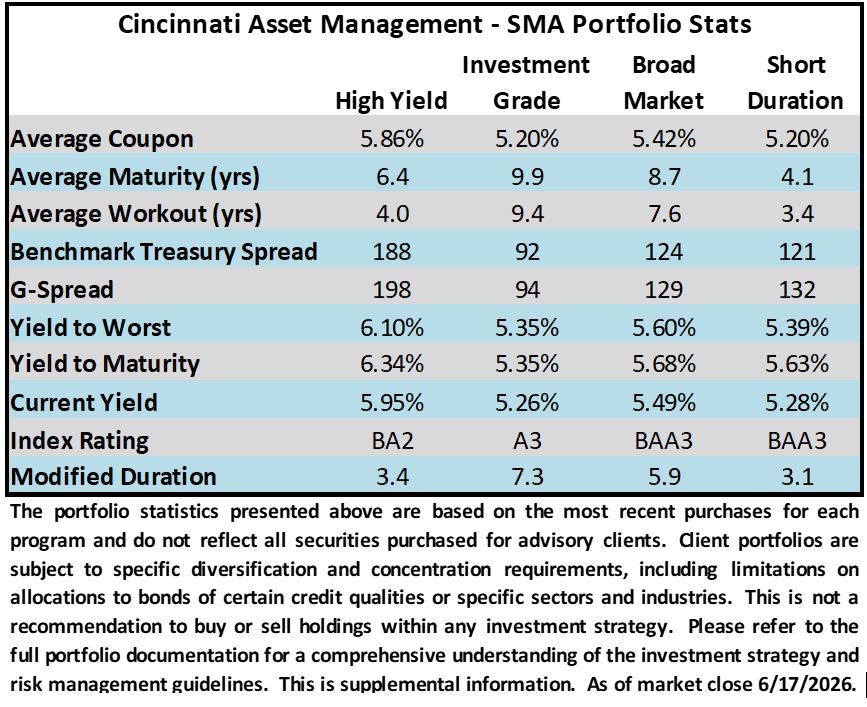

CAM Investment Grade Weekly Insights

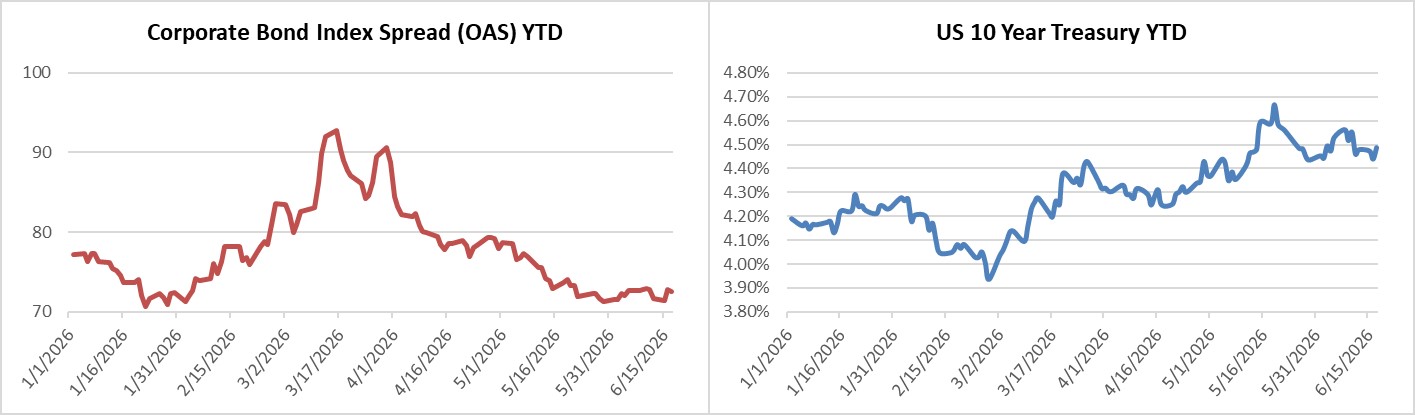

Credit spreads moved slightly wider during the holiday shortened week. The OAS on the Corporate Index closed at 73 on Wednesday June 17th after closing the week prior at 72. Spreads are slightly tighter as we go to print on Thursday afternoon. The 10yr Treasury ended last week at 4.48% and it closed at 4.49% on Wednesday evening. Rates are about 5bps lower across the Treasury curve on Thursday. Through Wednesday, the Corporate Bond Index year-to-date total return was +0.55% and the yield to maturity for the index was 5.24%.

Points of Interest

The main event of the week was Kevin Warsh’s first meeting and press conference as FOMC chair. It was an interesting juxtaposition; Warsh was adamant during the nomination process that the Fed’s policy rate was too high, but his first action as chair was delivering the views of an FOMC that is increasingly thinking about increasing the Federal Funds Rate by the end of the year. The Fed’s dot plot showed nine officials were in favor of at least one hike (six of those were looking for multiple increases) while 8 were expecting no change and just one was looking for a cut. Chairman Warsh did not participate in the dot plot because he does not believe it is “helpful in the conduct of policy.” The voting members of the FOMC were unanimous (12-0) in their decision to leave interest rates unchanged.

With the advent of a new Chairman, a quick history lesson seems prudent. The Fed did not always do regular post-meeting press conferences and it was only formally introduced in April of 2011, and it was only on a quarterly basis. Chairman Bernanke introduced it as a way to increase central bank transparency in the wake of the financial crisis. In 2019, Chairman Powell expanded the press conference practice to occur at the conclusion of every regular scheduled FOMC meeting. Regarding the Summary of Economic Projections, also known as the “dot plot”, this release was formally introduced on January 25, 2012 and has always been done on a quarterly basis since then. The Fed has changed the way it communicates over the years and we expect that Kevin Warsh will add his own mark in the months ahead.

Primary Market

$44 billion in new debt was priced this week through Wednesday, blowing past dealer estimates of $25bln. There are two deals pending on Thursday that will add $5.05bln to that number, bringing the weekly total to almost

$50bln. The biggest deal of the week hit the tape first thing on Monday morning as Nvidia printed $25bln across seven different maturities. Next week, syndicate desks are looking for $50bln of issuance. The word on the street is that SpaceX could make its inaugural foray into the investment grade credit markets as soon as next week with a new deal that could total at least $20bln. The pace of issuance this year remains torrid and is well ahead of 2025, up more than 30% y/y.

Flows

According to LSEG Lipper, for the week ended June 17th, short and intermediate investment-grade bond funds reported a net inflow of +$5.2bln. 2026 year-to-date net flows into investment grade were +$67.1bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.