CAM High Yield Weekly Insights

(Bloomberg) High Yield Market Highlights

- US junk bonds may end a three-week rally as they head to close the week with modest negative returns. Markets were jolted earlier this week when faster-than-expected inflation caused the biggest one-day loss in four months.

- The consumer price index rose by more than forecast in January on a monthly and annual basis, suggesting that the road back to the 2% inflation target will be bumpy.

- However, the markets quickly pared those losses. The rebound got a boost after data showed US factory production declined for the first time in three months and retail sales dropped in January, indicating that inflation will moderate steadily toward the target.

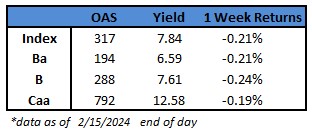

- Yields climbed to a five-week high of 7.91% on Tuesday after the surprise rise in inflation, but dropped to 7.84% after data showed retail sales fell the most in year and factory production declined. However, yields are still up nine basis points week-to-date at 7.84%.

- The modest losses extend across ratings in the US junk bond market. CCC yields rose eight basis points for the week to 12.58% after jumping to 12.68% on Tuesday.

- BB yields closed at 6.59% after rising to 6.63%, up eight basis points for the week. BBs are headed toward a second straight week of losses.

- As the market was rattled by inflation data, US borrowers stayed on the sidelines as they assessed the risk appetite.

- The primary market was relatively quiet after Monday. More than $6b priced on Monday to make it the busiest day since April 2023.

- The month-to-date supply stood at almost $19b and year-to-date at $50b.

- Even amid volatility, spreads were closer to 300 basis points and yields were still below 8%.

- Barclays expects spreads to compress further to a range of 290-315 basis points in the next six months.

- Marginal demand for yield is strong, and spreads seems to be an afterthought, Brad Rogoff and Dominique Toublan of Barclays wrote this morning.

- We see limited headwinds from the macro side and credit fundamentals, they wrote.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.