CAM Investment Grade Weekly Insights

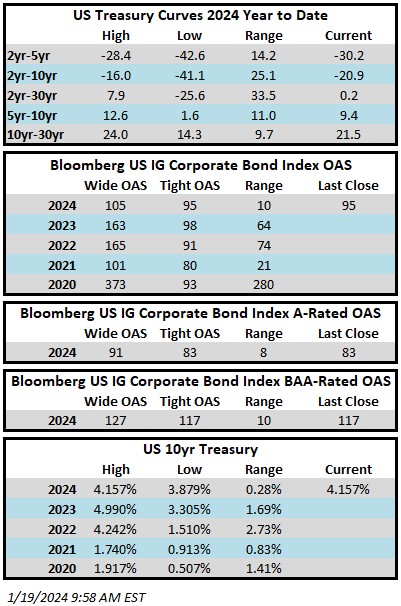

Credit spreads are looking to finish the week on a strong note, trading at the tightest levels of the year as we go to print. The Bloomberg US Corporate Bond Index closed at 95 on Thursday January 18 after having closed the week prior at 97. The 10yr is trading a 4.16% this Friday morning, up sharply on the week after having closed the week prior at 3.94%. The benchmark rate is now trading at its highest yield of the New Year. Through Thursday, the Corporate Index YTD total return was -1.35%.

Economics

It was a busy week for economic data with several market moving prints. December retail sales data on Wednesday came in with a larger increase than expected, fueling higher Treasury yields. On Friday, consumer sentiment rose to its highest level since January 2021, far in excess of the estimate. The data also showed that consumers expect prices will increase at an annual rate of 2.9% over the next year, down from 3.1% a month earlier. So far in 2024, the data has served to cool market expectations of near term Fed rate cuts. The market went from anticipating as many as 6 cuts in 2024 but now the expectation has shifted to 3 or 4 cuts based on interest rates futures. The next 10 days will be busy from a data perspective, culminating in a FOMC meeting on January 31.

Issuance

It was a huge week of issuance especially considering that the market was closed on Monday in observance of Martin Luther King Day. With no new deals on Friday, issuers managed to print >$49bln of new debt in three days bring supply for the month of January to nearly $150bln. Investor demand has been strong and new issue concessions have shrunk in concert as investors have gobbled up new paper leaving most new issues to immediately trade better in the secondary market. Another strong week could easily see this January surpass the all-time January record of $175bln that was set in 2017.

Flows

According to Refinitiv Lipper, for the week ended January 17, investment-grade bond funds reported a net inflow of +$227.3mm. This was the fifth consecutive weekly inflow for IG funds.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.