CAM High Yield Weekly Insights

(Bloomberg) High Yield Market Highlights

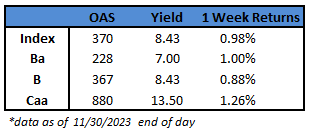

- The broad November rally in risk assets propelled CCCs, the riskiest tier of the junk bond market, alongside equities, to post the biggest monthly returns since January of this year. CCC yields plunged 125 basis points in November, also the most in 10 months, to 13.50%, driving gains of 4.53%.

- The broad surge across risk assets was fueled by a market consensus that the Federal Reserve was finished with the most aggressive tightening cycle in decades and that it will begin to ease monetary policy by the middle of 2024. Junk bond spreads dropped to a 10-week low of 370 basis points, after falling 67 basis points in November, the biggest monthly decline in five months.

- The rally came as the 5- and 10-year Treasury yields dropped by about 60 basis points each during the month of November to close at 4.27% and 4.33%, respectively. Treasury yields plunged from near 5% on Oct. 19

- US junk bonds racked up gains of 4.53%, the largest in a month since July 2022, fueled by BBs. Yields fell 106 basis points to 8.43%, also the biggest monthly decline in 16 months

- BBs had the best performance in 16 months, with returns of 4.6% reversing the three-month losing streak as rates tumbled

- Yields crashed by 99 basis points to close near a four-month low of 7%, the biggest monthly decline in over a year

- Resilient growth, cooling inflation and a softening labor market gave a strong impetus to the November rally, luring investors and US borrowers from the sidelines

- November is the fourth busiest month for issuance as volume surged to $19.4 billion, more than double October’s total of $9.45 billion

- US junk bond funds were inundated with new cash as investors poured more than $11b in November

- Year-to-date supply stood at $163 billion, up by about 60% from 2022’s $102 billion

- Forecasts for junk bond supply in 2024 range from $200 billion to $230 billion, with the exception of BofA, which estimates gross supply to be around $165 billion, a 5% drop from its projection of $175 billion for 2023

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.