CAM Investment Grade Weekly Insights

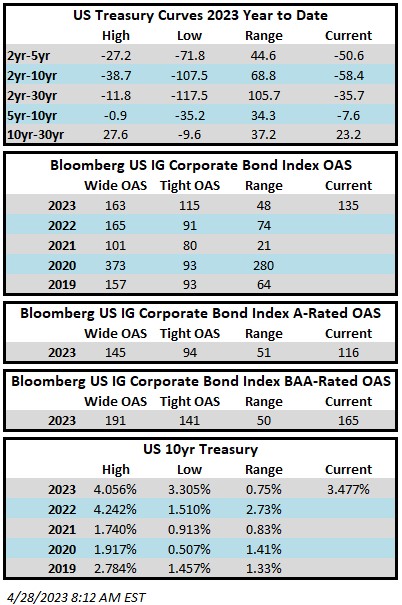

Investment grade credit spreads were mostly unchanged for the second consecutive week with the spread on the index just slightly wider from where it started the week. The Bloomberg US Corporate Bond Index closed at 135 on Thursday April 27 after having closed the week prior at 133. The 10yr Treasury yield trended lower throughout the week with the benchmark rate trading at 3.48% as we go to print relative to 3.57% at the close last Friday. Through Thursday the Corporate Index had a YTD total return of +3.7% while the S&P500 Index return was +8.3% and the Nasdaq Composite Index return was +16.3%.

It was a quiet week in that the Federal Reserve was in media blackout so there weren’t many speeches to parse but there was still plenty of economic data. On Friday we got a PCE inflation print that showed that inflation remained a problem last month which will likely reinforce the case for a Fed rate hike next Wednesday. Also on Friday morning, the spending numbers showed that consumers are starting to lose steam with the February spending number seeing a downward revision and the March number coming in flat. There will be plenty of action next week starting with a FOMC rate decision on Wednesday. The debt ceiling looms large and more frequent headlines will start to become a regular occurrence as we drift closer to the X date.

The primary market was reasonably active given that earnings season is in full swing. $16.85bln in new debt priced this week which just eclipsed the high end of the $10-$15bln estimate. There are no new deals in the queue this last day of April so new issuance will finish with a monthly total of just $66bln vs a $100bln estimate. The big questions for May: will supply come to fruition and what will the impact be on credit spreads? May is typically a seasonally busy month having averaged $135bln in new supply over the past 5 years.

According to Refinitiv Lipper, for the week ended 4/26/2023, investment-grade bond funds saw -$1.3bln of cash outflows. This was the first reported outflow for investment grade since March.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.