CAM Investment Grade Weekly Insights

CAM Investment Grade Weekly

08/31/2018

As summer winds down, it was another quiet week in the credit markets, and spreads are set to finish the week a touch wider on global trade concerns.

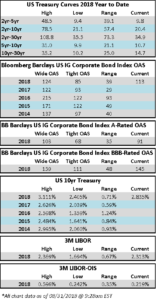

According to Wells Fargo, IG fund flows for the week of August 23-August 29 were +$965 million. IG flows are now +$91.421 billion YTD.

Per Bloomberg, there was just $2.5 billion of new issuance printed during the week. Bloomberg’s tally of YTD total issuance stands north of $774bn.

(Bloomberg) When Diversification Doesn’t Spread Your Risks

- If you want to diversify your risks, invest with a bunch of different managers, right?

- Well, not always. When investment managers create diversity within their funds, chances are they will look similar to other managers also aiming for diversity. And that means they could all succumb to the same ills. This is a widespread issue, but it is highly relevant right now in risky credit markets.

- A simple illustration is index-tracking equity funds. There is almost zero benefit to investing in several managers that all track the S&P 500: You are just buying the same stocks via different channels.

- A more complex example is how banking developed over the years before the 2008 crisis. Banks grew large and they diversified across borders and business lines, which was partly to avoid their past mistakes of taking too much risk in one place, such as Texan real estate. But big global banks ended up with many of the same exposures, and so all hit the same problems at the same time.

- This diversification philosophy also drove securitization, the business of turning a big book of mortgages, for example, into a set of investible bonds. But you know the story: Each deal was diversified and risks were spread around, but too many mortgages were too similar and everybody lost.

- This idea is alive and well in today’s market for risky leveraged loans, where securitization creates so-called collateralized loan obligations, which buy 60% of loans.

- Despite the recent boom in the issuance of both loans and CLOs, markets remain concentrated. So CLO portfolios are often similar and the biggest loans are very commonly held, according to data from Fitch Ratings. In the U.S., debt from computer maker Dell International is owned by 86% of CLOs, for example. On average, U.S. CLO managers have roughly one-third of all borrowers in common, while in Europe about half of borrowers are common.

- There is a simple lesson here for CLO investors: Never assume that investing with multiple managers diversifies your risk, as there is a fair chance you are buying many of the same underlying loans.

- But there is a potential pitfall here that everyone should note. Today’s loan market has a much greater concentration of deals with low ratings, single-B and below, which are more prone to downgrades and defaults. More low-quality loans everywhere likely means more widespread losses when a downturn comes—no matter what kind of diversification you think you have.

(Bloomberg) Moody’s upgrades Abbott Laboratories’ senior unsecured rating to Baa1, outlook remains positive

- Moody’s Investors Service (“Moody’s”) today upgraded Abbott Laboratories’ (“Abbott”) senior unsecured rating to Baa1 from Baa2. The company’s commercial paper rating was affirmed at Prime-2. The rating outlook remains positive.

- “The upgrade reflects the company’s continued progress deleveraging since the 2017 acquisitions of St Jude Medical and Alere,” stated Scott Tuhy, a Senior Vice President at Moody’s. Moody’s expects that Abbott’s debt/EBITDA will approach 3 times by the end of 2018. Debt/EBITDA was approximately 3.4 times as of June 30, 2018. “The upgrade also reflects the progress the company has made integrating its acquisitions. In particular, Abbott’s Cardiovascular and Neuromodulation businesses — the significant majority of which is legacy St Jude operations — has shown accelerating revenue growth and expanding operating margins since the merger,” added Tuhy.

- The positive outlook reflects Moody’s expectations for further deleveraging into 2019 as the company reduces debt and improves earnings. Upward pressure is tempered by the company’s recent track record of increasing debt to fund acquisitions.