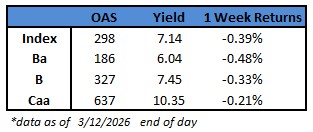

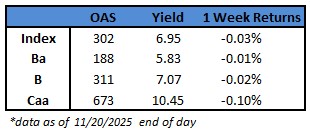

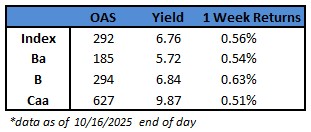

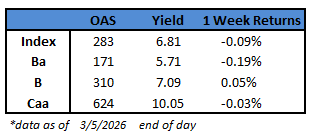

(Bloomberg) High Yield Market Highlights

- US junk bonds will take their cue from key employment and retail sales data Friday amid broader market angst tied to Iran war

- Meanwhile, issuance of new junk notes has slowed to a trickle

- Thursday saw one deal enter the market, a $250 million tap from NGL Energy, but that offering was subsequently dropped as a concurrent leveraged-loan offering was upsized by that amount

- High-yield bonds have posted losses on five of the last six sessions, and the market is at risk of its first back-to-back weekly declines in four months, according to data compiled by Bloomberg

(Bloomberg) US Unexpectedly Sheds 92,000 Jobs, Unemployment Rate Rises

- US employers unexpectedly cut jobs in February and the unemployment rate rose, pointing to lingering fragility in a labor market that was thought to be stabilizing.

- Nonfarm payrolls decreased 92,000 last month after a strong start to the year, according to Bureau of Labor Statistics data out Friday. The unemployment rate climbed to 4.4%. The decline in payrolls — which was one of the largest since the pandemic — partly reflected a decrease in health care employment due to strike activity.

- The report calls into question whether the labor market is actually steadying after the worst year for hiring outside of a recession in decades. While job growth jumped in January and unemployment insurance claims have settled at a low level, companies may be starting to follow through on a series of previously announced layoffs.

- And a recent trend in productivity gains illustrates how spending on artificial intelligence has allowed some firms to get by with leaner staffing.

- “The idea the labor market has turned a corner implodes with this report,” Samuel Tombs, chief US economist at Pantheon Macroeconomics, said in a note.

- The figures could refocus the Federal Reserve’s attention on the jobs market as it assesses how long to hold interest rates steady. Policymakers have been more attuned to inflation lately — even before the US-Israeli war on Iran sparked concerns among investors about price pressures.

- In an interview on CNBC following the report, San Francisco Fed President Mary Daly said, “The hopes that the labor market was steadying, maybe that was too much, and we really have to keep our eye on the labor market.”

(Bloomberg) US Retail Sales Fell in January on Fewer Vehicle Purchases

- US retail sales declined in January, restrained by weakness at auto dealers as winter weather-related disruptions tempered some activity.

- The value of retail purchases, not adjusted for inflation, decreased 0.2% after no change in December, Commerce Department data showed Friday. Excluding car dealers, sales were little changed.

- Seven out of 13 categories posted decreases. Motor vehicle sales dropped 0.9%, while receipts at apparel merchants, gas stations and health and personal care stores also declined.

- The report showed a 0.3% increase in so-called control-group sales — which feed into the government’s calculation of goods spending for gross domestic product. The measure excludes food services, auto dealers, building materials stores and gasoline stations.

- More modest overall retail spending at the turn of the year has been accompanied by worries about the job market and cost of living. While wealthier households have the wherewithal to purchase non-essential goods, middle- and lower-income consumers may be growing more cautious.

- Walmart Inc., a bellwether for the economy, last month forecast less earnings growth this year than expected.

- A lengthy winter storm that included significant snowfall and ice across the central and eastern US likely impeded shoppers during the weather event. The Arctic blast triggered the most flight cancellations since the pandemic and left more than 1 million homes and businesses without power.

- Receipts at restaurants and bars, the only service-sector category in the retail report, declined 0.2% in January. Restaurants including Sweetgreen Inc. and Chipotle Mexican Grill Inc. said that sub-freezing temperatures and winter storms hindered sales.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.