CAM Investment Grade Weekly Insights

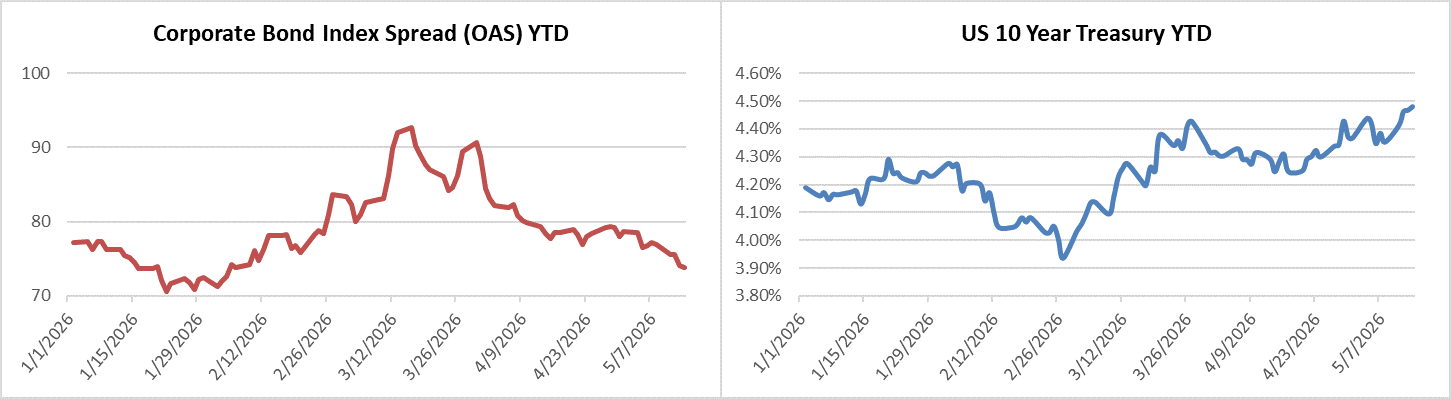

Credit spreads moved tighter this week but they are a touch softer as we go to print on Friday morning. The OAS on the Corporate Index closed at 74 on Thursday May 14th after closing the week prior at 77. The 10yr Treasury ended last week at 4.35% and it closed at 4.48% on Thursday evening. The benchmark rate moved higher again on Friday morning as investors expressed disappointment that President Trump’s visit to China did not yield a near term resolution for the closure of the Strait of Hormuz. Through Thursday, the Corporate Bond Index year-to-date total return was +0.03% and the yield to maturity for the index was 5.18%.

Points of Interest

It was a tough week for inflationary pressures. CPI came in hot, with most measures posting readings that were higher than expectations. The PPI release also came in meaningfully higher than consensus estimates. PPI is a measure of inflation at the business or wholesale level, before those prices reach consumers, so it has the potential to act as a leading indicator for CPI and could mean that there are even higher CPI readings coming in the future. Additionally, investors did not receive the news they were looking for as President Trump went China to meet with President Xi Jinping. Market participants were anticipating that China would apply more pressure on its Iranian allies to fully reopen the Strait of Hormuz. Putting it all together, the aforementioned issues, along with a tenuous Iranian ceasefire, have led to an increase in Treasury yields across the entire curve.

In other news, Kevin Warsh was confirmed by the Senate as the new Federal Reserve Chair in a 55-45 vote, the narrowest margin since 1977. Jerome Powell’s term as Chair ends today and Warsh’s first meeting at the helm will occur on June 17th (The FOMC does not meet in the month of May).

Primary Market

It was a solid week for primary market issuance during the seasonally busy month of May. Investment grade rated companies priced more than $52bln in new debt, almost precisely in line with expectations. Dealers are looking for $40bln next week. Year-to-date new issue supply stood at $903bln through the end of the week.

Perhaps the most interesting piece of news in the primary market this week was not related to the U.S. domestic bond market. Alphabet priced the biggest Japanese Yen bond deal on record from a foreign issuer. The size of the deal was roughly $3.64bln USD. This is interesting for two reasons. First, Hyperscalers are increasingly turning to foreign bond markets to raise capital for their AI-related spending in order to diversify their funding sources. Alphabet has also raised capital in Canadian dollars, British pounds and Swiss francs. Amazon, Meta, Microsoft and Oracle have also tapped foreign bond markets in recent weeks. The fact that these companies are raising capital outside of the US market is supportive of their $USD credit spreads and helps to avoid a negative technical of too much AI supply in our market. The second interesting point is the fact that Alphabet’s deal was the largest ever Yen deal when it was only a mere $3.64bln USD. This is a decent slug of bonds, no doubt, but would hardly draw any attention at all in the US market. This points to the depth and breadth of the US market, which is the largest, deepest and most liquid bond market in the world. Japan is no slouch as the third largest bond market (China is #2), it is just that the US is that much larger and more efficient which is why issuers prefer it for the bulk of their capital raising needs.

Flows

According to LSEG Lipper, for the week ended May 13th, short and intermediate investment-grade bond funds reported a net inflow of +$4bln. 2026 year-to-date flows into investment grade were +$52.3bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.