CAM Investment Grade Weekly Insights

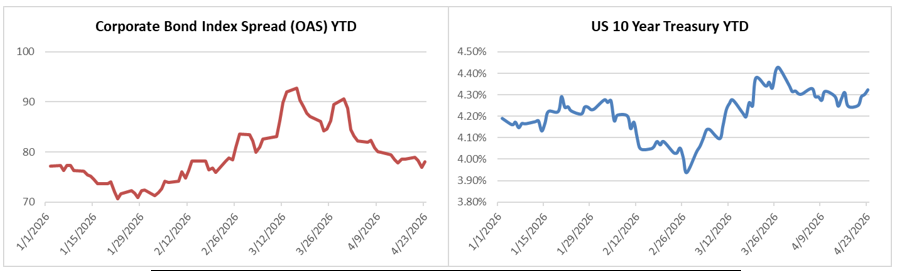

Credit spreads were modestly tighter on the week through Thursday. The OAS on the Corporate Index closed at 78 on Thursday April 23rd after closing the week prior at 79. The 10yr Treasury ended last week at 4.25% and it closed at 4.32% on Thursday evening. Through Thursday, the Corporate Bond Index year-to-date total return was +0.42% and the yield to maturity for the index was 5.06%.

Points of Interest

The highlight of the week occurred on Tuesday with Federal Reserve Chair nominee Kevin Warsh’s confirmation hearing before the Senate Banking Committee. Warsh repeatedly stated that he would embrace the role in an independent manner and he reaffirmed his preference for a smaller Fed balance sheet. The Fed’s use of forward guidance was a topic of discussion; Warsh has been critical of the Fed’s signaling and its focus on PCE as its preferred inflation gauge. He argues that Fed forecasts can lead to policy errors instead of allowing decisions to be made based on real-time debate in response to changing economic conditions. On Friday, the DOJ announced that it was dropping the criminal probe of current Fed Chair Powell which may clear the way for Warsh’s confirmation. Next week is Jerome Powell’s last scheduled meeting as Federal Reserve Chair though he has said he will remain on as chair pro tempore if his successor is not confirmed. Fed Funds Futures are pricing almost no chance of a rate cut/hike at next week’s meeting.

It was another light week for economic data but things ramp up next week. Thursday in particular is a busy one with personal income/spending, PCE and GDP releases. Next week is also the height of earnings season in the credit markets with 259 investment grade rated companies reporting. All eyes will be on the hyperscalers as Alphabet, Amazon, Meta and Microsoft will all release earnings on Wednesday afternoon.

Primary Market

Investment grade companies priced $19.3bln of new debt this week, in line with the low end of dealer estimates. Syndicate desks are looking for a similar figure next week. Volume should start to pick up in the first full week of May as many companies will have reported earnings by that time. Year-to-date new issue supply stood at $751bln through the end of the week.

Flows

According to LSEG Lipper, for the week ended April 22nd, short and intermediate investment-grade bond funds reported a net inflow of +$1.53bln. 2026 year-to-date flows into investment grade were +$39.7bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.