CAM Investment Grade Weekly Insights

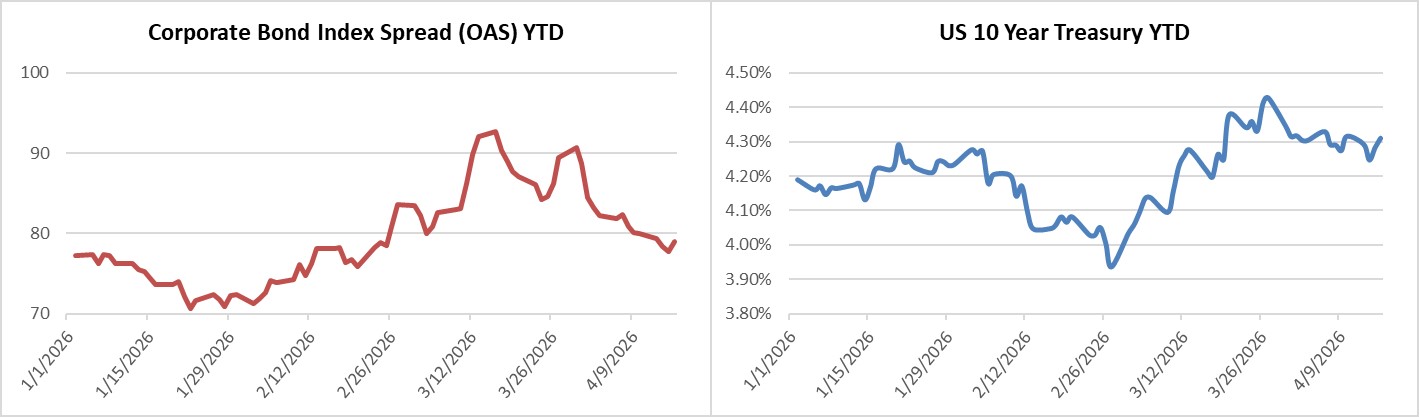

Credit spreads were slightly tighter on the week through Thursday and Friday morning is seeing some positive price action as well. The OAS on the Corporate Index closed at 79 on Thursday April 16th after closing the week prior at 80. For context, the Index OAS is now several basis points better than where it was just prior to the beginning of the Iran conflict. The 10yr Treasury ended last week at 4.32% and it closed at 4.31% on Thursday evening. Through Thursday, the Corporate Bond Index year-to-date total return was +0.34% and the yield to maturity for the index was 5.04%.

Points of Interest

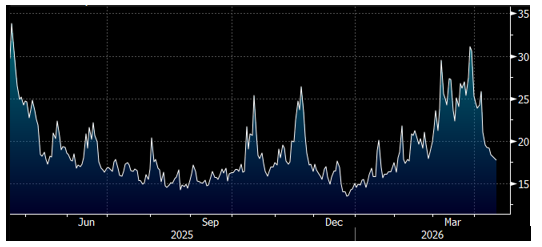

The big theme of the week was the return of relative calm across risk assets. The CBOE Volatility Index (VIX) has come off sharply from recent highs. VIX readings above 30 indicate high volatility while readings under 20 show periods of stability.

With no formal deal in place with Iran we remain somewhat skeptical about the speed with which equity markets have rebounded. They should certainly be better relative to the lows but the situation remains tenuous at best and higher oil prices will weigh heavily on the consumer and certain sectors of the economy.

It was a light week for economic data with nothing earth shattering from a market movement perspective. Existing home sales remained unsurprisingly sluggish amid an environment of higher mortgage rates for the past month. Producer price inflation surprised slightly to the downside but the release had little market impact. Next week brings a bit more excitement with additional housing data, retail sales, PMI and consumer sentiment data. Looking further ahead, the next FOMC decision occurs on April 29th. As of Friday morning, Fed Funds Futures were pricing a >99% chance of no change in the policy rate at the upcoming meeting.

Primary Market

Subdued interest rate volatility brought issuers off the sidelines this week. According to data compiled by Bloomberg, 21 companies priced over $57bln of new debt. The largest banks in the US all posted earnings this week which allowed them to exit blackout periods with a green light to raise capital –banks alone accounted for $36.5bln of this week’s volume.[i] Next week is expected to have a slower cadence, with syndicate desks estimating $20-$25bln of new supply as corporate issuers continue to work through a busy period for earnings. Year-to-date new issue supply stood at $731bln through the end of the week.

Flows

According to LSEG Lipper, for the week ended April 15th, short and intermediate investment-grade bond funds reported a net inflow of +$0.849bln. This comes after two consecutive weeks of outflows, which were the first incidents of negative flows since November 2025. 2026 year-to-date flows into investment grade were +$38.2bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

i Bloomberg, April 17 2026, “US IG OPEN: Bond Sales ON Pause After Big US Banks Boost Volume”