CAM Investment Grade Weekly Insights

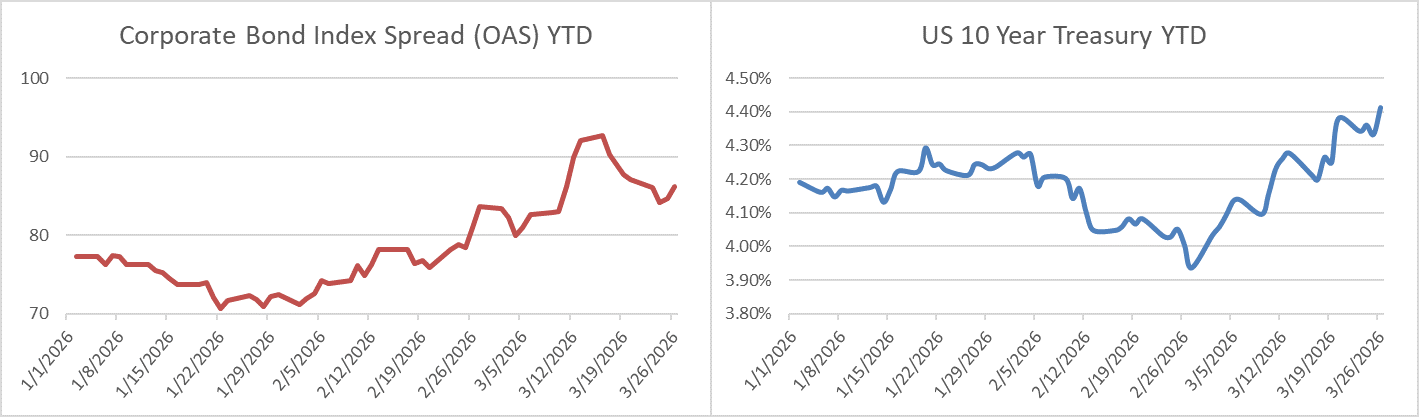

Credit spreads were tighter on the week through Thursday but Friday’s price action is indicating that the market will finish the period unchanged. The OAS on the Corporate Index closed at 86 on Thursday March 26th after closing the week prior at 87. The 10yr Treasury ended last week at 4.38% and it closed at 4.41% on Thursday evening. Through Thursday, the Corporate Bond Index year-to-date total return was -1.20% and the yield to maturity for the index was 5.26%.

Points of Interest

It was another volatile week for risk assets with plenty of headlines to parse and lots of risk reversals depending on the social media post of the day (or minute) regarding Iran. Equities continued to bear most of the brunt and IG credit was particularly well behaved. Investment grade credit is lower on the risk spectrum relative to most other assets and higher yields have drawn investor interest which has helped support spreads. On the economic front, it was a light week for meaningful data. Next week things ramp up with consumer confidence, retail sales, vehicle sales and then finally the nonfarm payroll report on Friday morning.

Primary Market

New issue volume this week was $28.95bln, in line with the $30bln estimate. Next week is expected to be light with an estimate of just $10bln in new supply. Bond and equity markets are closed next Friday in observance of Good Friday. Year-to-date new issue supply stood at $631bln through the end of the week.

Flows

According to LSEG Lipper, for the week ended March 24th, short and intermediate investment-grade bond funds reported a net inflow of +$2.9bln. This was the 17th consecutive week of inflows. 2026 year-to-date flows into investment grade were +$44.1bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.