CAM Investment Grade Weekly Insights

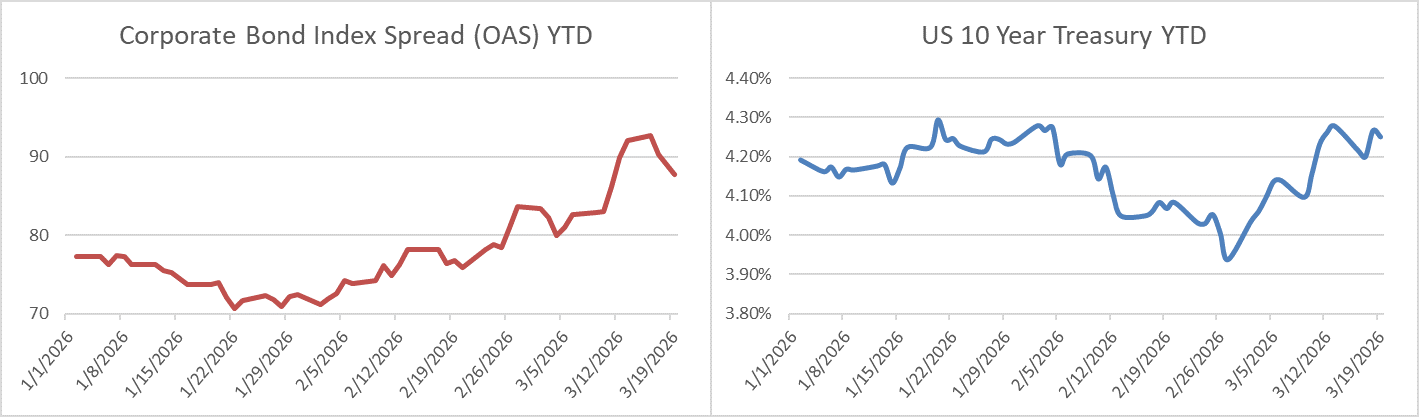

Credit spreads were tighter this week. The OAS on the Corporate Index closed at 88 on Thursday March 19th after closing the week prior at 92. Spreads were quite volatile throughout the period but the price action was downright orderly compared to most risk assets. Equites are poised to finish lower for the 4th consecutive week. The 10yr Treasury ended last week at 4.28% and it closed at 4.25% on Thursday evening. The benchmark rate was sharply higher on Friday and was trading at 4.37% as we went to print on Friday afternoon. Through Thursday, the Corporate Bond Index year-to-date total return was -0.36% and the yield to maturity for the index was 5.11%.

Points of Interest

Volatility took center stage once again as the war with Iran continued to drag on. There was extensive damage to energy infrastructure in the middle east this week. In one particular instance, QatarEnergy’s CEO commented that Iranian attacks had knocked out 17% of Qatar’s liquified natural gas export capacity for least three to five years, threatening supplies to Europe and Asia.[i] In domestic news, the FOMC rate decision was the highlight of the week. As expected, the committee left its policy rate unchanged. Chairman Powell’s presser was interpreted as somewhat hawkish by investors as he showed little conviction regarding the path forward for interest rates. The mere fact that he did not squash the possibility of increasing the policy rate led the market to drastically reprice the path forward. At the beginning of March, investors were pricing two rate cuts in 2026 while the Fed’s dot plot was calling for one. Today, the market is pricing zero rate cuts in 2026 while the updated dot plot released on Wednesday was still predicting a single cut. Bottom line, with the ongoing war, constantly changing tariffs, a tired US labor market and a spike in fuel prices, the path forward is now fraught with uncertainty. If there is one thing that capital markets do not appreciate it is uncertainty. This means volatility is here to stay.

Primary Market

New issue volume this week came in at $36.45bln versus projections of $40bln. All of this supply occurred on Monday and Tuesday as issuers took a pass on Wednesday due to the FOMC and Thursday due to volatility. Syndicate desks are looking for $30bln next week. Year-to-date new issue supply stood at $602bln through the end of the week.

Flows

According to LSEG Lipper, for the week ended March 17th, short and intermediate investment-grade bond funds reported a net inflow of +$4.79bln. This was the 16th consecutive week of inflows. 2026 year-to-date flows into investment grade were +$41.3bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

[i] Reuters, March 19 2026, “Iran attacks wipe out 17% of Qatar’s LNG capacity for up to five years, QatarEnergy CEO says”