CAM High Yield Weekly Insights

(Bloomberg) High Yield Market Highlights

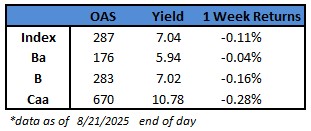

- The US junk bond rally hit a pause as yields crossed the 7% mark to close at a three-week high of 7.04%, after rising for four sessions, the longest streak since early April. Spreads closed at a two-week high of 287 basis points after climbing eight basis points in the last four sessions. Rising yields and steadily widening spreads drove losses for the third consecutive session and the biggest one-day loss in three weeks.

- The rally lost steam after the minutes of the last Fed meeting showed that most policy makers were concerned about inflation risks in the coming months. Momentum faded further ahead of Chair Powell’s speech at the gathering of central bank officials in Jackson Hole later Friday.

- Bloomberg economists Anna Wong and Chris G Collins expect Powell to acknowledge labor market weakness, while also maintaining that demand and supply have offset each other as reflected in the low unemployment rate

- While data showed the labor market weakening, the solid factory purchasing managers index dampened hopes of a rate cut in September. Traders trimmed their bets for a rate cut in September. The probability of a rate cut in the next meeting dropped to about 71% from 100% a few days ago.

- A bevy of Fed officials continue to say inflation risks outweigh their concerns about weaker employment

- Chicago Fed President Austan Goolsbee said while some recent inflation readings have come in better than expected, he hopes one “dangerous” data point is just a blip, referring to the data showing services inflation shooting up

- The decline extended across the market. BB yields are up six basis points for the week and closed at a two-week high.

- CCCs extended their modest loss for the fourth session in a row. Yields rose 27 basis points in four sessions to a nearly five-week high of 10.78%, and spreads to a three-week high of 670 basis points. Spreads widened for the sixth consecutive session, the longest streak since April

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.