CAM Investment Grade Weekly Insights

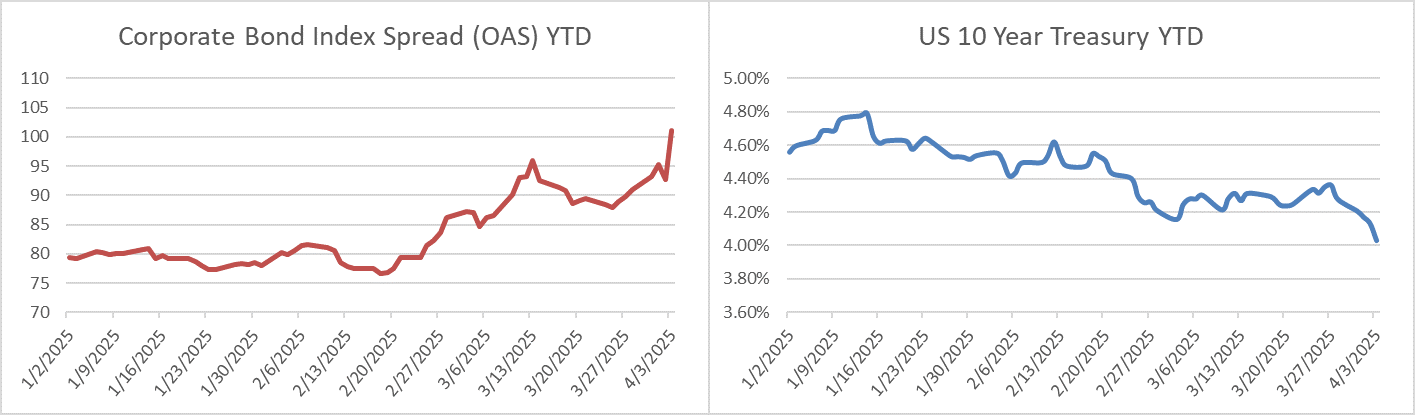

Credit spreads will finish this week much wider. The OAS on the corporate index closed at 102 on Thursday evening after ending the week prior at a spread of 93 and the IG credit market is generically 10bps wider as we go to print mid-morning on Friday. The 10yr Treasury yield rallied after Wednesday’s tariff announcement, moving from 4.25% at the end of last week to 4.03% at Thursday’s close. The benchmark rate is rallying again this Friday morning and is another 13bps lower at press time on the back of China’s retaliatory tariff response and weakness in global equity markets. IG credit is hanging in there for now and doing its job as a tool for diversification. Through Thursday, the Corporate Bond Index year-to-date total return was +2.82% while the yield to maturity for the Index closed the day at 5.06%.

Economics

The data this week took a back seat to global trade. The U.S. tariff announcements on Wednesday roiled global markets causing a rout in equities and wider credit spreads. U.S. Treasuries were a safe haven for investors and yields plunged. Friday’s employment report for the month of March was solid as payrolls posted a broad advance, easily besting the consensus number. The unemployment rate ticked higher from 4.1% in February to 4.2% for March. Markets paid little mind to the positive report with some investors dismissing it as backward-looking relative to the uncertainty regard trade. Traders are now trying to figure out how to navigate a global trade war as China announced retaliatory tariffs on Friday. It appears that there will not be a quick resolution on trade and that volatility is here to stay.

Looking ahead, all eyes will be on Fed chairman Jerome Powell who is slated to speak later this Friday morning. Major data releases next week include CPI and PPI, both in the latter half of the week.

Issuance

It was a very light week in the primary market which is no surprise considering the volatile backdrop. Just four firms sold $6bln of new debt relative to the $20bln estimate. The outlook for next week is murky and will be dependent on the market tone –dealers are estimating $10-$15bln of new supply.

Flows

According to LSEG Lipper, for the week ended March April 2, investment-grade bond funds reported their second net outflow of the year at -$353mm. This was the second consecutive week of modestly negative flows. Total year-to-date flows into investment grade funds are still soundly positive at +$19.31bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.