CAM Investment Grade Weekly Insights

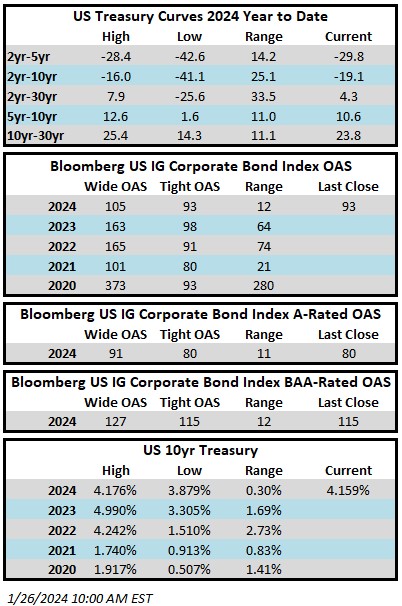

Credit spreads are once again trading at the tightest levels of the year as we go to print. The Bloomberg US Corporate Bond Index closed at 93 on Thursday January 25 after having closed the week prior at 95. The 10yr is trading at 4.16% this Friday morning after closing last week at 4.12% –the 10yr yield is 24bps higher than where it began 2024. Through Thursday, the Corporate Index YTD total return was -0.99%.

Economics

It was a robust week of data and central bank meetings, although none of the releases resulted in large market swings. The Bank of Canada held its key rate at 5% on Wednesday while the ECB held its deposit rate at 4% for the third consecutive meeting on Thursday. In the U.S. the most anticipated release was Friday morning when the Federal Reserve’s preferred inflation measure hit the tape. PCE rose 0.2% in December from the previous month after posting a 0.1% decline in November. It showed that prices were up 2.6% on the year, which is much lower than the reading at the end of 2022. Bottom line, the data is showing significant progress in the war against inflation. Next week, all eyes are on the FOMC which releases its first rate decision of the year on Wednesday. Market prognosticators are looking for the Fed to hold steady but it is the commentary around the timing of easing that could impact global markets.

Issuance

Issuance this week was not paltry but it was underwhelming compared to the consensus estimate as companies priced $18.55bln in new debt relative to expectations of $25bln. There is one deal pending on Friday morning with its size to-be-determined which will add to the monthly total through Thursday of $167.8bln. Recall that the all-time record for the month of January was $175bln which was set in 2017. This record is well within striking distance as preliminary estimates for issuance next week are $20-$25bln.

Flows

According to Refinitiv Lipper, for the week ended January 24, investment-grade bond funds reported a net inflow of +$1.24bln. This was the sixth consecutive weekly inflow for IG funds.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.