CAM Investment Grade Weekly Insights

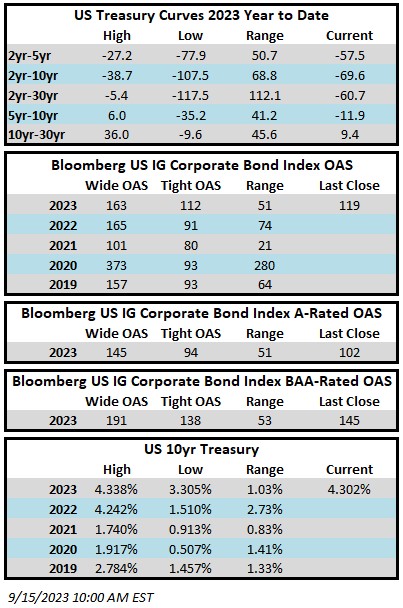

Investment grade credit spreads drifted a touch wider mid-week before settling into a level that was mostly unchanged as we went to print on Friday. The Bloomberg US Corporate Bond Index closed at 119 on Thursday September 14 after having closed the week prior at 119. The 10yr was trading at 4.30% Friday morning, higher by 4 basis points on the week. Through Thursday, the Corporate Index YTD total return was +1.76%.

It was one of the busier weeks for economic data that we have experienced in some time. Monday and Tuesday where quiet before things picked up on Wednesday with August CPI that came in hotter than expected, although more than half of the increase in the numbers was attributable to gasoline. On Thursday, Retail sales came in significantly higher than expected but also due in part to some help from fuel prices. The control-group sales were much softer. Like much of the economic data we have received throughout 2023, there were tidbits that fit the narrative of those in both the soft and hard landing camps. Also on Thursday, the ECB delivered its 10th and likely final rate hike: “Based on its current assessment, the Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target.” Finally, on Friday there was some good news in the U.S. as inflation expectations fell to the lowest level in over two years, with respondents seeing cost increases of +2.7% over the next five to ten years. Next Wednesday, all eyes will be on the FOMC. Most economic prognosticators expect that the Fed will keep rates steady. The Fed’s dot plot shows one more increase at its November meeting but economists surveyed by Bloomberg think that the Fed will forego this final increase.

There was $34bln of new issuance on the week, which we would typically classify as a fairly busy week. However, most of the supply this week, and for the month of September, has been somewhat niche-like in nature, failing to satisfy broader investor demand. This month has seen a dichotomy of issuers with many smaller one-off issuers and then also a mix of serial issuers that tap the market frequently. As a result, we believe that the month-to-date supply figure of $90bln is somewhat misleading. Even though the actual dollar volume of supply has been solid thus far it has left many investors hungry for more because it hasn’t been the right fit for many market participants. Next week should see an additional $15-$20bln of supply based on street estimates, a subdued figure relative to the past two weeks due to the FOMC meeting on Wednesday.

According to Refinitiv Lipper, for the week ended September 13, investment-grade bond funds reported a net inflow of +$233mln. This is the first weekly inflow for IG in 4 weeks but flows for the full year are a net positive +$23.8bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.