CAM Investment Grade Weekly Insights

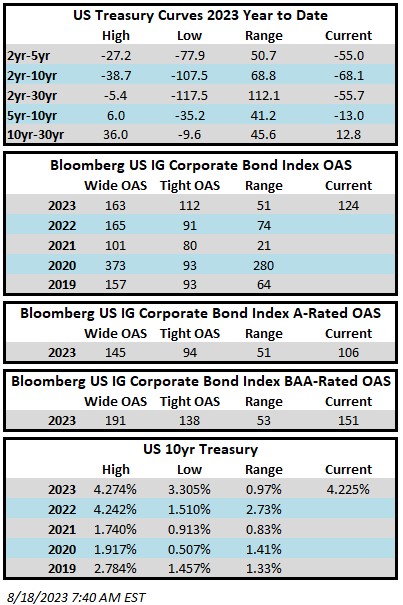

Investment grade credit spreads will finish the week wider. The Bloomberg US Corporate Bond Index closed at 124 on Thursday August 17 after having closed the week prior at 119. The 10yr is trading at 4.23% this morning, higher by 8 basis points on the week. Through Thursday August 10 the Corporate Index YTD total return was +0.87%. Although higher interest rates have weighed on returns in recent weeks, spreads have been resilient and the asset class has remained in positive territory as a result.

”

Interest rates were at the forefront this week. The 10yr Treasury touched its highest yields since 2008 after it closed one evening above 4.25%. The average mortgage rate rose to 7.09%, its highest level in more than 20 years.[i] Economic data on the week was strong, especially Retail Sales which showed a month on month advance of +0.7% relative to expectations of +0.4%. The most recent Fed meeting minutes reinforced the narrative that rates may possibly be held at their current level (or higher) for an extended period. It seems the move higher in rates is less about any one specific economic release and more about market participants coming around to the idea that the economy truly could experience a soft landing. Bearish investors are tempering optimism about the economy by pointing to dwindling excess savings, resumption of student loan payments and consumer credit card borrowing that just surpassed an all-time high of $1 trillion. There continue to be good arguments on both sides in the soft versus hard landing debate.

It was a light week for issuance as higher interest rates and squishy credit spreads likely kept some borrowers on the sidelines. The next two weeks figure to be pretty light from a calendar perspective as we head into the final stanza of the summer season. There has been $853bln of issuance year-to-date.

According to Refinitiv Lipper, for the week ended August 16, investment-grade bond funds reported a net outflow of -575mm. Flows for the full year are a net positive +$27.5bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

[1] The Wall Street Journal, August 17 2023, “Mortgage Rates Hit 7.09%, Highest in More Than 20 Years”