CAM Investment Grade Weekly Insights

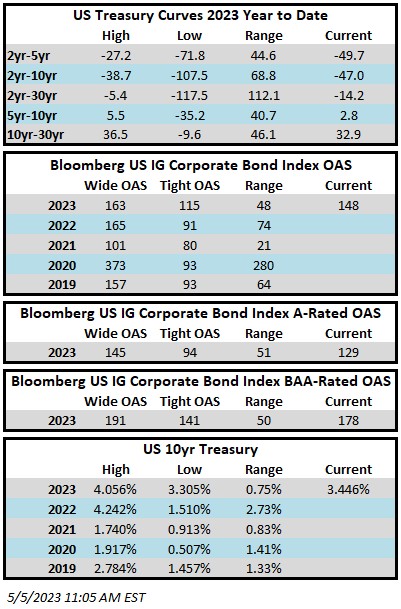

Investment grade credit spreads moved wider throughout the week. The Bloomberg US Corporate Bond Index closed at 148 on Thursday May 4 after having closed the week prior at 136. The 10yr Treasury yield was only a few basis points higher this week after having closed last Friday at 3.42%. Through Thursday, the Corporate Index had a YTD total return of +3.92%. Much of the softness in spreads this week can be traced to renewed fears about regional bank deposits and capitalization. It didn’t help matters that TD and First Horizon agreed to terminate their $13bln merger on Thursday. Midway through the trading day on Friday we are seeing a relief rally in financials which could lead the index to close tighter for the day.

There was a huge amount of data to analyze this week. The biggest event of the week was on Wednesday as the FOMC chose to raise its benchmark rate by +25bps, in line with expectations. The Fed did not go as far as to say that this was the last hike of this cycle but it left open the possibility that it could be. On Friday, we got a very solid labor report that won’t make the Fed’s job any easier. The unemployment rate edged lower to 3.4% while the labor market added +253k jobs during the month of April relative to expectations of a jobs gain of just +185k. There were also ISM services and manufacturing releases this week that indicated a strengthening economy during the month of April. Overall, the data on the week was mixed, but it reinforced the “higher for longer” narrative that some prognosticators are predicting out of the FOMC. Away from the U.S. we also got a +25bps policy rate increase by the ECB with signaling of further tightening to come.

The primary market got off to a strong start in what is expected to be a busy month of May. Through Thursday, $28.35bln in new debt had priced. This is an impressive figure considering the fact that spreads drifted wider throughout the week. There are 2 deals pending on Friday totaling $1bln+ which will likely be enough to push the weekly total beyond $30bln. Supply estimates next week are calling for another $30-$35bln in new debt.

According to Refinitiv Lipper, for the week ended 5/3/2023, investment-grade bond funds reported an inflow of +$0.322bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.