CAM Investment Grade Weekly Insights

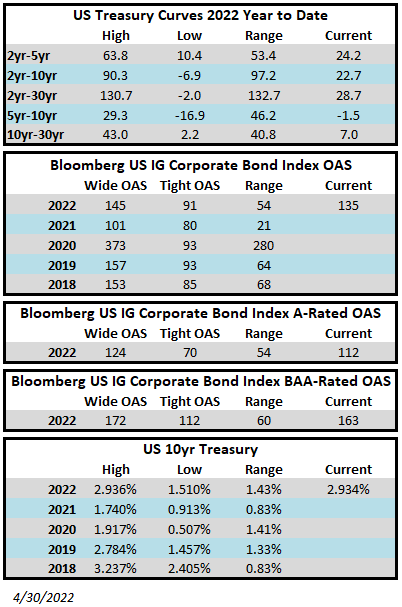

It was an ugly week for risk assets. The OAS on the Bloomberg US Corporate Bond Index closed the week of April 29th at 135 after having closed the week prior at 132. The month of April is one that investors would like to forget; it was historically bad for credit and stocks were down substantially. All eyes will be on the Federal Reserve next Wednesday. The market is pricing in a 50bps increase in the Fed Funds rate and is awaiting more details on balance sheet run-off. The Investment Grade Corporate Index had a negative YTD total return of -12.73% through the end of the week while the YTD S&P500 Index return was -12.92% and the Nasdaq Composite Index return was -21.2%.

Volume in the primary market was underwhelming during the week and finished just under $9bln relative to estimates that were in the neighborhood of $25bln. Per Bloomberg, this boosted the monthly total for April to $107.2bln. Historically, May is a seasonally busy month and estimates are calling for $125-150bln of monthly supply. While investor demand for high quality issuers has remained strong, we detect a sentiment of caution among borrowers as their funding costs are higher than they have been in several years so it will be interesting to see if May volume can keep pace with expectations. There are some large bond deals waiting in the wings related to M&A that could come to market in May and it will also be interesting to see if investors demand higher new issue concessions from those borrowers who in some cases have to float large amounts of new debt.

Per data compiled by Wells Fargo, flows for investment grade were negative on the week. Outflows for the week of April 21–27 were -$2.4bln which brings the year-to-date total to -$47.5bln.