CAM Investment Grade Weekly Insights

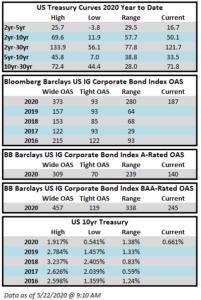

Spreads moved significantly tighter throughout the week. The Bloomberg Barclays US Corporate Index closed on Thursday May 21 at 187 after closing the week of May 15 at 208. The corporate index total return for the year through Thursday was +2.15%. The fixed income markets will close early on Friday ahead of the Memorial Day weekend and spreads are modestly wider as we go to print as it looks like the extended rally in credit might finally have an off day.

The primary market was busy again but volume was lower than the week prior. It could well be that the early market close on Friday was the only thing that kept volumes lower on the week as we saw over $47bln of new debt price through Thursday with no issuers on the calendar for Friday morning. Corporate issuance is closing in on the $1 trillion mark as nearly $970bln of corporate debt has been priced so far this year which is 90% ahead of 2019’s pace. We are still finding attractive opportunities in the primary market but certainly fewer today than in the recent past. According to data compiled by Bloomberg, concessions have trended downward over the last month with issuers averaging just over 5bps this week vs 11bps last week and 22bps the week prior.

According to data compiled by Wells Fargo, inflows for the week of May 14-20 were +$8.5bln which brings the year-to-date total to -$55.2bln. This extends the 7-week steak of inflows to $43.5bln for investment grade funds.