CAM Investment Grade Weekly Insights

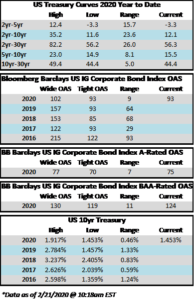

Corporate credit spreads were wider across the board this week but lower Treasury rates were the bigger story and more than offset the move wider in spreads. After closing the week prior at a spread of 96, the Bloomberg Barclays Corporate Index closed Thursday evening at a spread of 97, but spreads are weak and drifting wider as we go to print on Friday morning. Global risk markets are skittish among renewed fears that coronavirus may not be adequately contained. Frankly, we are a bit mystified at how easily markets dismissed virus fears to this point. It is not so much the virus itself but the fact that the second largest economy in the world has been closed for business for the better part of a month. This has serious consequences for growth across the globe due to the interconnected nature of the global economy. Treasuries were volatile over the course of the past week. The 10yr closed at 1.58% last Friday and it is wrapped around 1.45% as we go to print, coincident with its lowest levels of 2019. Meanwhile, the 30yr Treasury fell as much as 7 basis points on Friday morning to an all-time low of 1.89%.

The primary market had a very solid week especially considering it was shortened by one day due to a market holiday on Monday. Weekly issuance topped $35bln pushing the month-to-date total north of $86bln. Year-to-date issuance is now closing in on $220bln which is ahead of 2019’s pace by more than +23% according to data compiled by Bloomberg. Issuance is off to a strong start in 2020 but we would expect this pace to slow in the second half of the year as the presidential election approaches.

According to Wells Fargo, IG fund flows during the week of February 13-19 were +$7.4bln. This marks one of the strongest starts to a year on record. Year-to-date IG fund flows have now eclipsed $71bln.