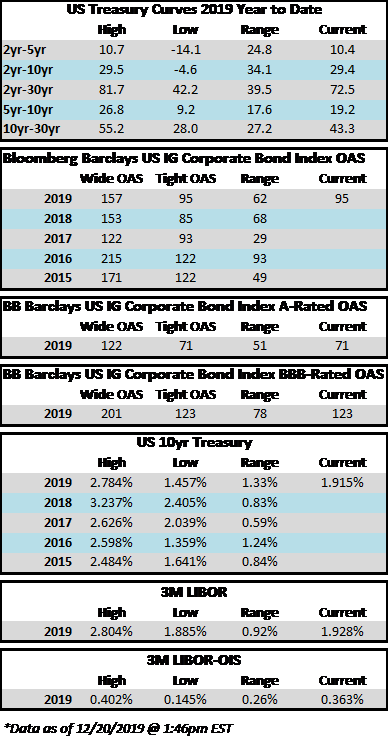

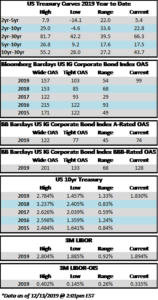

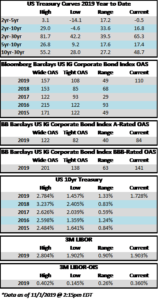

Another week has come and gone and corporate bonds continue to inch tighter into year end. The OAS on the Bloomberg Barclays Corporate Index opened the week at 99 and closed at 95 on Thursday. Spreads are now at their tightest levels of 2019 and the narrowest since February of 2018 when the OAS on the index closed as low as 85. Price action in rates was relatively muted during the week amid low volumes but Treasuries are set to finish the week a few basis points higher. The 10yr opened the week at 1.87% and is trading at 1.91% as we go to print.

As expected, the primary market during the week was as quiet as a church mouse. December supply stands at a paltry $18.9bln according to data compiled by Bloomberg. 2019 issuance stands at $1,110bln which trails 2018 by 4%. As we look ahead to 2020, we expect robust supply right of the gates in January but the street consensus for 2020 as a whole is that supply will be down 5% relative to 2019. Further, net supply, which accounts for issuance less the 2020 maturity of outstanding bonds, will be down substantially from prior years. If these forecasts come to fruition then the supply backdrop could lend technical support to credit spreads in 2020. Supply, however, is merely one piece of the puzzle.

According to Wells Fargo, IG fund flows during the week of December 12-18 were +$0.85bln. This brings YTD IG fund flows to +$295bln. 2019 flows are up over 11% relative to 2018.

The grind continues as the OAS on the Bloomberg Barclays Corporate Index breached 100 for the first time in 2019 with a 99 close on Thursday evening. The index has not traded inside of 100 since March of 2018 and has averaged a spread of 127 over the past 5-years and 113 over the past 3-years. Treasuries were again volatile on the week, especially Friday, which saw a range of 15 basis points on the 10yr Treasury. However, as we type this during the late afternoon on Friday it appears that the 10yr is going to end the week almost entirely unchanged from the prior weeks close.

The primary market has entered year-end Holiday mode. Less than $4bln in new debt was brought to market during the week. The first half of next week is the last chance for meaningful issuance in the month of December. According to data compiled by Bloomberg, 2019 issuance stands at $1,110bln which trails 2018 by 4%.

According to Wells Fargo, IG fund flows during the week of December 5-11 were +$5.4bln. This brings YTD IG fund flows to +$282bln. 2019 flows are up over 10% relative to 2018.

This is an abbreviated Note due to the Thanksgiving holiday. Happy Thanksgiving!

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $0.2 billion and year to date flows stand at $23.5 billion. New issuance for the week was $12.8 billion and year to date HY is at $251.1 billion, which is +55% over the same period last year.

(Bloomberg) Single and Double B Junk Bond Returns Hit 2019 Peak Amid Rally

Junk bond returns are creeping back to record highs after three consecutive days of gains.

Junk bond year-to-date returns rose to 11.928%, inching closer to the highs of just over 12% reached earlier this month. Index yields were unchanged, closing at a two-week low of 5.64%

BB returns hit a year-to-date peak of 13.944%, while single B returns set a new high at 12.553%

CCCs are also catching a bid, boosted by a lift in energy bonds, after posting gains for three straight sessions to take year-to-date returns to 4.101%. That comes less than a week after CCC spreads jumped above 1,000bps over U.S. Treasuries for the first time in more than three years

Credit spreads are set to finish the week generally unchanged but may be a touch wider in some spots when it is all said and done. The spread on the Bloomberg Barclays Corporate Index opened the holiday shortened week at 105 and closed at 106 on Thursday. There is positive sentiment in the markets on Friday morning amid China-US trade innuendo out of Washington. For the second week in a row we have seen a relatively significant move in treasuries; last week it was higher rates and this week lower. The 10yr Treasury closed the prior week at 1.94% and is now 1.83%, 11 basis points lower on the week as we go to print.

The primary market posted an impressive haul this week, especially considering the fact that the market was closed on Monday. It was the second largest volume week of the year thanks to a big boost from AbbVie, which printed a $30bln deal that featured 10 different maturities. With one deal pending this morning, weekly issuance will come in at the $50bln mark. Oddly enough both the largest and second largest issuance weeks in 2019 have both come on holiday shortened weeks. The largest volume week was the week of Labor Day when nearly $75bln of new debt was priced in just four days. According to data compiled by Bloomberg, 2019 issuance stands at $1,065bln which trails 2018 by -4.4%.

According to Wells Fargo, IG fund flows during the week of November 7-November 13 were +$2.8bln. This brings YTD IG fund flows to +$252bln. 2019 flows are up 9.5% relative to 2018.

Bloomberg) AbbVie Propels High-Grade Issuance to Year’s Second-Biggest Week

It’s the second-biggest week of the year for U.S. investment-grade issuance, which at about $50 billion in volume trails only the record-setting start to September.

AbbVie’s $30 billion deal on Tuesday clocked in as the year’s largest bond sale and the fourth-biggest ever, helping to establish this week’s second-place finish

Supply for the week stands at $49.4 billion as of Thursday with more deals potentially coming Friday given a shorter window to sell debt after Monday’s Veteran Day close

The first week of September saw $75 billion of high-grade bond sales, the most for any comparable period since records began in 1972

This week overtook the five days to May 9, when IBM and Bristol Myers brought $39 billion in acquisition-related supply in a 24-hour span

(Bloomberg) Here’s How KKR Might Just Pull Off the Biggest LBO in History

One of the private equity industry’s titans called it a “stretch,” and it’s been dismissed as a pipe dream by a bevy of analysts.

Yet interviews in recent days with debt-market specialists suggest that KKR & Co. could find a narrow path to finance what would be the biggest leveraged buyout in history: a potential take-private deal for pharmacy chain Walgreens Boots Alliance Inc. that analysts have estimated would need to be funded with at least $50 billion of debt.

The challenge for any Walgreens suitor will be raising the necessary money via the markets of choice for private equity firms — junk-rated loans and bonds — which have become fragile after an unprecedented borrowing binge left investors with a hangover. Debt funds that financed more than $3.5 trillion of leveraged buyouts in the past decade have become pickier, leaving banks stuck holding more than $2 billion of unsold loans on their balance sheets as recently as last month.

But a road map may be hidden in two other recent debt-fueled takeovers: Dell Technologies Inc.’s $67 billion takeover of EMC Corp. in 2016 and Charter Communications Inc.’s $78.7 billion acquisition of Time Warner Cable Inc. that same year.

Junk-rated Dell and Charter both borrowed heavily in the investment-grade bond market by issuing secured debt. T-Mobile US Inc. is going down a similar route to help pay for its purchase of Sprint Corp.

In Charter’s case, it pledged security to new and existing bonds issued by higher-rated Time Warner to ensure the debt remained investment-grade. Dell used a similar strategy when it bought investment-grade rated EMC. Walgreens’s debt could be segregated into two borrowing structures at a holding company level and an operating company portion, with investment-grade debt placed on the latter.

In doing so, Dell and Charter won access to the most stable part of the corporate debt market, where investors are still buying heavily as an alternative to low or negative-yielding assets elsewhere. At the same time, they limited their reliance on leveraged finance markets, where sentiment can shift quickly and prove costly.

Both companies did tap those markets, but with more manageable offerings. Bankers who asked not to be identified estimated that Walgreens would be able to raise between $10 billion and $20 billion of junk-rated debt to fund a buyout.

Other market participants, who asked not to be named because they weren’t authorized to speak publicly, said KKR still might need to find a deep-pocketed third-party investor to help put more equity into the deal.

Or it may seek to spin off a portion of Walgreens to lessen its financing needs. The company’s European operations could potentially bring in $18 billion to $20 billion, CreditSights analyst James Goldstein said in a phone interview.

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $1.6 billion and year to date flows stand at $24.4 billion. New issuance for the week was $3.8 billion and year to date HY is at $219.3 billion, which is +37% over the same period last year.

(Bloomberg) High Yield Market Highlights

S. junk bonds rebounded as equities rallied to a record high and the 10Y UST yield jumped. The debt may open on a softer note as stock futures declined and oil prices dropped amid uncertainty over supply cuts.

The debt’s returns turned positive on Thursday after a two-day losing streak as equities climbed to a new high. Year-to-date returns were 12.01%, just 9bps off the 2019 peak

Gains were across ratings, with single-Bs posting the most at 0.1% and YTD at 12.39%

Junk bond yields were little changed. Single-Bs dropped 6bps to close at 5.68% and BBs closed at 3.88%, down 2bps

Spreads held firm across ratings moving in tandem with UST yields

There was lull in the primary market with just two drive-by deals for $1.1b pricing yesterday

Yesterday’s deals took the November volume to $4.98b

As investors turned cautious of weaker credits, Wesco’s $2.18b bond offering faced some resistance and its pricing was delayed

(Reuters) U.S. may not need to impose auto tariffs this month

The United States may not need to impose tariffs on imported vehicles later this month after holding “good conversations” with automakers in the European Union, Japan and Korea, U.S. Commerce Secretary Wilbur Ross said in an interview published on Sunday.

The United States must decide by Nov. 14 whether to impose threatened U.S. national security tariffs of as much as 25% on vehicles and parts. The tariffs have already been delayed once by six months, and trade experts say that could happen again.

“We have had very good conversations with our European friends, with our Japanese friends, with our Korean friends, and those are the major auto producing sectors,” Ross said.

“Our hope is that the negotiations we have been having with individual companies about their capital investment plans will bear enough fruit that it may not be necessary to put the 232 (tariffs) fully into effect, may not even be necessary to put it partly in effect,” he added.

(Business Wire) The GEO Group Reports Third Quarter 2019 Results

GEO reported third quarter 2019 net income attributable to GEO of $45.9 million, compared to $39.3 million, for the third quarter 2018. GEO reported total revenues for the third quarter 2019 of $631.6 million up from $583.5 million for the third quarter 2018.

GEO reported third quarter 2019 Normalized Funds From Operations (“Normalized FFO”) of $70.3 million, compared to $62.9 million, for the third quarter 2018. GEO reported third quarter 2019 Adjusted Funds From Operations (“AFFO”) of $85.6 million, compared to $77.9 million, for the third quarter 2018.

George C. Zoley, Chairman and Chief Executive Officer of GEO, said, “We are pleased with our strong quarterly financial performance, which reflect strong fundamentals and growing earnings. During the quarter, we reactivated 4,600 previously idle beds, which are expected to drive future cash flow growth. We are proud to have published our first-ever Human Rights and ESG report in September, highlighting our long-standing commitment to respecting the human rights of all those in our care, as well as, the continued success of our GEO Continuum of Care enhanced rehabilitation and post-release programs. We believe that our current dividend payment is supported by stable and predictable cash flows, and we expect to continue to apply our growing excess cash flow towards paying down debt.”

During the third quarter 2019, GEO repurchased approximately $34 million of senior unsecured notes due 2022. GEO also closed on a $44 million, 15-year real estate loan bearing interest at 4.22 percent annually. At the end of the third quarter, GEO had approximately $395 million in available borrowing capacity under its $900 million revolving credit facility, which matures in May 2024.

(Business Wire) Arconic Reports Third Quarter 2019 Results

The Company continues to target the completion of the separation in the second quarter 2020. We expect the Form 10 filing to be available in the fourth quarter 2019. The Engineered Products and Forgings businesses (engine products, fastening systems, engineered structures and forged wheels) will remain in the existing company (Remain Co.), which will be renamed Howmet Aerospace Inc. at separation. The Global Rolled Products businesses (global rolled products, aluminum extrusions and building and construction systems) will comprise Spin Co. and will be named Arconic Corporation at separation.

Arconic Inc. reported third quarter 2019 results, for which the Company reported revenues of $3.6 billion, up 1% year over year. Organic revenue was up 6% year over year on strong volumes across all key markets and favorable pricing in the Engineered Products and Forgings segment, and volume growth in packaging, industrial, and aerospace markets as well as favorable pricing in the Global Rolled Products segment.

Third quarter 2019 operating income was $326 million, versus operating income of $345 million in the third quarter 2018. Operating income excluding special items was $475 million, up 36% year over year, as favorable product pricing, higher volume, favorable aluminum prices, and net cost reductions more than offset operational challenges in the aluminum extrusions business and unfavorable product mix.

Arconic Chairman and Chief Executive Officer John Plant said, “In the third quarter 2019, the Arconic team delivered improved quarterly revenue, adjusted operating income, adjusted operating income margin, adjusted free cash flow and adjusted earnings per share on a year-over-year basis. Arconic’s third quarter 2019 return on net assets improved by 550 basis points year over year. We expect this positive year-over-year trend to continue in the fourth quarter. Based on our performance through the first nine months of 2019 and our outlook for the remainder of 2019, we are increasing our full-year adjusted earnings per share guidance for the third time in 2019.”

Arconic ended the third quarter 2019 with cash on hand of $1.3 billion. Cash provided from operations was $52 million; cash used for financing activities totaled $202 million, reflecting the impact of the accelerated share repurchase program of $200 million; and cash provided from investing activities was $117 million. Adjusted Free Cash Flow for the quarter was $154 million.

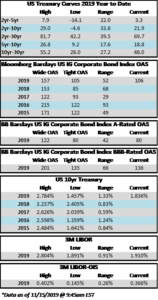

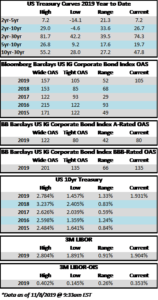

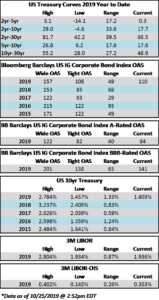

Credit spreads were tighter during the week and are now at the tightest levels of 2019. The spread on the Bloomberg Barclays Corporate Index closed at 105 on Thursday and there is a positive tone in the air on Friday morning which could lead to an even tighter close as we head into the long weekend –the bond market is closed on Monday in honor of Veteran’s Day. The move in Treasuries during the week has more than overshadowed tighter credit spreads. It has been a quick and violent move higher in rates. As we go to print the 10yr Treasury is over 22 basis points higher on the week while the 30yr is 21 basis points higher. Unpredictability in rate moves is the principal reason that we are “rate agnostic” at CAM and instead focus on credit risk while avoiding interest rate speculation by always positioning investor portfolios in intermediate maturities.

The primary market got a decent start to the month as $21.8bln in new debt came to market. The pace should pick up substantially as soon as next week due to pending M&A funding from AbbVie which could total near $30bln. 2019 issuance has now passed the trillion dollar mark and it stands at $1,014bln which trails 2018 by -7%.

According to Wells Fargo, IG fund flows during the week of October 31-November 6 were +$3.2bln. This brings YTD IG fund flows to +$249bln. 2019 flows are up 9.5% relative to 2018.

Bloomberg) Global Bond Sell-Off Persuades Some Investors to Buy the Dip

Recent losses in Treasuries, which crescendoed Thursday into one of the worst days since Donald Trump was elected president, look like a buying opportunity for many investors who have a grim view of the economy’s prospects.

And it appears some are pouncing, with traders cashing out bearish wagers and buy-the-dip buyers rushing in. The rekindled interest in the safety of bonds nudged yields on the 10-year, which had climbed to a three-month high of 1.97% on Thursday, down to as low as 1.89% in early European trading Friday before bouncing back to around 1.94%. European bonds rebounded after French and Belgian yields had climbed above 0% Thursday.

Signs of progress in U.S.-China trade talks have thrashed bonds for days, and the two countries agreed Thursday to roll back tariffs on each other’s goods if a deal is reached. The Treasury market has seen a huge turnaround since August, when fears that global growth is slowing prompted the biggest monthly rally since 2008.

(Bloomberg) U.S. Says Phase-One China Deal Would Include Tariff Rollback

The U.S. and China have agreed to roll back tariffs on each other’s goods in stages as negotiations continue over resolving the more than yearlong trade war, officials on both sides said.

“In the past two weeks, top negotiators had serious, constructive discussions and agreed to remove the additional tariffs in phases as progress is made on the agreement,” China’s Ministry of Commerce spokesman Gao Feng said Thursday.

White House economic adviser Larry Kudlow confirmed the advance in negotiations. “If there’s a phase one trade deal, there are going to be tariff agreements and concessions,” he told Bloomberg.

An agreement to ratchet back tariffs would pave the way for a de-escalation in the trade war that’s cast a shadow over the world economy. China’s key demand since the start of negotiations has been the removal of punitive tariffs imposed by Trump, which by now apply to the majority of its exports to the U.S.

“If China, U.S. reach a phase-one deal, both sides should roll back existing additional tariffs in the same proportion simultaneously based on the content of the agreement, which is an important condition for reaching the agreement,” Gao said Thursday.

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $1.1 billion and year to date flows stand at $22.9 billion. New issuance for the week was $5.9 billion and year to date HY is at $215.4 billion, which is +36% over the same period last year.

(Bloomberg) High Yield Market Highlights

U.S. junk bonds are set to rebound from a three-day decline to open higher this morning as stock futures advance on the heels of better-than-expected manufacturing data from China and as oil prices rise after a four-day losing streak.

Junk bonds fell for the third straight session and reported a loss of 0.15%, the longest losing streak in almost five weeks. Spreads are 38bps wider in the past four days at 392bps over U.S. Treasuries

CCCs posted a loss of 0.29%, the most across high yield yesterday, taking year-to-date returns down to 5.38%. CCC yields surged to a nine-month high of 11.25% and spreads widened the most in 10 months to 969bps

Investors, though cautious, continued to allocate cash to high-yield for the week

Supply has ground to a halt with no new deals announced or priced in the past two days but there are some in the pipeline that could emerge soon.

(Bloomberg) Extended Junk Rally Squeezes Spread Between BBB and BB to Record

The difference between BBB and BB U.S. corporate bond spreads collapsed further as investors continued chasing yield in the highest-rated junk bonds

The differential between the best high yield and worst investment grade hit a fresh post-credit crisis low amid continued inflows to bond funds and negative yielding debt

overseas

The compression is making it so investors may have to start reaching even further down the ratings spectrum to find value

The differential between BBB and BB was 49 basis points Monday morning, a new record

(Business Wire) Western Digital Announces CEO Succession Plan

Western Digital Corp. announced that Steve Milligan, chief executive officer and a member of the Western Digital Board of Directors (“the Board”) since January 2013, has informed the Board that he intends to retire as the Company’s CEO. Milligan will continue to serve as CEO until the Board has identified and appointed a successor, and then will remain with the Company in an advisory role until September 2020 to ensure a smooth transition. He will also remain a director on the Company’s Board for a transition period after his successor is appointed.

The Board has initiated a search to identify Western Digital’s next CEO, and has engaged Heidrick & Struggles, a leading executive search firm, to assist in the process. In order to facilitate a comprehensive process, the Board will evaluate both internal and external candidates.

“The Board and management team are committed to ensuring a smooth transition, and we are grateful that we’ll continue to benefit from Steve’s experience and perspective throughout this process,” said Matthew Massengill, chairman of the Board. “As the Board conducts its search for Steve’s successor, we are focused on identifying a strong leader with a proven track record of operating successfully at scale while defining and executing a growth strategy driven by innovation, operational excellence, and world-class talent development.”

(PR Newswire) Tenneco Reports Third Quarter 2019 Results

Tenneco Inc. reported third quarter 2019 revenue of $4.3 billion, versus $2.4 billiona year ago, including $1.8 billion from acquisitions. On a constant currency pro forma basis, total revenue increased 3% versus last year, while light vehicle industry production declined 3% in the quarter.

Third quarter EBIT was $148 millionincluding the acquired Federal-Mogul business, versus $112 million last year. EBIT as a percent of revenue was 3.4% versus 4.7% last year. Cash generated from operations was $164 million.

Light vehicle production in the fourth quarter is expected to be lower year-over-year by 6%, and the commercial truck market is showing signs of softening in the quarter. In this environment, Tenneco expects fourth quarter revenue in the range of $3.95 billionto $4.05 billion. Further, the company expects its fourth quarter adjusted EBITDA to be in the range of $295 million to $315 million, including year-over-year margin improvement of approximately 50 basis points in the DRiV division. The company expects the GM labor stoppage to have a negative impact on EBITDA of approximately $35 million.

The company has made significant progress on the administrative separation of the two business divisions into two independent companies

Tenneco remains committed to the separation of the businesses and continues to execute its plan for the spin off. Additionally, the company is evaluating multiple strategic options to deleverage and facilitate the separation. Certain of these options could help mitigate the impact of challenging market conditions, which, if current trends were to continue, would likely affect the company’s ability to complete a separation in the mid-year 2020 time range.

Reuters) U.S. Fed cuts interest rates, signals it is on hold

The Federal Reserve on Wednesday cut interest rates for the third time this year to help sustain U.S. growth despite a slowdown in other parts of the world, but signaled there would be no further reductions unless the economy takes a turn for the worse.

“We believe that monetary policy is in a good place,” Fed Chair Jerome Powell said in a news conference after the U.S. central bank announced its decision to cut its key overnight lending rate by a quarter of a percentage point to a target range of between 1.50% and 1.75%.

“We took this step to help keep the economy strong in the face of global developments and to provide some insurance against ongoing risks,” he said. “We see the current stance of monetary policy as likely to remain appropriate as long as incoming information about the economy remains broadly consistent with our outlook.”

In his news conference, Powell ticked off an extensive list of reasons why he feels the economy is doing well, and likely to continue to do so under the current stance of monetary policy – from robust consumer spending, strengthening home sales, and asset prices he considered healthy but not to a level of excess.

The outlook for the U.S. economy continues to be for “moderate” growth, a strong labor market and inflation rising back to the Fed’s 2% annual goal, he said, and only “a material reassessment” of that outlook could drive the central bank to cut rates further from here.

Credit spreads were turbulent during the week. The first half of the week saw tighter spreads, and the OAS on the Corporate Index closed at 106 on Tuesday, the tightest level of 2019. Spreads traded wider from there on the back of Fed commentary on Wednesday which was followed by a surprisingly weak Chicago PMI reading on Thursday morning leading to a close of 110 for the index on Hallows eve. The economic news continued to roll in on Friday morning, but this time it was received in positive fashion as employment numbers beat market expectations. As we go to print amid lighter volumes in corporates most bonds are trading 2-4 tighter which should see the index close right around 108. If we do close at 108 then spreads will have finished the week unchanged. Rates too were volatile during the week with the 10yr closing at 1.84% on Monday but it is now trading at 1.73% on Friday afternoon. This is lower on the week, as the 10yr finished the week prior at 1.79%.

The primary market was somewhat more active this week but finished the month well shy of expectations. October volume closed at $68.6bln versus dealer projections of $85bln according to data compiled by Bloomberg. 2019 issuance stands at $992bln which trails 2018 to the tune of -6%.

Demand for corporate credit continues to remain robust. According to Wells Fargo, IG fund flows during the week of October 24-30 were +$4.2bln. This brings YTD IG fund flows to +$246bln. 2019 flows are up over 9% relative to 2018.

(Bloomberg) Credit Risk Gauge Drops to Six-Week Low on Bullish Jobs Report

Investors pushed the cost to protect a basket of investment-grade company debt against default to the lowest level since Sept. 19 following the unexpectedly strong U.S. jobs report on Friday.

The Market CDX Investment Grade index spread fell as much as 2 bps to touch 52.96 bps Friday morning in New York before paring some of the gains to trade at 53.67 bps at 12:30 p.m, according to ICE Data Services. The index narrowed by the most in almost three weeks, data compiled by Bloomberg show.

Excess demand for higher-quality bonds and low supply have propelled gains in corporate investment-grade markets. October new IG issues ended at $68.6 billion, falling short of the $85 billion dealer projections by nearly 20%, while cash continues to flow intohigh-grade bond funds.

(Bloomberg) Riskiest Junk Debt Still Isn’t Cheap Enough to Lure Buyers

Notes rated in the CCC tier, essentially the lowest level in the junk bond market, have grown cheaper since May even as most of the market has grown stronger. Risk premiums, or spreads, on the debt are close to their widest level relative to the tier just above them since mid-2016, according to data compiled by Bloomberg.

The weaker performance of the lowest-rated debt underscores how even as investors are reaching for higher returns as the Federal Reserve eases interest rates, they’re still wary of a potential economic downturn and fear that defaults could start to tick higher. The highest tier of junk bonds have gained 13.5% this year, and overall high-yield corporate bonds are up 11.9%, while those rated CCC have gained just 5.7%.

CCC debt doesn’t usually perform like this. Because the companies that sell the notes are already so close to defaulting, CCC bonds are typically hit harder than the broad market during a market downdraft. When the market recovers, the securities often perform much better. The debt plunged in early 2016 when energy prices dropped, but went on to notch huge returns for the year — 31.5% to the broader market’s 17.1% — as oil prices started recovering.

This year, CCC bonds are performing worse than the market even as the overall supply of the lowest-rated notes has been shrinking. There are about $156 billion of those bonds outstanding today, down from $167 billion in February. So far this year, CCC rated companies have sold around $24 billion of debt, less than the same period for each of the previous two years, according to data compiled by Bloomberg.

Bloomberg) Top Fed Officials Hammer Home Message That Rates Are on Hold

Federal Reserve Vice Chairman Richard Clarida reinforced the central bank’s new message this week that interest rates are on hold, saying that both monetary policy and the U.S. economy are “in a good place,” though some risks remain.

“We have a favorable outlook for the economy,” Clarida said Friday in an interview with Jonathan Ferro and Tom Keene on Bloomberg Television. “We think the economy is in a good place, we think monetary policy is in a good place.”

He repeated that message in a lunchtime speech at the Japan Society in New York, with Fed Vice Chairman for Supervision Randal Quarles delivering a similar signal at an event at the same time at Yale University in New Haven, Connecticut.

The vice chairs’ overlapping remarks hewed closely to what Chairman Jerome Powell said earlier this week after the Fed cut rates for a third time this year, signifying a strong consensus at least among the Board of Governors. The Fed has acted to protect a record U.S. economic expansion amid headwinds from trade uncertainty and global weakness, while the domestic economy has been holding up.

Spreads are tighter to the tune of several basis points on the week while Treasury rates crept higher. The OAS on the Bloomberg Barclays Corporate Index was 110 on Friday morning after having closed at 112 the week prior. Spreads have continued to grind tighter throughout the day as we go to print on Friday afternoon and the close on the index OAS is likely to come close to touching the year-to-date tight of 108. Treasury rates are set to finish the week higher with the 10-year up 5 basis points on the week.

The primary market continued its October trend with another week of lackluster supply. Weekly new issue volume was just shy of $14bln pushing the monthly total to $39.5bln according to data compiled by Bloomberg. 2019 issuance stands at $963bln trailing 2018 by nearly 8% on a relative basis.

According to Wells Fargo, IG fund flows during the week of October 17-23 were +$4.4bln. This brings YTD IG fund flows to +$242bln. 2019 flows are up 9% relative to 2018.

Bloomberg) Bond Funds Learn to Exploit Ratings System to Buy Riskier Debt

In today’s low interest-rate world, investment-grade bond funds face an all-too-familiar trade-off: buy risky debt to improve returns or play it safe and underperform.

In particular, funds are loading up on bonds where ratings firms are split on whether they’re investment grade or junk. While reasonable people can disagree about which one is right, for a growing number of firms, the answer is always the same: the higher one.

The practice has obvious advantages. With high-grade corporate bonds yielding less than 3% on average, managers can pick up an extra half-percentage point on split-rated debt. And funds can say they’re invested in safe assets while running a portfolio that actually looks a lot like a junk bond fund.

Granted, managers have always had the discretion and the flexibility to choose which ratings standards to follow. The methodology is there for all to read in the fund’s prospectus, though it’s often tucked into the fine print. Then, there’s the question of how much stock to put into ratings anyway. Many managers lean on their own analysis to determine a bond’s credit risk.

That extra yield comes with a price. Historical data from S&P shows that lower initial ratings correspond with higher rates of default. The gap is notably stark in the divide between investment grade and junk. Ten-year default rates on bonds with BB ratings are double those with BBB grades.

(Bloomberg) Corporate Bond Syndicates Yawn Amid Sleepiest October in Years

S. investment-grade debt sales are expected to miss estimates for October — by a lot.

Just $39.5 billion of new debt has been sold as of Thursday, compared to initial forecasts calling for $85 billion. This projection, put together by compiling dealer estimates, was revised lower mid-month to around $65 billion and now even that may be a stretch.

Volume is the lowest since October 2013, when $41.9 billion of blue-chip company bonds was sold. There are still five trading days left, but that narrows to two when you consider Fridays are often blank, Wednesday is a Fed decision day and Thursday is Halloween.

The following factors likely play a role.

Big banks have been absent. Of the top 10 U.S. banks, just Bank of America Corp. and Wells Fargo & Co. have issued new debt, together totaling $10. 5 billion. Typically there is more, especially when financial institutions report better-than-expected earnings as Goldman Sachs Group Inc., Morgan Stanley and JPMorgan Chase & Co. have.

Earnings season. Issuers and investors want to see how well companies have been doing. Buyers want to know about the recent quarter and fourth quarter outlook, considering the geopolitical risks such as the U.S.-China trade war and Brexit

Muted merger and acquisition activity. It’s widely understood that M&A issuance is down, but overall the calendar just seems lighter. Every once in a while there is a whisper about T-Mobile USA Inc., but at the moment that is looking more like a 2020 story.

Restart

Issuance will begin to pick up next week, albeit from a pretty low bar set in the last few weeks. Desks are expected to front-run the Fed and complete the bulk of next week’s debt issuance on Monday and Tuesday.

There are a plethora of companies expected to report next week. The week after next, earnings will subside and with the bulk of the reports released, more candidates will consider selling debt. The first week of November is when the real ramp up should occur.

The fact that October is running about 54% behind estimates doesn’t come as a surprise since actual supply has been missing weekly estimates for five weeks in a row. That trend is going to break as Wells Fargo’s $6.5 billion deal catapulted this week to $13.7 billion, in line with estimates of $15 billion area.

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $1.7 billion and year to date flows stand at $21.7 billion. New issuance for the week was $5.6 billion and year to date HY is at $209.4 billion, which is +33% over the same period last year.

(Bloomberg) High Yield Market Highlights

S. junk bond returns hit a new peak of 11.853% this year, the highest since 2016, amid a hunt for yield by investors. Junk bonds have rallied for 11 straight days, the longest winning streak since April, according to Bloomberg Barclays index data.

BB bond returns also rose to a high of 13.433%

Junk bond yields also fell to 5.56%, approaching a 20-month low of 5.55% hit on Sept. 23

BB yields are 3.85%, near the record low of 3.82% reached on Oct. 21

Spreads were largely unchanged moving in tandem with 5Y UST

Investors are pouring cash into the asset class.

The rally may run out of steam Friday as oil prices are lower and stock futures mixed

(Bloomberg) Cracks in Leveraged Credit Are Widening

S. leveraged credit markets are coming under increasing pressure amid price swings, ratings downgrades and selling by CLOs, according to a report from Morgan Stanley.

Strategists led by Srikanth Sankaran identified the increased frequency of big price moves in loans and bonds even outside stressed credits, amid a number of pockets of weakness

In loans, about $48b of notional debt representing 4.2% of the leveraged loan index now trades below 80 cents, compared to $14b and 1.3% a year ago

The sub-90 cash price bucket also increased to 9.8% from 3.2% in the same period, according to the report

“Beneath the veneer of relative spread resilience and muted realized defaults, the weak links in the leveraged credit markets are coming under pressure,” the strategists wrote in the report

Selling pressure from CLOs has exacerbated the loan price swings, and willingness to sell is particularly high in CCCs

“CLO managers are net sellers of large price moves, especially in lower-rated names,” the strategists wrote

(Wall Street Journal) Wave of Financial Stress Hits Low-Rated Companies

An array of business challenges are hitting low-rated companies across the U.S. economy, driving selling in the bottom tier of the corporate-debt market that contrasts with gains in stocks and other riskier assets.

In recent months, consumer demands for wireless phones and high-speed internet have helped push one landline telecom company, Windstream Holdings Inc., into bankruptcy protection and another, Frontier Communications Corp., into restructuring talks with its creditors.

Meanwhile, competition from cheap natural gas and renewable-energy sources has caused at least seven coal producers to file for chapter 11 protection over the past year. Opioid lawsuits and the threat of legislation that would curb surprise medical bills have exposed vulnerabilities at some highly leveraged health-care companies. Retailers continue to be pressured by the shift to online shopping. And a wave of financial distress has again hit the oil patch due in part to persistently low commodity prices.

Taken together, these developments have caused yields, which rise when bond prices fall, to climb for months on the lowest-rated group of corporate bonds. Unusually, that has happened even as yields have fallen on higher-rated junk bonds.

Investors and analysts closely watch junk bonds because companies with subpar credit ratings tend to be affected by economic problems sooner than others. Right now, many remain confident that the problems befalling certain companies aren’t symptomatic of broader economic challenges. Still, others worry that cracks at the very bottom of the market shouldn’t be taken lightly and could ultimately spread to a larger group of assets.

“There are specific names and specific subsectors where things are not working,” said Oleg Melentyev, a credit strategist at Bank of America Corp.

Melentyev doesn’t think the problems facing the lowest-rated businesses will spill over into the broader market. Still, he said, it is difficult to know for sure because “you have too many yellow signs, warning signs, around.”